EMISSIONS: EU End-Of-Day Carbon Summary: EUAs Track Weekly Losses, UKAs Gain

{EU}{EUAs Dec25 are falling today and on track for a weekly decline of near 1%, weigh by EU equities and TTF losses, fallen below all 10, 50, 100-day average simultaneous for the first time since 1 July, suggest that bearish momentum is strengthening and that further downside may be possible in the near term if the market failed to identify upside catalyst. UKAs Dec25 are set for a weekly gain of 3.60%, supported by buying interest after headline of potential progress on linking the EU and UK ETS schemes reported earlier in the week. However, some gains were trimmed today, likely due to profit-taking by long holders after prices hit a three-week high on Wed.

- EUA DEC 25 down 0.55% at 70.16 EUR/t CO2e

- UKA DEC 25 down 3.1% at 49.4 GBP/t CO2e

- TTF Gas AUG 25 down 2.3% at 33.615 EUR/MWh

- NBP Gas AUG 25 down 2.1% at 80.34 GBp/therm

- Estoxx 50 down 0.4% at 5356.76

- The latest Germany ETS CAP3 auction cleared at €69.68/ton CO2e, up 0.55% compared with the previous Germany auction at €69.3/ton CO2e according to EEX.

- TTF front month declined today on lower forecasted temperatures in Europe and higher Norwegian flows today, alongside a reduced appetite for LNG in Asia amid cooling temperatures.

- LEBA OTC physically delivered EUAs volumes in June 2025 were at 182Mt, up 27% m/m but down 3.2% y/y. Meanwhile, UKA volumes were at 26.3Mt, up 12% m/m and 123% y/y.

- The EU Commission has unveiled its budget proposal for the 2028-2034 period, which includes plans to incorporate revenues from the EU ETS and CBAM into the bloc’s budget, it said.

- Serbia has called for a phased introduction of the EU’s CBAM to avoid economic disruption, according to SeeNews.

- INEOS has achieved a 75% reduction in emissions at its Hull manufacturing site following the completion of a £30mn hydrogen conversion project, it said.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

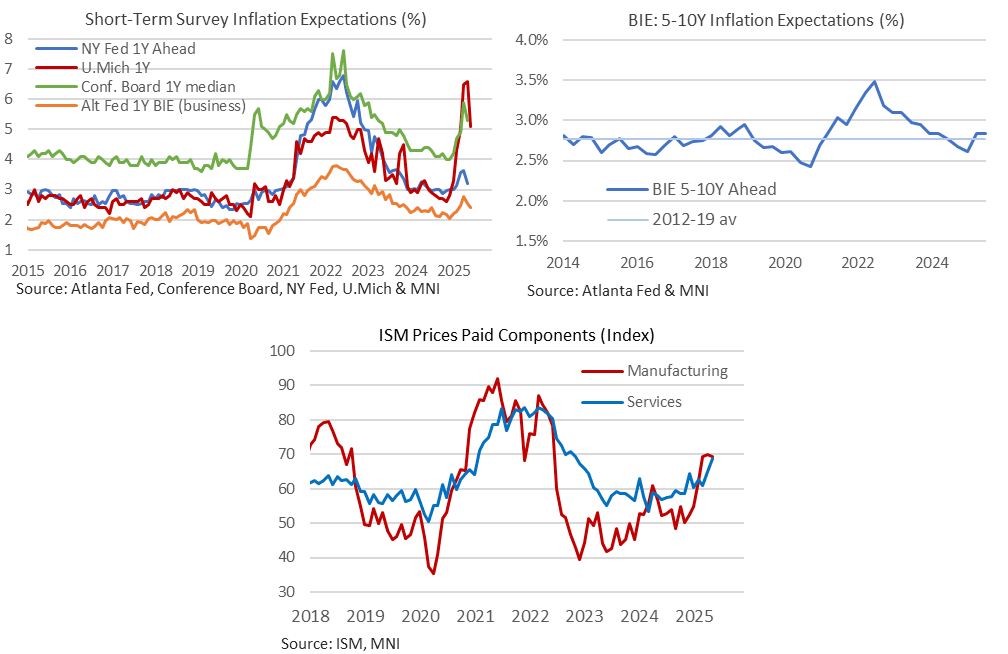

US DATA: Business Inflation Expectations Contained In June – Atlanta Fed

The Atlanta Fed’s Business Inflation Expectations survey for June (in-depth report, here) continued to show relatively modest impacts from US tariff policy.

- Firms’ 1Y ahead inflation expectations, defined in the details as the mean change in expected unit costs over the next 12 months, fell to 2.42% in June from 2.54% in May.

- It’s down from a recent high of 2.76% in April (highest since Jul 2023) for the lowest since February but still a little above the 2.24% averaged in 2024 for context.

- The increase and subsequent pullback is more in keeping with a modest increase in consumer expectations from the NY Fed’s survey as opposed to the sharper climbs in the U.Mich survey and less so Conference Board survey.

- This release also sees the quarterly question for firms’ long-run unit cost inflation expectations 5-10Y ahead, with it unchanged at 2.8% from the March survey. It’s up from Q4 low of 2.6% (lowest since 3Q20) but has only increased back to the 2.8% averaged since the survey started in 2012 through 2019.

- The combination points to a more mellow uptick in inflation expectations compared to sharper increases in prices paid components of ISM manufacturing and services surveys as of May.

FED: US TSY 8W BILL AUCTION: HIGH 4.470%(ALLOT 16.95%)

- US TSY 8W BILL AUCTION: HIGH 4.470%(ALLOT 16.95%)

- US TSY 8W BILL AUCTION: DEALERS TAKE 48.72% OF COMPETITIVES

- US TSY 8W BILL AUCTION: DIRECTS TAKE 9.12% OF COMPETITIVES

- US TSY 8W BILL AUCTION: INDIRECTS TAKE 42.16% OF COMPETITIVES

- US TSY 8W BILL AUCTION: BID/CVR 2.70

FED: US TSY 4W BILL AUCTION: HIGH 4.060%(ALLOT 48.91%)

- US TSY 4W BILL AUCTION: HIGH 4.060%(ALLOT 48.91%)

- US TSY 4W BILL AUCTION: DEALERS TAKE 18.15% OF COMPETITIVES

- US TSY 4W BILL AUCTION: DIRECTS TAKE 2.93% OF COMPETITIVES

- US TSY 4W BILL AUCTION: INDIRECTS TAKE 78.92% OF COMPETITIVES

- US TSY 4W AUCTION: BID/CVR 3.15