EMISSIONS: EU End-Of-Day Carbon Summary: Carbon Rise On EU Gas, Equities Gains

Sep-04 15:26

EUAs/UKAs Dec25 are rising, supported by gains in EU equities and gas, with the STOXX advancing following comments from French President Macron on avoiding a snap election, while traders resumed betting ahead of a key payrolls report on Friday

- EUA DEC 25 up 0.68% at 75.46 EUR/t CO2e

- UKA DEC 25 up 1.94% at 55.7 GBP/t CO2e

- TTF Gas OCT 25 up 1.3% at 32.53 EUR/MWh

- NBP Gas OCT 25 up 1.3% at 79.47 GBp/therm

- Estoxx 50 up 0.4% at 5347.34

- The latest EU ETS CAP3 auction cleared at €74.38/ton CO2e, up 1.20% compared with the previous EU auction at €73.5/ton CO2e according to EEX.

- EUA Auction Calendar Week Ahead (Calendar Week 37) - A total of 16.8mn EUAs will be auctioned next week, with 4 auction sessions will be held. The latest EU ETS auction cleared at €74.38/ton CO2e, up 4.50% w/w, rising to the highest level since mid-June and standing above the 10, 50 and 100-day averages.

- Traders Position For Further EUAs Upsides - EUA Dec25 is positioned for further upsides, as downside protection grows cheaper and call interest rises, with the put/call open interest ratio declining and the call‑put volatility skew touching a seven-month low. Meanwhile EUA Dec25 prices edged up 4.36% w/w and open interest up 1.04% as of 3 Sep.

- Bullish conditions in ICE EUA futures remain intact and this week’s gains reinforce current conditions. Key short-term resistance at 73.35, the Jul 30 and Aug 8 high, has been cleared. This highlights a bullish development and signals scope for an extension towards €76.75, the Jun 13 high and a key medium-term resistance. Support to watch lies at €68.71, the May 30 low. A clear breach of this level would reinstate a bearish theme.

- BNEF said that following the new 15% US tariff on the EU, if EU industrial demand weakens due to slowing trade, a 2.5% emissions cut by 2035 would lower the average EUA price forecast by €25/t to €84/t by 2030.

- TTF is slightly higher today but withing the €31.4/MWh to €32.7/MWh range seen so far this week, with higher LNG imports helping to cover during the current Norwegian maintenance season.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 52W AUCTION: NON-COMP BIDS $1.116 BLN FROM $50.000 BLN TOTAL

Aug-05 15:15

- US TSY 52W AUCTION: NON-COMP BIDS $1.116 BLN FROM $50.000 BLN TOTAL

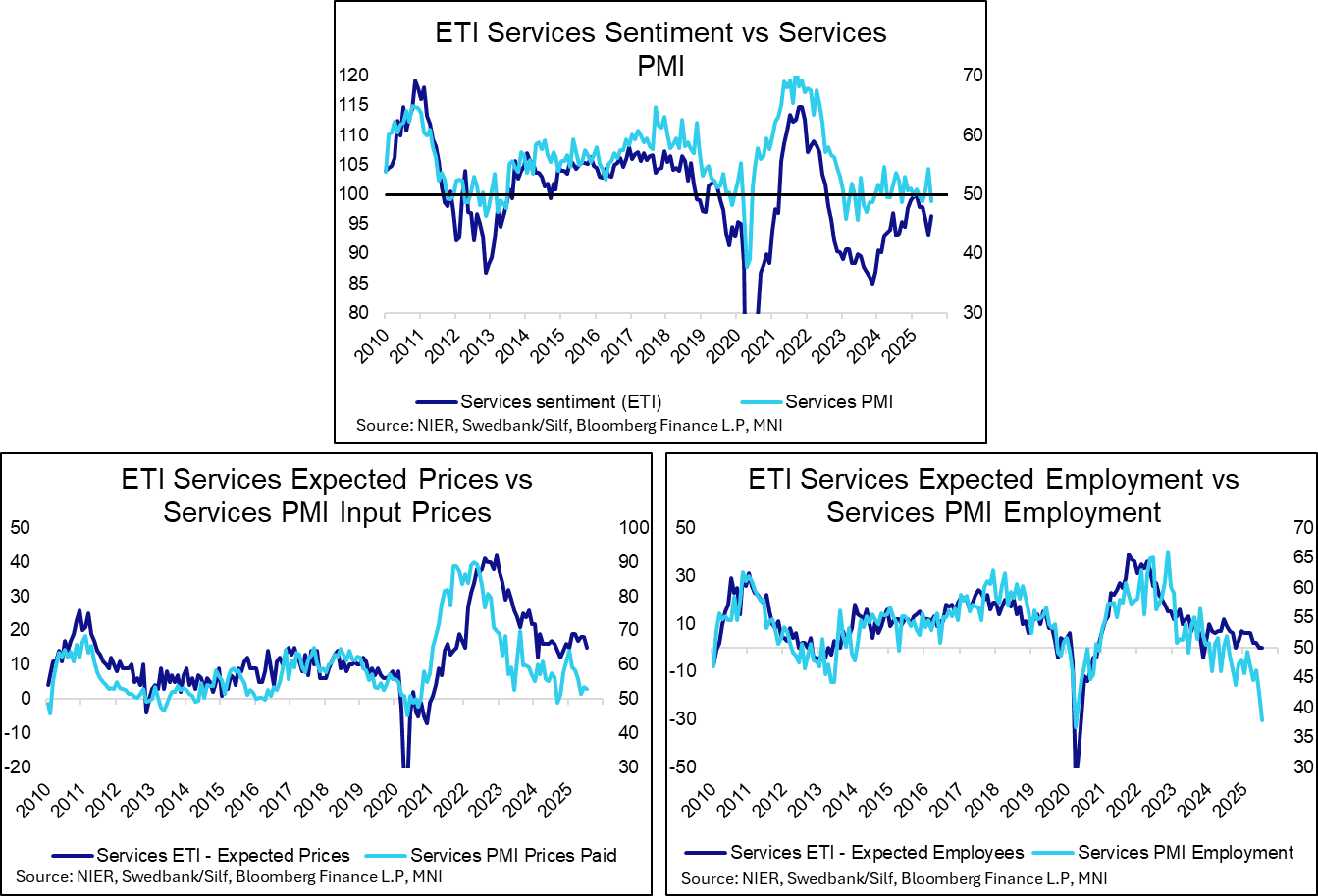

SWEDEN: Weak July Services PMI Keeps An August Rate Cut Possible

Aug-05 15:12

This morning’s services PMI was weak, falling 5.5 points to 48.8 – the largest one month drop since April 2020. While less closely followed than the Economic Tendency Indicator, the PMI has still contributed to a 1.6bp fall in 2-year SEK swap rates today.

- Thursday’s flash July CPI report will be key in determining the likelihood of a Riksbank August rate cut. Markets currently price just a 20% implied probability of such a move, but we have noted for several weeks that a cut cannot be ruled out before seeing the inflation data, particularly with activity signals still weak.

- Although new orders (51.5 vs 59.5 prior) and production (50.1 vs 57.3 prior) PMI components remained in expansionary territory in July, the falls relative to June were sharp.

- More alarmingly, the employment component fell to a 5-year low of 37.8 (vs 36.7 prior). The downward trend is more volatile than, but still broadly consistent with, the signal from the Economic Tendency Indicator’s services employment series.

PIPELINE: Corporate Bond Update: Issuance List Expands

Aug-05 15:05

- Date $MM Issuer (Priced *, Launch #)

- 08/05 $500M CNA Financial WNG 10Y +125a

- 08/05 $500M Freedom Mortgage 7.75NC3

- 08/06 $500M Travel + Leisure 8NC3

- 08/05 $Benchmark MSCI 10Y +140a

- 08/05 $Benchmark Essential Utiites 10Y +130a

- 08/05 $Benchmark Macquarie Bank 11NC10 +170a

- 08/05 $Benchmark Standard Chartered 11NC10 +145a

- 08/05 $Benchmark Tennessee Valley Authority 5Y +25a

- 08/05 $Benchmark Daimler Truck 2Y +90a, +5Y +115a, +7Y +130a

- 08/06 $Benchmark PetSmart 7NC3, 8NC3 investor calls