POWER: EU End of Day Power Summary: CWE, Nordics Rise W/W

CWE front-month power futures are trading higher today, on track for a week-on-week increase, supported by gains in the energy complex. Nordic January power has also risen on the week on forecasts for a drier, cooler outlook and lower nuclear availabilities.

- Nordic Base Power JAN 26 up 3.2% at 65.05 EUR/MWh

- Germany Base Power JAN 26 up 1.2% at 103.07 EUR/MWh

- France Base Power JAN 26 up 1.1% at 72.82 EUR/MWh

- EUA DEC 25 down 0.2% at 83.7 EUR/MT

- TTF Gas JAN 26 up 3% at 27.6 EUR/MWh

- TTF front month has risen to the top end of its weekly range of €26.5/MWh to €27.7/MWh, amid cooler temperatures towards the end of December and into January, though temperatures are still seen above-normal for the majority of December.

- EUAs Dec25 are edging down today from the highest level since October 2023 in the previous session but remain on track for weekly gains of about 2%, supported by persistent bullish sentiment ahead of tightening supply in 2026.

- The EU installed 65.1GW of PV capacity in 2025, a 0.7% drop on the year, with projections now putting 2030 capacity at 718GW, short of the 750GW target, despite reaching 406GW of total capacity this year.

- EdF operations may be disrupted as workers launch a 24-hour strike from Monday evening, following a notice issued for 15–16 December.

- France’s nuclear regulator ASNR has cleared EdF’s 1.6GW Flamanville 3 nuke to boost output beyond 80% of its rated power, allowing the long-delayed reactor to continue ramp-up tests toward full operation.

- Ireland has lifted its de facto ban on new data centre grid connections in Dublin, allowing new projects to proceed if they can meet their own power needs and support the grid.

- Nordic spot prices are likely to be supported next week (week 51) as forecasts point to revised lower and cooler temperatures – albeit remaining above the seasonal average. Lower nuclear availability and a weakened hydro balance in Sweden are likely to weigh on Nordic reservoir levels and increase supply risk.

- Statnett has been fined NOK 1.5mn (€130,000) after failing to promptly disclose a major 1.44GW NordLink outage, a delay that regulators say undermined transparency in the power market.

- Planned works on the 723MW NorNed power link between Norway-Netherlands will occur on 15 December, with the unit fully disconnected for around 10Hrs.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Price Action Consistent with GBP Demand, USD Sales into 4pm London

USD reversal holds in recent trade, helping form a notable intraday reversal in the likes of EURUSD, USDCNH and - in particular - GBPUSD.

- Price action is consistent with some GBP buying and USD sales into the 4pm WMR fix, and while the rally in GBPUSD does put the pair close to 50 pips off intraday lows, the rally is still well short of AM highs into 1.3155 and yesterday's 1.3184.

- Futures volumes are consistent with a pick-up in interest for GBP as the spot rate recovered off lows - and the tail-off of activity as the rate stalls into 1.3140 further supports the view that the move was flow-related.

- We noted earlier today that dips in EURGBP remain well supported around the prior breakout level at 0.8769, highlighting the dominant uptrend. The next topside target remains at 0.8875, the April 2023 high.

FED: US TSY 17W AUCTION: NON-COMP BIDS $505 MLN FROM $69.000 BLN TOTAL

- US TSY 17W AUCTION: NON-COMP BIDS $505 MLN FROM $69.000 BLN TOTAL

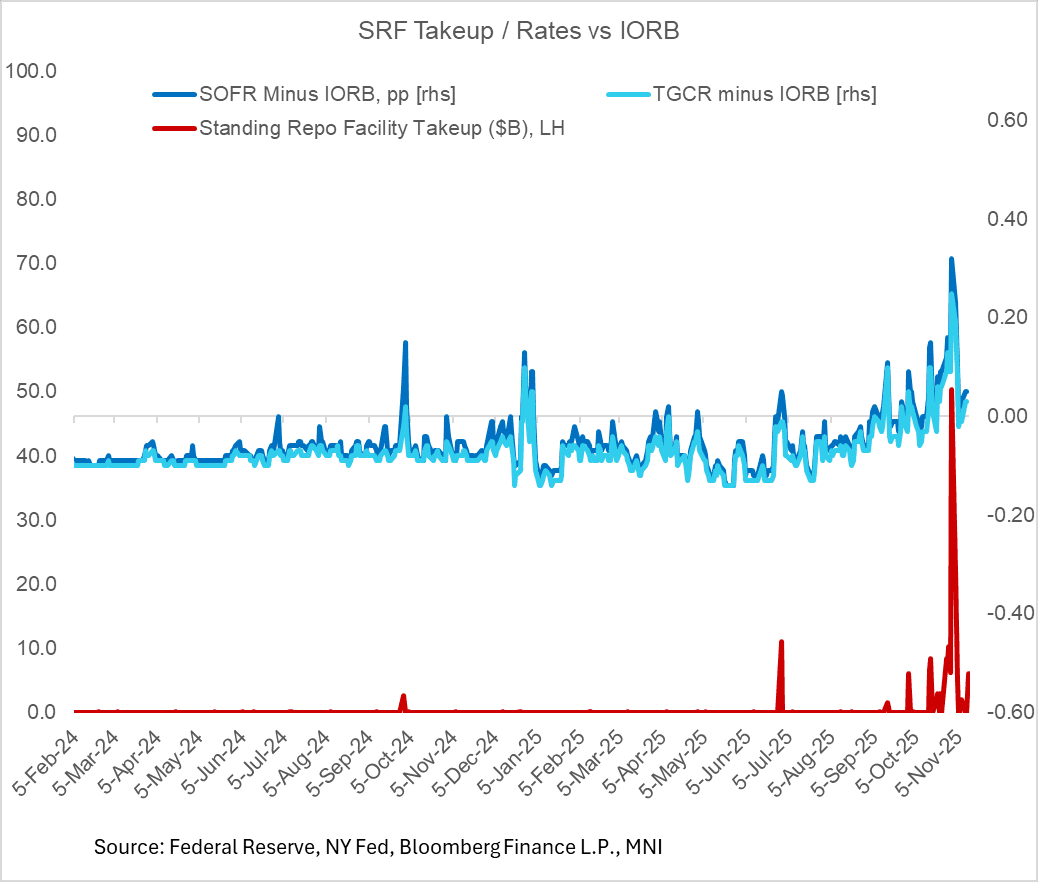

US TSYS/OVERNIGHT REPO: Secured Rates Ticked Up Monday, Set To Stay Elevated

Secured rates ticked up on Monday Nov 10 (data was published this morning by the NY Fed which alongside rate markets was closed Tuesday due to the Veterans Day holiday).

- SOFR rose 2bp (3.95%) with TGCR up 4bp (3.93%), marking the highest both in absolute terms and relative to the Fed's administered rates (notably IORB which is 3.90%) since Nov 4 when October month-end pressures looked to have been dissipating.

- We also note that takeup of the Fed's Standing Repo Facility came in at $6.05B in this morning's operation, already the highest for a full day since Nov 3.

- Additionally, Treasury bill settlement will raise $14B in new cash today and $23B Thursday, applying some upside pressure to funding rates.

- As such it doesn't look like there will be much relief in rates today.

- Effective Fed funds were unchanged at 3.87% Monday.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 3.95%, 0.02%, $3135B

* Broad General Collateral Rate (BGCR): 3.93%, 0.04%, $1234B

* Tri-Party General Collateral Rate (TGCR): 3.93%, 0.04%, $1214B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 3.87%, no change, volume: $77B

* Daily Overnight Bank Funding Rate: 3.87%, no change, volume: $161B