EMISSIONS: EU End of Day Carbon Summary: EUA, UKAs Recover

Oct-09 15:22

EUAs and UKAs are edging higher in the European afternoon, after holding onto losses for most of the session. This is despite losses in EU gas and equities as well as relatively bearish short-term fundamentals.

- EUA DEC 25 up 0.3% at 79.23 EUR/MT

- ICE UKA Dec25 up 0.1% at 55.06 GBP/MT

- NBP Gas NOV 25 down 0.8% at 83.01 GBp/therm

- TTF Gas NOV 25 down 0.9% at 32.39 EUR/MWh

- Rotterdam Coal NOV 25 down 0.4% at 90.85 USD/MT

- TTF front month gives up some of the gains from the start of the week amid lower geopolitical risks following news that an agreement has been reached between Israel and Hamas. Fundamentals remain steady with supply risks weighing Ukrainian gas infrastructure disruption and delayed LNG cargoes to Egypt amid weak demand.

- The latest month-ahead ECMWF weather forecast for NWE has been revised up to. Mean temperatures are forecast to be broadly in line with the average this week, with slightly cooler temperatures next week, before rising back up.

- TTF front month gives up some of the gains from the start of the week amid lower geopolitical risks following news that an agreement has been reached between Israel and Hamas. Fundamentals remain steady with supply risks weighing Ukrainian gas infrastructure disruption and delayed LNG cargoes to Egypt amid weak demand.

- The latest EU ETS CAP3 auction cleared at €77.95/ton CO2e, down from €78.3/ton CO2e in the previous round on 7 October.

- Germany’s government has agreed on new incentives worth a total of €3 billion through 2029 to help low- and middle-income households purchase EVs.

- The German coalition government aims to agree on a common stance regarding the upcoming 2035 combustion engine ban.

- Austria has joined Germany in urging the European Union to extend the planned phase-out of EU ETS allocations, Austria’s Economy Minister Wolfgang Hattmannsdorfer said.

- Zero Waste Europe is urging the EU to adopt a cap-and-trade system for residual waste, aiming to cut per-capita waste and reduce GHG emissions.

- Latvia’s climate and energy ministry said on Wednesday it had again delayed adopting the EU emissions trading scheme’s requirements as part of the “On Pollution” Law.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Extending Lows

Sep-09 15:07

- Treasuries are extending lows at the moment, no particular headline or Block driver as many ply the sidelines ahead of CPI/PPI data next two sessions.

- Currently, the Dec'25 10Y trades -10 at 113-07.5 (yld 4.0856 +.0458) -- Initial firm support to watch is 112-11+, the 20-day EMA.

- Curves bear flattening: 2s10s -0.971 at 54.171, 5s30s -0.249 at 112.703.

- US$ gaining, BBG index BBDXY currently +1.51 at 1200.06 vs. 1196.69 post data low.

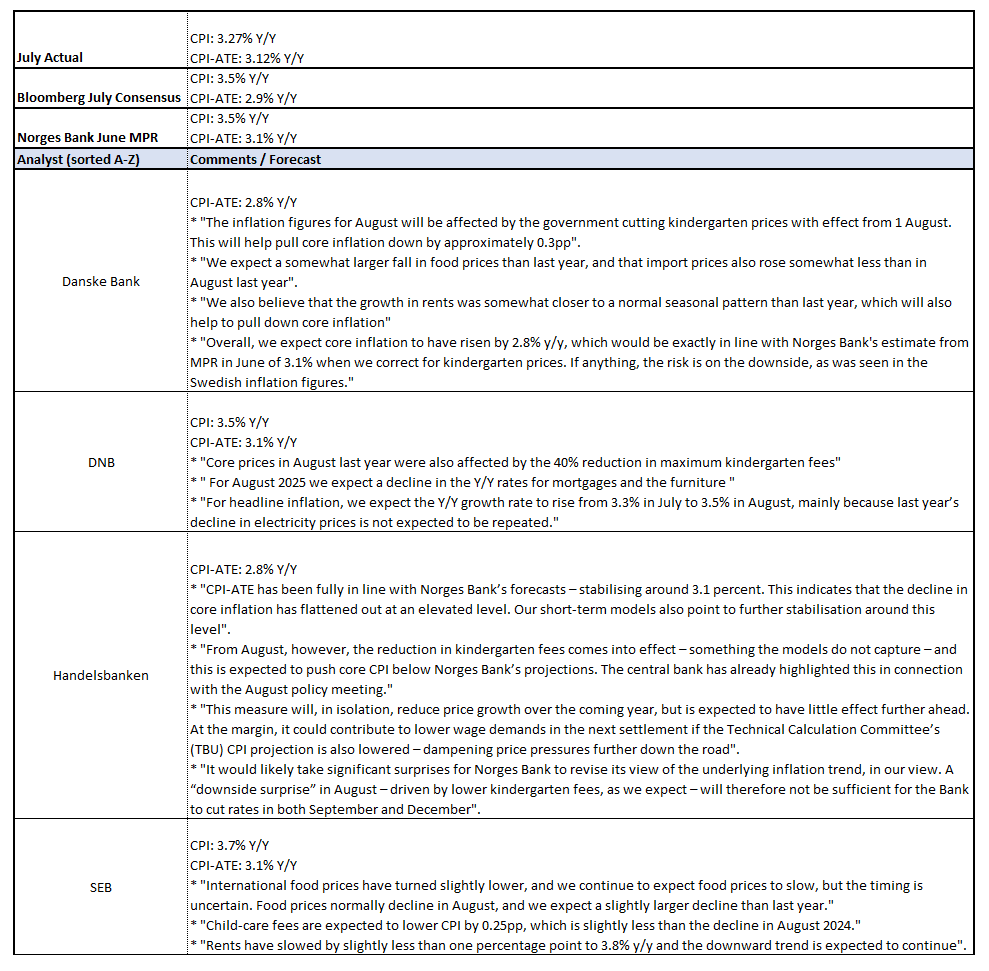

NORWAY: Preview: August Inflation Due At 0700BST/0800CET Tomorrow

Sep-09 15:01

Norwegian August inflation is due tomorrow at 0700BST/0800CET. Together with Thursday’s Q3 Regional Network Report, the data will be key in determining whether Norges Bank can deliver another 25bp cut on September 18.

- At its June and August decisions, Norges Bank Governor Wolden Bache said that the June MPR rate path was consistent with “one or two” more rate cuts this year (with implied probabilities skewed towards the quarterly MPR meetings in September and December). These comments keep the door open to a rate hold in September if this week’s data surprise in a hawkish direction – a risk markets may be underappreciating at present.

- Norges Bank’s June MPR projections for CPI-ATE are on track after two consecutive 3.1% Y/Y prints in June and July. In August, there are downside risks to the 3.1% Y/Y Norges forecast due to a reduction in child daycare prices in the 2025 Revised National Budget. From Norges Bank’s August monetary policy assessment: “Child daycare prices were reduced from 1 August 2025 and will thus be lower than assumed in the June Report. The reduction in child daycare prices will lead to lower 12-month inflation in the coming year and a modest improvement in household purchasing power but will probably have little impact on inflation further out”. That suggests Norges Bank are happy to look through the temporary policy change.

- The median analyst expects CPI-ATE inflation at 2.9% Y/Y in August, with forecasts ranging from 2.8-3.1%. A 3.1% Y/Y reading probably isn’t enough to derail a September cut just yet, but any higher and we think doubts should be increased - particularly if the Regional Network Survey is also hawkish.

- Alongside the daycare price impact, analyst previews we have seen generally expect a softening in food and rent inflation in August.

- Headline inflation is seen accelerating on an electricity base effect to 3.5% Y/Y (vs 3.3% prior), in line with Norges Bank projections.

MNI EXCLUSIVE: Senior European Commission energy analyst gives his view

Sep-09 14:56

Senior European Commission energy analyst gives his view on medium-term energy market trends.-- On MNI Policy MainWire now, for more details please contact sales@marketnews.com