POWER: EU End of Day Power Summary: France Pulls Back, Germany Trades Rangebound

France January power is pulling back today with ample supply and expectations of seasonally low demand. The German equivalent is trading rangebound with mixed movements in the energy complex, while still tracking weekly losses.

- France Base Power JAN 26 down 1.9% at 68.4 EUR/MWh

- Germany Base Power JAN 26 down 0% at 98.07 EUR/MWh

- Italy Base Power JAN 26 up 0.5% at 113.4 EUR/MWh

- EUA DEC 25 down 0.7% at 81.84 EUR/MT

- TTF Gas JAN 26 up 0.6% at 27.255 EUR/MWh

- TTF front month has recovered slightly after reaching its lowest since April 2024 at €26.80/MWh earlier this morning. A warm weather forecast has added significant pressure this week.

- EUAs Dec25 are edging down today and on track for weekly losses of around 1.5%, trading in a €81‑83/t range through the week, with open interest falling to its lowest level since December 2024.

- CWE spot power prices are expected to be under pressure next week with mean temperatures well above the seasonal average, weighing on demand for electric heating. Wind output is forecast to be higher at the start of the week across the region.

- Swedish utility Vattenfall has received approval to build a 254MW BESS facility at Germany’s decommissioned Brunsbuettel nuclear site.

- The German government announced it will reduce 2026 offshore wind tender volumes to 2.5GW, from 5GW previously.

- Global power markets traded volumes on the EEX exchange declined by 8% on the year in November to 1,105TWh, amid lower European power future volumes.

- GB Energy plans to deliver at least 15GW of clean energy generation and storage capacity by 2030, as part of the Great British Energy Strategic Plan 2025.

- Nordic spot prices are likely to be weighed down next week (week 50) as forecasts point to revised higher and mostly above seasonal temperatures, weighing on heating demand. Strong wind speeds and firm nuclear availability in the region are also expected to add downward pressure.

- OMV Petrom’s 860MW Brazi gas-fired power plant in Romania has resumed operations after a temporary shutdown caused by water restrictions, with full capacity expected soon.

- Orlen has started building its latest 450MW CCGT plant in Gdansk, Poland, with the commencement of capacity obligations slated for 2029.

- Hungarian utility MVM has secured a €1.2bn syndicated loan to build a 1GW CCGT power plant at its Tiszaujvaros site.

- D.Trading has signed a two-year offtake agreement with Eurowind in Romania for the delivery of renewable energy from 110MW of solar and onshore wind plants.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 17W AUCTION: NON-COMP BIDS $424 MLN FROM $69.000 BLN TOTAL

- US TSY 17W AUCTION: NON-COMP BIDS $424 MLN FROM $69.000 BLN TOTAL

US TSYS: Extending Lows

- Treasuries are extending lows at the moment - tracking German Bunds with no obvious headline of Block driver, and unlikely comment from Fed Miran that: "DATA SUGGEST RATES CAN BE A LITTLE LOWER THAN THEY ARE" while "KEEPING POLICY THAT RESTRICTIVE RUNS UNNECESSARY RISKS," Bbg.

- Currently, Dec'25 10Y contract trades -15 to 112-10 low, 10Y yield at 4.1532% (+.0681). A continuation lower would open 112-06, the Sep 25 low and the next key support.

UK: Labour Risks Falling To 3rd In Polls With Budget Statement Looming

The gov't faces a difficult few weeks ahead of the 26 November budget in the wake of Chancellor of the Exchequer Rachel Reeves' Downing St. speech on 4 November that refused to rule out manifesto-breaking income tax/VAT/National Insurance increases. While there is likely to have been an element of needing to prepare the ground with the public and markets regarding the all-but-confirmed tax hikes (saying "each of us must do our bit for the security of our country and the brightness of its future"), coming three weeks before the budget means the looming spectre of tax increases will retain a dominant position in the news cycle.

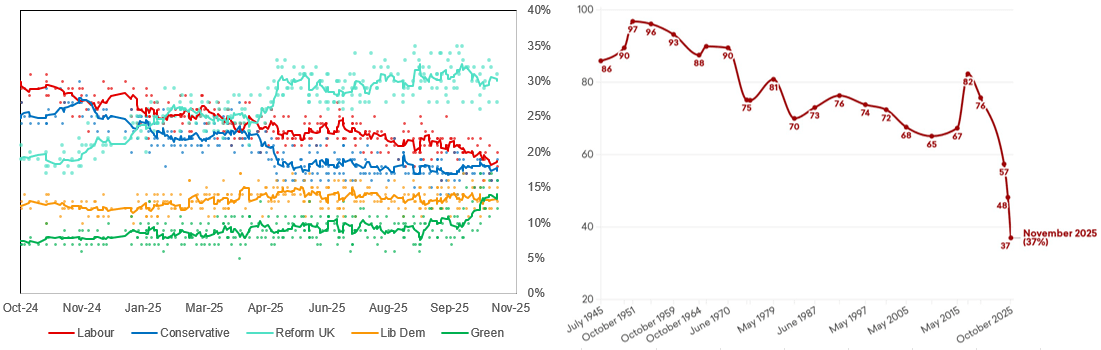

- Comes amid the slow, but sustained decline in support for the centre-left Labour Party in opinion polling (see left chart below). Whereas Labour has trailed the right-wing populist Reform UK for several months, it has generally retained a comfortable advantage over the main opposition centre-right Conservatives. However, with the environmentalist Greens having recorded a spike in support under its new left-wing populist leader, Zack Polanski, largely at the expense of Labour, PM Sir Keir Starmer's party now risks being pushed into third place nationally.

- Should Labour's polling numbers slump even further post-Budget, it will put even greater pressure on Reeves and Starmer, and indeed a significantly negative public or market reaction could make Reeves' position untenable. Data from Smarkets shows bettors assigning a 40.6% implied probability that Starmer leaves office in 2026, with the May local elections viewed as a potential reckoning day for the PM.

Chart 1. General Election Opinion Polling by Party, % and 6-Poll Moving Average (LHS) and Combined Vote Share for Labour and Conservatives in General Elections & Opinion Polling, % (RHS)

Source: More in Common, YouGov, Find Out Now, Opinium, Techne, Lord Ashcroft Polls, Focaldata, JL Partners, Freshwater Strategy, Survation, Ipsos, BMG Research, MNI