EMISSIONS: EU End-Of-Day Carbon Summary: EUAs Track Weekly Losses

{EEUAs/UKAs Dec25 are on track for weekly losses of 0.28% and gains of 1.08%, influenced by heightened trade tensions between the US and China and TTF volatility. EUAs/UKAs Dec25 are trending lower, weighed by losses in EU gas and equities. TTF is declining after Trump announced plans to hold a second meeting with Putin, while STOXX are down amid concerns over the US credit market.

- EUA DEC 25 down 0.28% at 79.29 EUR/t CO2e

- UKA DEC 25 down 0.42% at 56.24 GBP/t CO2e

- TTF Gas NOV 25 down 1.7% at 31.84 EUR/MWh

- NBP Gas NOV 25 down 2% at 80.76 GBp/therm

- Estoxx 50 down 0.6% at 5616.7

- The latest German EUA CAP3 auction cleared at €77.99/ton CO2e, compared with €79.22/ton CO2e in the previous auction on 10 October according to EEX.

- EUA Dec25 options implied volatility as of 16 Oct rebounded from the all-time low recorded earlier in the month, while put options open interest rose, signalling rising expectations for price swings and demand for downside protection.

- The uptrend in ICE EUA futures remains intact and recent weakness appears to have been a correction. Support to watch lies at the 50-day EMA, at €75.91. A clear break of this average would signal scope for a deeper corrective pullback. For bulls, sights are on €80.37, the Oct 10 high and a bull trigger. Clearance of this hurdle would confirm a resumption of the uptrend and open €82.12.

- Germany’s environment ministry, Jochen Flasbarth, has suggested extending the EU ETS beyond 2039, potentially up to 2045, without increasing the total emissions cap, according to Politico.

- A group of EU member states, led by Cyprus and several central and eastern European countries, plan to urge EU Commission to postpone the launch of the EU ETS 2 from to 2030 from 2027, according to Bloomberg.

- The ECB's projections currently pencil in HICP inflation at 1.9% in 2027, a tenth below the 2% target. That forecast is being pushed up because of the introduction of the EU ETS2. Without this policy, inflation would be even further below the 2% target.

- The US has motioned to suspend voting on the IMO Net Zero Framework (NZF) at today’s Marine Environment Protection Committee (MEPC) meeting, following President Trump urging member states to vote against it on Truth Social after market close yesterday, according to Bloomberg.

- TTF front month has pulled back from a high of €32.73/MWh and is net relatively unchanged on the week with steady fundamentals set against the forecast of colder weather in the last week of October.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

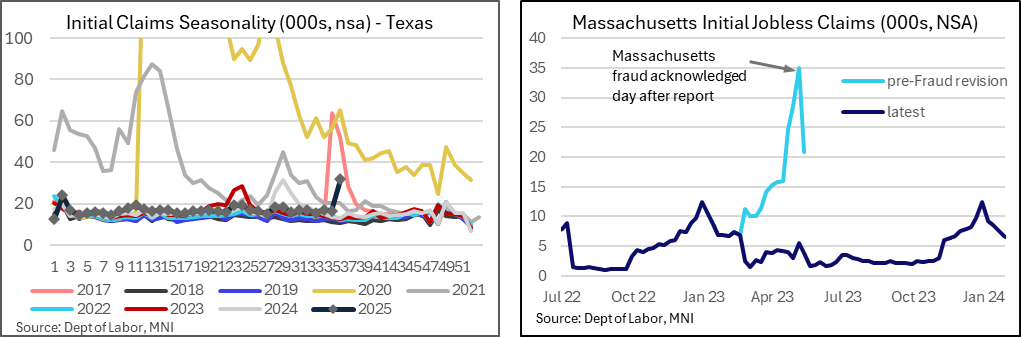

US LABOR MARKET: Massachusetts Lessons For Texas Jobless Claims Fraud

With the rise in Texas initial jobless claims directly linked to ID fraud, we revisit the Massachusetts example from back in May 2023 which saw subsequent revisions to the series two weeks after being first officially recognized. These revisions came outside of the regular claims publication (albeit only by a few minutes) which makes it hard to predict when we might hear something for Texas. Tomorrow’s claims report will no doubt see particular focus on this front but the issue could remain outstanding.

- As noted yesterday, the Texas Workforce Commission indicated that the rise in initial claims was “directly related to an increased volume of fraudulent claim attempts… Since Labor Day, we’ve observed an uptick in ID fraud claim attempts” (cited by Axios, link).

- Recall that last week’s jobless claims release surprisingly jumped to a seasonally adjusted 263k (cons 235k) as the non-seasonally level of claims in Texas increased 15.3k vs 7.9k nationally.

- Axios added that: "The Labor Department did not respond to questions about whether Texas communicated that the fraud issue inflated its claims - and if so, why it was not flagged in the public release." We aren’t surprised by the latter, with it taking some time for fraud in Massachusetts in 2023 to first be acknowledged and then corrected.

- Back in May 2023, national initial jobless claims surprisingly jumped to a seasonally adjusted 264k (cons 245k) in the week to May 6, with Massachusetts accounting for 6.4k of the 14k increase in the national non-seasonally adjusted level as MA continued some sizeable weekly increases. It saw the outright level increase to 34.9k (second only to California’s 46k despite a population less than a fifth of its size).

- The next day (May 12 after the May 11 publication), MA said that the increase was due to fraud attempts.

- However, it wasn’t until May 25 that MA released significant revisions just a few minutes before the publication of the regular claims release. What was seen as the peak 35k initially (before a 14k drop to 21k the week after) was subsequently revised down to 5.5k (and 3.8k).

- Sizeable revisions went back almost three months, although when it comes to Texas, the explicit reference to Labor Day suggests a more limited lookback to the roughly three weeks to Sep 1. Another difference this time is the sudden pop higher for Texas vs the more concerted build in MA.

SOFR OPTIONS: UPDATE BLOCK/Screen: Short Dec'25 SOFR Call Spread

- -50,000 0QZ5 97.00/97.25 call spds, 10.0

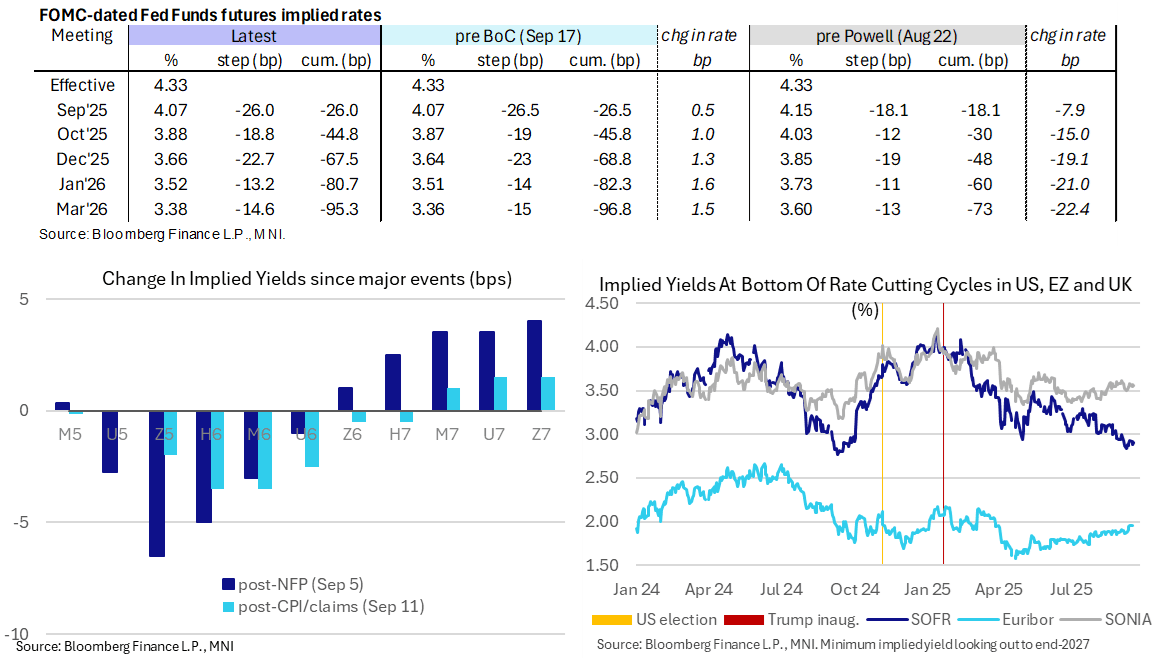

STIR: Modest Hawkish Tilt Post-BoC In Fed Rates, 26bp Cut Priced For Today

- US rates have seen a steady hawkish adjustment in BoC spillover, starting with the decision before an extension on Macklem’s press release noting that governing council considered leaving rates unchanged and not seeing a recession.

- Moves are contained though ahead of the FOMC decision at 1400ET, not least with the BoC having seen a clear consensus to cut 25bps and there being more comfort that some upward pressures on underlying inflation are easing off.

- Fed funds implied rates are 1.5bp higher since the decision through Dec-Mar meetings, whilst SOFR future implied yields are up to 2.5bps higher in late 2027 contracts (for +4bp on the day).

- Cumulative cuts from 4.33% effective: 26bp for today, 45bp Oct, 67.5bp Dec, 80.5bp Jan and 95.5bp Mar.

- SOFR implied terminal yield at 2.91% (SFRH7, +3bp) to shift back towards the higher end of its post-payrolls range roughly between 140-150bp of cuts from current levels.