EMISSIONS: EU End-Of-Day Carbon Summary: EUAs/UKAs Track Weekly Gains

Sep-19 15:30

EUAs/UKAs Dec25 are tracking weekly gains, supported by strong EUAs auction prices amid sustained demand for physical allowances ahead of the end-of-month surrender deadline. EUAs/UKAs are edging lower on the day, weighed by losses in EU gas, with TTF falling after the EC’s announcement to phase out LNG

- EUA DEC 25 down 0.41% at 77.52 EUR/t CO2e

- UKA DEC 25 down 1.41% at 57.37 GBP/t CO2e

- TTF Gas OCT 25 down 2.3% at 32.18 EUR/MWh

- NBP Gas OCT 25 down 2.3% at 79.63 GBp/therm

- Estoxx 50 up 0.2% at 5467.72

- The latest Germany ETS CAP3 auction cleared at €76.57/ton CO2e, up 2.07% compared with the previous Germany auction at €75.02/ton CO2e according to EEX.

- Bullish conditions in ICE EUA futures remain intact and this week’s gains reinforce current conditions. Price also remains closer to its recent highs. The contract traded to a fresh cycle high on Wednesday, confirming a resumption of the uptrend and extending the bullish price sequence of higher highs and higher lows. Scope is seen for a move towards €78.73, a Fibonacci retracement. Key support to watch lies at €68.71, the May 30 low.

- Current EUAs spot price remains above market consensus for EUAs prices in Q3 2025, reflecting strong short-term upward momentum driven up by TTF and global equities volatility and physical demand ahead of the end-of-month surrender deadline.

- TTF front month has fallen with focus returning to immediate supply-demand pressures after the EC announced a faster phase out of Russian LNG in line with expectations today.

- 2024 Climate Targets - The EU Environment council made no material progress towards the finalisation of the 2040 climate target at its meeting on 18 September, with the next step being a 23 Sept vote on rapporteur Ondrej Knotek’s draft report rejecting the target.

- 2035 NDC - The EU Council approved a statement of intent on the 2035 nationally determined contribution (NDC), outlining an indicative 2035 target of 66.25–72.5% GHG emissions reduction versus 1990 levels. The next step will be communicating the statement to the UNFCCC Secretariat and the Paris Agreement Implementation and Compliance Committee, with full NDC submission planned ahead of COP30.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 17W AUCTION: NON-COMP BIDS $455 MLN FROM $65.000 BLN TOTAL

Aug-20 15:15

- US TSY 17W AUCTION: NON-COMP BIDS $455 MLN FROM $65.000 BLN TOTAL

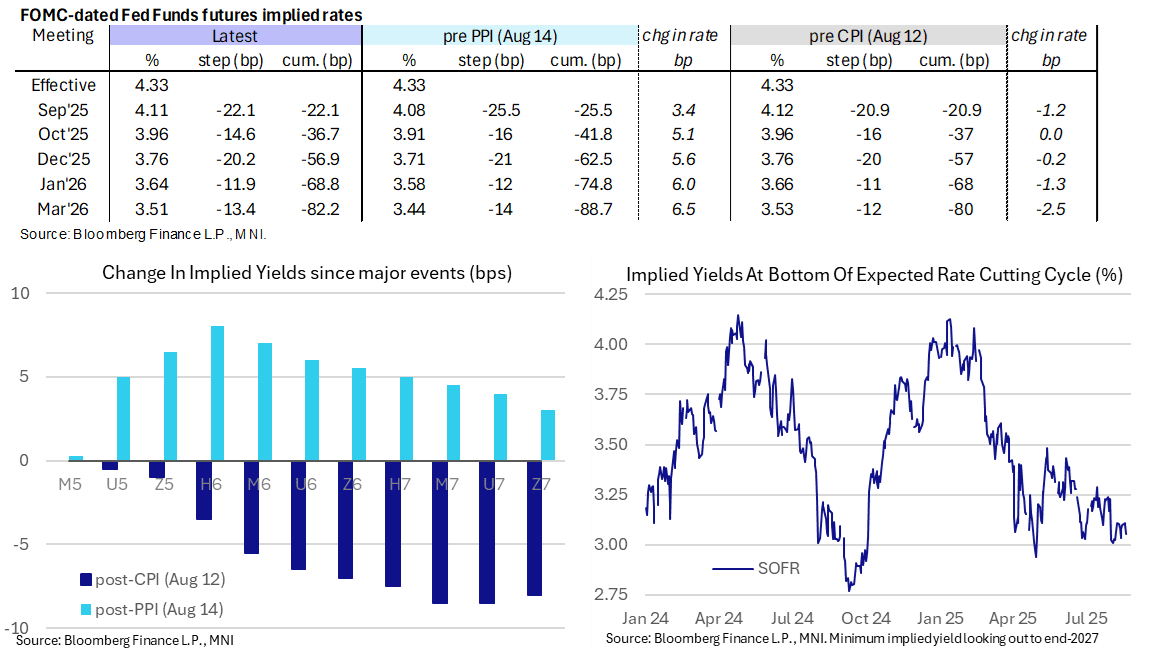

STIR: 2025 Rate Cut Prospects Build But Only Back To Pre-CPI Levels

Aug-20 15:13

- Rate cut prospects have increased on the two-prong nature of tech-led equity weakness and the WSJ reporting that Trump is considering firing Fed Governor Cook (a step up from his earlier Truth Social post urging her to resign).

- Fed Funds implied cumulative cuts from 4.33% effective: 22bp Sep, 36.5bp Oct, 57bp Dec, 69bp Jan and 82bp Dec.

- For context though, the 57bp of cuts to year-end is only back to levels seen shortly after Thursday’s strong PPI report and as such continues to have at least fully reversed the dovish impact from CPI earlier last week.

- Dovish implications are clearer to see further out the curve, with the SOFR implied terminal yield of 3.055% (SFRH7) now 4.5bp lower on the day (7.5bp lower than pre-CPI levels) after some narrow ranges in recent days.

- Terminal pricing does however keep to the 125bp +/-5bp of cuts from current levels range broadly seen since the Aug 1 payrolls report.

US TSY FUTURES: Extending Highs

Aug-20 15:10

- Mirroring late support in German Bund, Treasury futures continue to extend highs in late morning trade, weaker stocks (SPX eminis at 6377.5 -55.0) contributing to the move.

- Tsy Sep 10Y contract +7 at 111-31.5 session high, initial technical resistance at 112-15.5 (High Aug 5 and the bull trigger).

- Curves have reversed early flattening to steeper: 2s10s +.237 at 55.847, 5s30s +1.491 at 109.733.

- Focus on this afternoon's July FOMC minutes release at 1400ET.