POWER: EU End of Day Power Summary: CWE Rise on Temps, Energy Complex

CWE front-month power futures are rising on Tuesday with gains in the energy complex and a downward revision in temperature forecasts paired with forecasts for low wind generation. Nordic December power ended the session rangebound.

- Nordic Base Power DEC 25 down 0.1% at 62.7 EUR/MWh

- France Base Power DEC 25 up 3.1% at 69.44 EUR/MWh

- Germany Base Power DEC 25 up 1.1% at 103.3 EUR/MWh

- EUA DEC 25 up 1.3% at 82.24 EUR/MT

- TTF Gas DEC 25 up 2.1% at 32.42 EUR/MWh

- TTF has risen as the market weighs supply-demand fundamentals amid a downtrend in wind forecasts this week and through the weekend.

- EUAs Dec25 are rising to the highest levels since 11 February 2025, supported by continued bullish sentiment and TTF influence on the day with markets awaiting updates from the EU Environment Council meeting.

- The number of European PPAs signed so far this year has declined by 60% versus 2024 levels, while contracted capacity is down by 40% on the year.

- French hydropower reserves last week increased for the second consecutive week by 1.5 percentage points to 69.6% of capacity, narrowing the deficit to the five-year average and last year’s level.

- EdF has extended the unplanned outage at the 1.31GW Belleville 1 nuke to 10 November from 8 November.

- France’s CRE has awarded 129 projects for a total of 301MW of new rooftop solar PV capacity in the eleventh round at an average achieved price of €96.48/MWh.

- Swiss hydropower reserves last week declined by 0.3 percentage points to 77.9% of capacity, widening the deficit to the five-year average.

- Centrica has made an initial £376mn investment to acquire a 15% stake in the 3.2GW Sizewell C nuclear project, while EdF has announced the financial closing of the project.

- Italy has received 157 applications totalling 1.85GW for its first Net Zero Industry Act photovoltaic auction, with project rankings to be published by 15 December.

- Spain has approved a Royal Decree to strengthen the resilience and stability of the national electricity system by enhancing oversight, promoting energy storage and repowering, and accelerating electrification.

- Norway’s NVE has rejected the 800MW Davvi onshore wind farm in Finnmark due to environmental and cultural concerns, with stakeholders able to comment until 5 December.

- Planned works at the 500MW unit 2 at the 2GW Dukovany nuclear power plant in the Czech Republic have come to an end.

- Poland’s Energy Regulatory will hold the final 2025 auction for the cogeneration premium over 15-17 December, offering support for up to 15.7TWh from new and modernised CHP units.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Fresh Cycle High

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4045 3.0% Upper Bollinger Band

- RES 2: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 1: 1.3989 200-dma

- PRICE: 1.3953 @ 16:02 BST Oct 3

- SUP 1: 1.3897/3825 Low Sep 30 / 50-day EMA

- SUP 2: 1.3727 Low Aug 29 and a bear trigger

- SUP 3: 1.3689 Low Jul 28

- SUP 4: 1.3637 Low Jul 25

A bull cycle in USDCAD remains intact and yesterday’s break above the late September’s high, firms the bullish theme. This move higher also maintains the bullish price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 1.4019, a Fibonacci retracement point. On the downside, first key support lies at 1.3825, the 50-day EMA.

AUDUSD TECHS: Support Remains Intact For Now

- RES 4: 0.6763 1.382 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 3: 0.6726 1.236 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 2: 0.6660/6707 High Sep 18 / 17 and key resistance

- RES 1: 0.6629 High Sep 30 & Oct 01

- PRICE: 0.6603 @ 16:01 BST Oct 3

- SUP 1: 0.6527/21 61.8% of the Aug 21 - Sep 17 bull leg / Low Sep 26

- SUP 2: 0.6484 76.4% retracement of the Aug 21 - Sep 17 bull leg

- SUP 3: 0.6463/6415 Low Aug 27 / Low Aug 21 / 22 and a bear trigger

- SUP 4: 0.6373 Low Jun 23

The AUDUSD uptrend remains intact and recent weakness appears to have been a correction. Support to watch lies at the 50-day EMA, at 0.6558. A clear break of this average would signal scope for a deeper retracement and expose 0.6527 once again, a Fibonacci retracement. For bulls, a stronger reversal higher would refocus attention on 0.6707, the Sep 17 high. Initial resistance to watch is 0.6629, the Sep 30 and Oct 1 high.

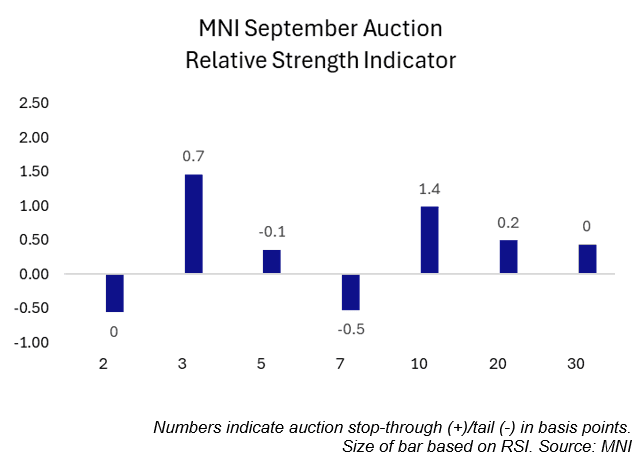

US TSYS/SUPPLY: September's Coupon Auctions Were Generally Solid (2/2)

September’s coupon auctions were generally solid, with three lines trading through, two coming out on the screws and two tailing slightly.

- Looking through the lens of MNI’s Relative Strength Indicator (RSI), five lines saw positive readings while two saw negative readings.

- The 3-year sale was the strongest auction of the month according to MNI’s RSI. The 3-year line traded through 0.7bps, the largest stop through in seven months. Meanwhile, the primary dealer take-up was just 8.4%, the lowest on record (data going back to 2003).

- The weakest sale of the month was the last – the 7-year line. This line saw the second consecutive 0.5bp tail, with the 12.0% primary dealer take-up above August’s 9.8% and July’s record low 4.1%.

September Auction Review:

- 2Y Note on-the-screws: 3.571% vs. 3.571% WI.

- 2Y FRN: 0.200% high margin vs. 0.195% prior

- 3Y Note trade-through: 3.485% vs. 3.492% WI.

- 5Y Note tail: 3.710% vs 3.709% WI.

- 7Y Note tail: 3.953% vs. 3.948% WI.

- 10Y Note trade-through: 4.033% vs. 4.047% WI.

- 10Y TIPS: 1.734% high yield vs. 1.985% prior

- 20Y Bond trade-through: 4.613% vs 4.615% WI.

- 30Y Bond on-the-screws: 4.651% vs. 4.651% WI.