POWER: EU End of Day Power Summary: EU Power Rises

CWE and Nordic front-month power futures are holding onto gains in Monday’s session. Forecasts for lower wind output and cool weather in parts of the region paired with gains in EU gas prices are supporting CWE, while a drier outlook is supporting Nordic futures. In the UK, gains in NBP gas are weighed against forecasts for windier and warmer weather.

- Nordic Base Power FEB 26 up 3.7% at 68.15 EUR/MWh

- Germany Base Power FEB 26 up 3.4% at 98.04 EUR/MWh

- France Base Power FEB 26 up 3.2% at 72.49 EUR/MWh

- UK Base Power Feb 26 up 0.5% at 81.6 EUR/MWh (BFV)

- EUA DEC 26 up 0.9% at 88.05 EUR/MT

- TTF Gas FEB 26 up 2.5% at 28.075 EUR/MWh

- TTF front month has risen to offset some of yesterday’s steep declines as the market continues to monitor forecasts for warming temperatures over the coming week before a dip cooler this weekend.

- EUAs Dec26 are rising ahead of the first auction of 2026 tomorrow, with upward momentum in TTF during the afternoon session also providing support.

- Power trading on Epex Spot hit a new monthly record in December 2025, with volumes climbing to 84.3TWh as stronger day-ahead activity drove gains across key European markets.

- EdF has signed a nuclear power production allocation contract (CAPN) with ArcelorMittal for the duration of 18 years.

- The unplanned outage at 905MW Chinon 4 has been extended by 12 hours to end on 7 January 12:00 CET.

- French hydropower reserves in calendar week 1 declined by 4.77 percentage points to 51.2% of capacity.

- German new EV registrations rose by 43.2% on the year in 2025 to 545,142, accounting for a share of 19.1%.

- Bnetza has increased the offered capacity for the country’s first onshore wind auction in 2026 to 3.445GW, up from the initially planned 2.5GW.

- UK new EV registrations in 2025 increased by 23.9% on the year to 473,348 vehicles, accounting for a market share of 23.4%.

- VPI’s 299MW VPI B open cycle gas turbine (OCGT) at Immingham is expected to be commissioned between December 2025 and May 2026.

- Renewables accounted for 55.5% of Spain’s energy mix in 2025, slightly down from 55.8% in 2024.

- The 1.1GW Forsmark 1 nuclear reactor has had an unplanned 104MW curtailment that will last until 8 January 15:00CET.

- Norway’s energy regulator RME/NVE has approved NOK 5.2bn (€440mn) in compensation to Statnett to offset sharply higher system services costs.

- The Czech Republic’s electricity consumption increased by 2.3% year on year in 2025 to 59.3TWh amid colder weather.

- Lithuania’s Litgrid has provisionally reserved 1.2 GW of transmission capacity for renewable and storage projects submitted over the past three months.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Bull Channel Breakout

- RES 4: 1.4140 High Nov 5 and a key resistance

- RES 3: 1.4131 High Nov 21

- RES 2: 1.4051 High Nov 28

- RES 1: 1.3939/4016 Low Nov 28 / 20-day EMA

- PRICE: 1.3865 @ 16:35 GMT Dec 5

- SUP 1: 1.3853 Intraday low

- SUP 2: 1.3840 50.0% retracement of the Jun 16 - Nov 6 bull cycle

- SUP 3: 1.3812 Low Sep 23

- SUP 4: 1.3779 Low Sep 22

A bear theme in USDCAD remains intact and Friday’s strong sell-off reinforces a bear theme. The pair has breached an important support at 1.3942, the base of a bull channel drawn from the Jul 23 low. The break highlights a stronger bear cycle and signals scope for an extension towards 1.3840 next, a Fibonacci retracement point. Initial firm resistance to watch is 1.4016, 20-day EMA.

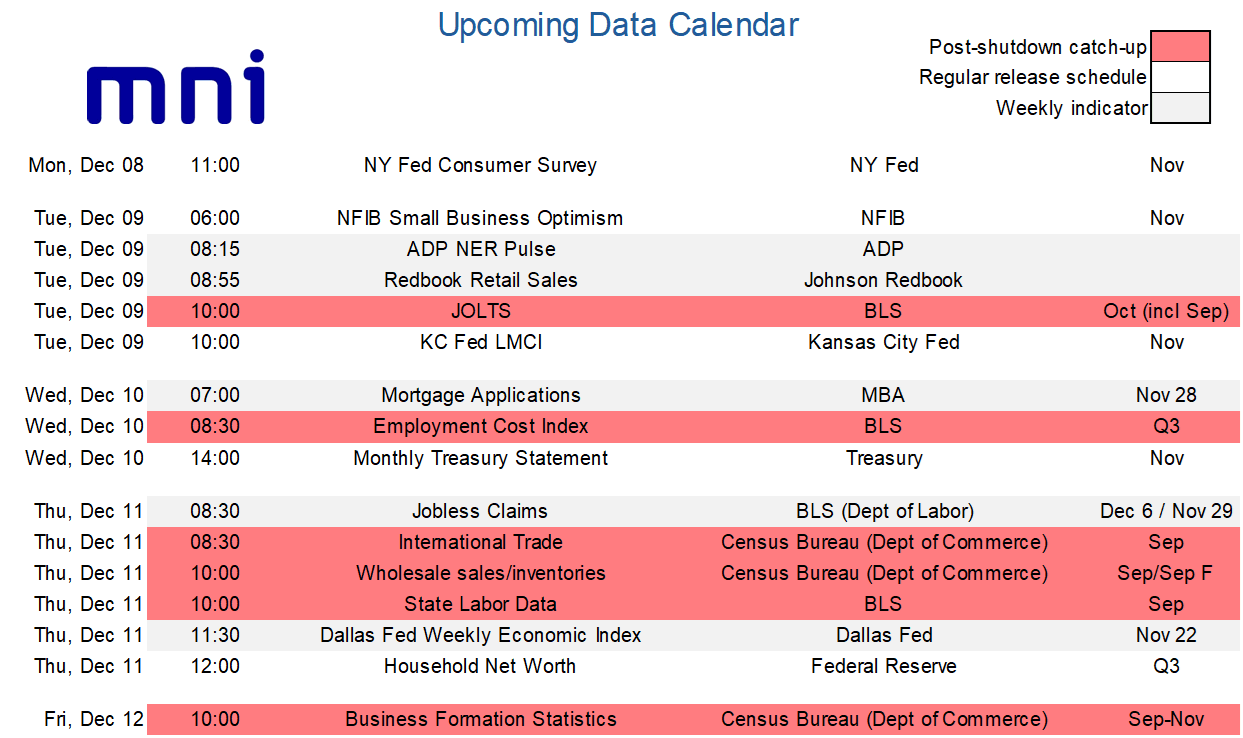

LOOK AHEAD: US Week Ahead: FOMC Decision Dominates, Post Shutdown Data Catch-Up

- Next week’s US calendar is dominated by the FOMC decision on Wednesday, with a third consecutive 25bp cut almost fully priced.

- Expect it to be a contentious meeting however, with many arguing for a pause not least whilst they’re still relatively in the dark on key official data releases following the government shutdown.

- Fed Chair Powell opted for a surprisingly hawkish tone at the late October press conference, highlighting a deeply divided committee on prospects for another cut in December.

- The “fog” had appeared to win out until NY Fed’s Williams, a senior permanent voter, gave unusually explicit guidance on still seeing room “for a further adjustment in the near term”. With no pushback from FOMC members or media briefings, it appears this message has approval from the core of the FOMC which should be enough to see a rate cut this month. The likely catalyst was the further increase in the unemployment rate to 4.44% back in September, although subsequent tracking suggests stabilization and jobless claims data don’t show any signs of deterioration.

- We’ll be looking for the number of hawkish dissents (we’d be surprised if anyone joins Miran dissenting for a 50bp cut) and expect a greater number to object to a cut in the 2025 dot plot, whilst the distribution of dots for 2026 should be in greater focus.

- As for the economic projections, we expect upward revisions to GDP growth but downward revisions to near-term core PCE inflation with tariff passthrough proving less severe than previously feared.

Aside from the Fed, we also receive two months worth of JOLTS data along with other delayed releases as the shutdown data backlog is slowly caught up.

AUDUSD TECHS: Bullish Impulsive Wave Extends

- RES 4: 0.6723 High Oct 21 ‘24

- RES 3: 0.6707 High Sep 17 and a key resistance

- RES 2: 0.6660 High Sep 18

- RES 1: 0.6649 Intraday high

- PRICE: 0.6630 @ 16:32 GMT Dec 5

- SUP 1: 0.6580/6533 High Nov 13 / 20-day EMA

- SUP 2: 0.6517 Low Nov 27

- SUP 3: 0.6466/21 Low Nov 26 / 21

- SUP 4: 0.6415 Low Aug 21 / 22 and a bear trigger

A strong impulsive bull wave in AUDUSD remains intact, having printed 10 consecutive sessions of higher highs. Recent gains have cleared a number of important short-term resistance points, strengthening a bull theme and highlighting scope for a continuation higher. Today’s rally has resulted in a breach of 0.6640, 76.4% of the Sep 17 - Nov 21 bear leg. This opens 0.6707, the Sep 17 high and key resistance. Key support to watch is at 0.6533, 20-day EMA.