EMISSIONS: EU End-Of-Day Carbon Summary: EUAs/UKAs Rise On TTF Gains

EUAs/UKA Dec25 are both rising to 10-day highs, supported by rally in EU gas, with TTF rising to the highest level since 6 Aug amid upcoming seasonal maintenance in Norway and ongoing uncertainty over progress towards ceasefire in Ukraine. Meanwhile, EU ad UK equities losses are limiting carbon gains, with STOXX declining as energy and industrials were the only sectors in the green today. Eurozone August manufacturing PMI was higher than expected at 50.5 (49.5 exp), while UK manufacturing PMI was a point lower than expected at 47.3 (48.3 exp).

- EUA DEC 25 up 1.84% at 72.6 EUR/t CO2e

- UKA DEC 25 up 2.58% at 52.14 GBP/t CO2e

- TTF Gas SEP 25 up 3.8% at 33.12 EUR/MWh

- NBP Gas SEP 25 up 4.2% at 82.36 GBp/therm

- Estoxx 50 down 0.2% at 5459.2

- The latest EU ETS CAP3 auction cleared at €71.19/ton CO2e, down 0.25% compared with the previous EU auction at €71.37/ton CO2e according to EEX.

- EUA Auction Calendar Week Ahead (Calendar Week 35) - A total of 11.4mn EUAs will be auctioned next week, with 4 auction sessions will be held. The latest EU ETS auction cleared at €71.19/ton CO2e, up 0.92% w/w, rising above the 10, 50 and 100-day averages.

- EUA Dec25 implied volatility stood at 27.99% as of 20 August, marking a three-week low and falling below the 30-day average. Volatility declined after hitting a record high of 28.70% on 18 Aug, while EUA Dec25 prices edged down by 0.74% and open interest remained at a similar level over the same period.

- TTF front month continues to rally from the low at the start of the week supported by upcoming seasonal maintenance in Norway amid ongoing uncertainty over progress towards is ceasefire in Ukraine.

- EU PMI - Overall, the Eurozone PMI data underscores the ECB's view that policy is in a "good place” but isn't enough to significantly dampen expectations for one more 25bp cut this cycle.

- UK PMI – The UK composite PMI is another release that is marginally higher than expected and therefore not supportive of a near-term cut, following last week's labour market report and yesterday's inflation release.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

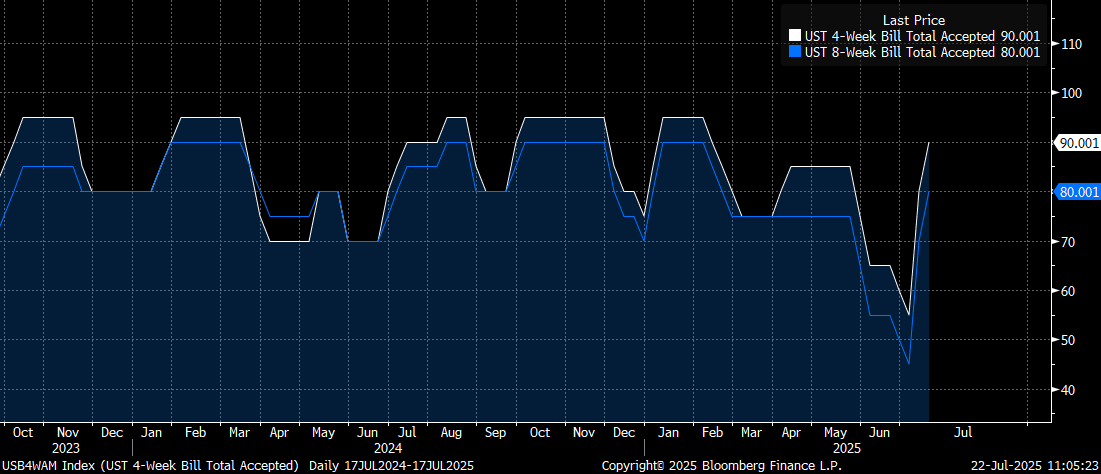

US TSYS/SUPPLY: Treasury Ups Bill Sizes Again As Cash Rebuild Picks Up Pace

Treasury continued to up the size of 4- and 8-week bills, rising $5B apiece for Thursday's auctions to $95B and $85B, respectively. The new 4-week level will match the all-time largest auctions seen over the last couple of years, with 8-weeks remaining below the $90B peak.

- This is the 3rd consecutive weekly increase - they're up from $55B/$45B at the beginning of the month, prior to the lifting of the debt limit. 17-week auction sizes were unchanged at $65B.

- The increase is something of a surprise (Wrightson ICAP this morning wrote "We think the Treasury has completed its current ramp-up of bill offering sizes"), in a possible sign that Treasury is not necessarily going to back-load its rebuild of the Treasury General Account post-debt limit: it said after the debt limit was lifted that it is aiming for a cash balance of $500B by end-July (vs $315B at end-last week) and $850B by end-September.

- Upon settlement next Tuesday, the bills will raise $60B in net cash.

- We expect to hear a little more about cash management plans in next week's Refunding round. For the foreseeable future, bills are going to be the moving part in meeting financing requirements, with coupon auction sizes not expected to be increased for several quarters at least. We'll publish our Refunding preview later this week.

US 10YR FUTURE TECHS: (U5) Monitoring Resistance

- RES 4: 112-15 61.8% retracement of the Apr 7 - 11 sell-off

- RES 3: 112-12+ High Jul 1 and a bull trigger

- RES 2: 111-28 High Jul 3

- RES 1: 111-13+ High Jul 21 & Jul 10

- PRICE: 111-11+ @ 16:10 BST Jul 22

- SUP 1: 110-08+ Low Jul 14 & 16

- SUP 2: 110-03 76.4% retracement of the May 22 - Jul 1 bull leg

- SUP 3: 109-28 Low Jun 6 and 11

- SUP 4: 109.25 Low May 27

Treasury futures traded higher again Tuesday, extending the firm start to the week. The move higher has resulted in a break of the 20-day EMA, strengthening the recovery, and markets have met resistance at 111-13+, the Jul 10 high. A clear break of this hurdle would highlight a stronger reversal. Key support lies at 110-08+, the low on Jul 14 and 16. A move through this support would reinstate the recent bearish theme.

BELGIUM AUCTION PREVIEW: On offer next week

Belgium will look to sell the following OLOs at its auction next Monday, with the target size set to be announced on Friday:

- the 2.60% Oct-30 OLO

- the 3.10% Jun-35 OLO

- the 3.50% Jun-55 OLO