EMISSIONS: EU End-Of-Day Carbon Summary: EUAs/UKAs Fall On Weaker EUAs Auction

Sep-25 15:32

EUAs/UKAs Dec25 are edging down, weighed by a weaker EUAs auction result, as buying momentum eases with the surrender deadline approaching. EUAs Dec25 have declined nearly 3% since hitting a seven-month high on 18 September, bringing month-to-date gains to 3.7%. Using the highest-performing September in the past five years as a benchmark, which saw month-on-month gains of 1.6% in 2021, a potential downside risk remains for the rest of the month.

- EUA DEC 25 down 0.43% at 75.69 EUR/t CO2e

- UKA DEC 25 down 1.34% at 56.08 GBP/t CO2e

- TTF Gas OCT 25 up 2% at 32.555 EUR/MWh

- NBP Gas OCT 25 up 2.3% at 81.35 GBp/therm

- Estoxx 50 down 0.3% at 5447.06

- The latest EU ETS CAP3 auction cleared at €75.56/ton CO2e, down 0.05% compared with the previous EU auction at €75.6/ton CO2e according to EEX.

- EUA Auction Calendar Week Ahead (Calendar Week 40) - A total of 20.2mn EUAs will be auctioned next week, with 5 auction sessions will be held. The latest EU ETS auction cleared at €75.56/ton CO2e, down -2.15% w/w, falling below the 10-day average for the first time since 20 Aug, indicating a downward pressure as buying momentum eases with the surrender deadline approaching.

- Bullish conditions in ICE EUA futures remain intact and the latest pullback appears corrective. A fresh cycle high last week confirmed a resumption of the uptrend and an extension of the bullish price sequence of higher highs and higher lows. Moving average studies are in a bull-mode position highlighting a dominant uptrend. Scope is seen for a move towards €78.73, a Fibonacci retracement. Key support to watch lies at €68.71, the May 30 low.

- TTF front month is higher but remains within its recent range amid cool weather and recovering Norwegian pipeline supplies

- Renewables intermittency and increased power hedging ahead of the upcoming winter, alongside rising participation in EU ETS, could provide support to EUAs prices, according to BNEF.

- During the UN Climate Summit yesterday, the EU announced the bloc’s “statement of intent” for its 2035 NDC target, pledging to set a reduction target of 66–72% versus 1990 levels, and promising to formally submit it before COP30 in November. The announcement was no surprise, as the statement had already been agreed among member states on 19 September.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: Midday September'25-December'25 Roll Update: 70%-80% Complete

Aug-26 15:27

Latest Tsy quarterly futures roll volumes from September'25 to December'25 below. Percentage complete currently 70%-80% ahead "First Notice" date this Friday, August 29. Current roll details:

- TUU5/TUZ5 appr 1,266,500 from -9.12 to -8.75, -9.0 last; 80% complete

- FVU5/FVZ5 appr 1,528,800 from -5.5 to -5.0, -5.25 last; 70% complete

- TYU5/TYZ5 appr 926,800 from -1.25 to -0.5, -0.75 last; 71% complete

- UXYU5/UXYZ5 app 550,300 from -0.25 to +0.5, 0.00 last; 72% complete

- USU5/USZ5 appr 312,600 from 12.0 to 12.75, 12.25 last; 79% complete

- WNU5/WNZ5 appr 435,700 from 7.0 to 8.25, 7.75 last; 74% complete

- Reminder, Sep futures don't expire until next month: 10s, 30s and Ultras on September 22, 2s and 5s on September 30.

OPTIONS: Larger FX Option Pipeline

Aug-26 15:16

- EUR/USD: Aug29 $1.1600(E1.3bln), $1.1625(E4.0bln), $1.1700(E1.1bln), $1.1725(E1.1bln)

- USD/JPY: Aug29 Y146.50($1.1bln)

- EUR/GBP: Aug29 Gbp0.8563-80(E2.0bln)

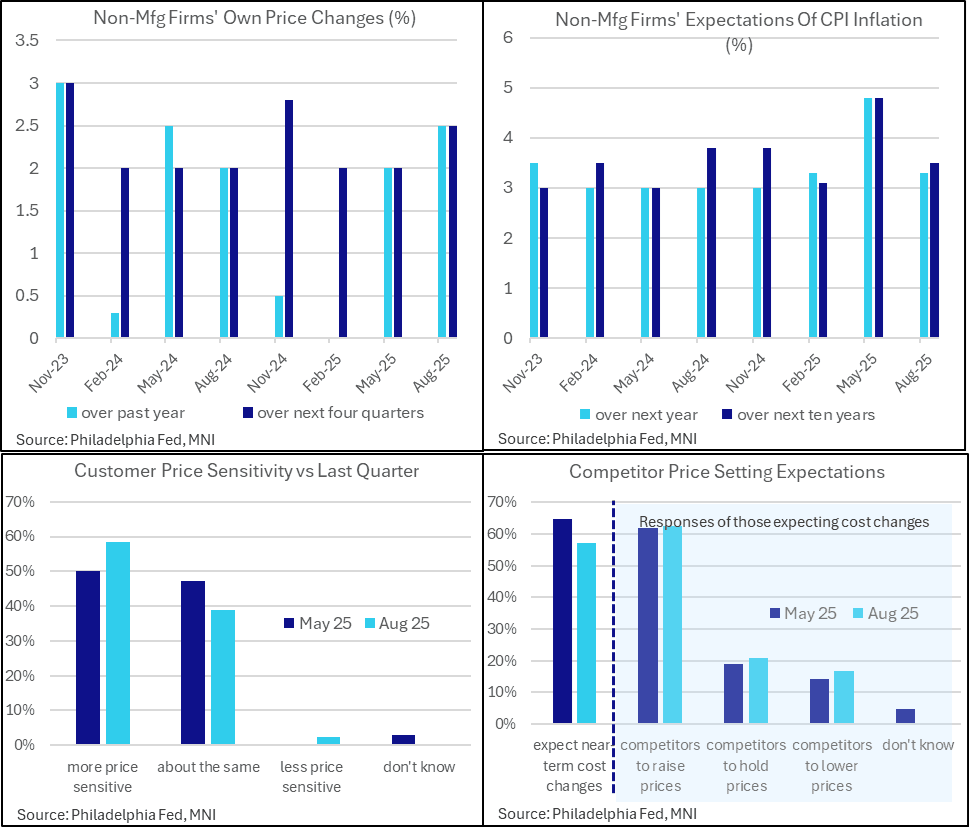

US DATA: Philly Non-Mfg Firms See Faster Price Increases Despite Sensitivity

Aug-26 15:08

- The Philly Fed non-manufacturing survey special questions on inflation expectations show a somewhat similar split in the activity indexes touched upon earlier with their historically large discrepancy between strong firms’ own activity and weak regional activity in August.

- The median firm reported increasing its own prices by 2.5% over the past year, up from 2.0% in the May question and having essentially paused annual price increases through end 2024/early 2025. It’s the strongest actual increase since the May 2024 survey.

- Own price expectations also firmed from 2.0% to 2.5%, above a typical median of 2% in surveys over the past almost two years but not an unprecedented level.

- Firms’ expectations of consumer inflation meanwhile cooled from a particularly strong May release, with those for the next year reverting to 3.3% from 4.8%. Ten-year ahead expectations also cooled to 3.5% after 4.8%, still above the 3.1% in February prior to reciprocal tariff announcements but within ranges.

- Elsewhere, these non-manufacturing firms reported greater price sensitivity over the quarter (59% reported higher sensitivity vs 50% in May) and fewer expect cost changes over the near-term (57% vs 65%). Of those that do expect cost increases, a similar almost two thirds expect those to be higher, with price changes over a median 3 months vs 2.5 months in the May survey.