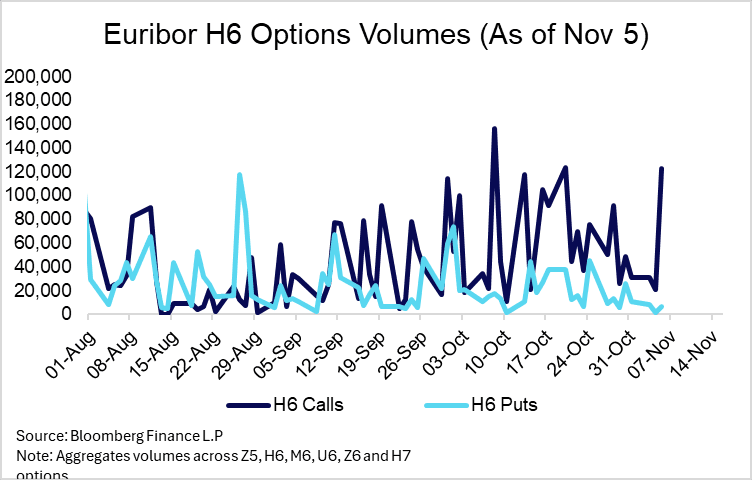

STIR: ETS2 Delay Didn't Shift OIS Pricing, But H6 Call Options Activity Noted

Yesterday’s announcement that ETS2 is likely to be delayed by one-year had little impact on ECB-dated OIS pricing. Markets retain an easing bias, with just under a 50% implied probability of one more cut this cycle. That said, there was a noticeable uptick in Euribor call options activity, particularly in calls tied to the ERH6 contract.

- The ECB had estimated that ETS2 would push up 2027 inflation by ~0.3pp in its September macroeconomic projections. If a delay is agreed in the EU Parliament and by the EC, it should imply a mechanical reduction of the 2027 inflation projection December, compensated almost one-for-one with an increase in the 2028 projection (which will be presented for the first time next month).

- Recent policymaker signalling suggests the ECB will avoid making monetary policy decisions (i.e. delivering another cut) solely on the basis of an ETS2-implied undershoot in 2027/2028.

- However, the delay will mean the ECB is set to significantly undershoot its 2% target in both 2026 and 2027. This may provide doves with an additional argument for one more cut, particularly those who still see risks to growth as skewed to the downside.

- The weaker-than-expected German September IP reading had little impact on EUR STIRs, with today’s Eurozone retail sales data also unlikely to be a mover.

- The ECB’s Money Market Conference starts today, and Executive Board member Schnabel gives a welcome address at 0800GMT. Schnabel is always worth listening to, especially on the balance sheet.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Dec-25 | 1.920 | -1.2 |

| Feb-26 | 1.905 | -2.7 |

| Mar-26 | 1.866 | -6.6 |

| Apr-26 | 1.858 | -7.4 |

| Jun-26 | 1.826 | -10.6 |

| Jul-26 | 1.826 | -10.6 |

| Sep-26 | 1.820 | -11.2 |

| Oct-26 | 1.827 | -10.5 |

| Source: MNI/Bloomberg Finance L.P. | ||

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: FX OPTION EXPIRY

Of note:

EURUSD 2.2bn at 1.1650/1.1665 (could act as magnet).

EURUSD 1.07bn at 1.1700 (wed).

EURUSD 5.76bn between 1.1600/1.1700 (fri).

- EURUSD: 1.1650 (1.83bn), 1.1665 (406mln), 1.1700 (220mln), 1.1705 (382mln), 1.1710 (282mln), 1.1750 (1.27bn).

- USDJPY: 150.00 (79mln), 150.60 (525mln), 151.00 (676mln).

- NZDUSD: 0.5810 (276mln), 0.5820 (305mln).

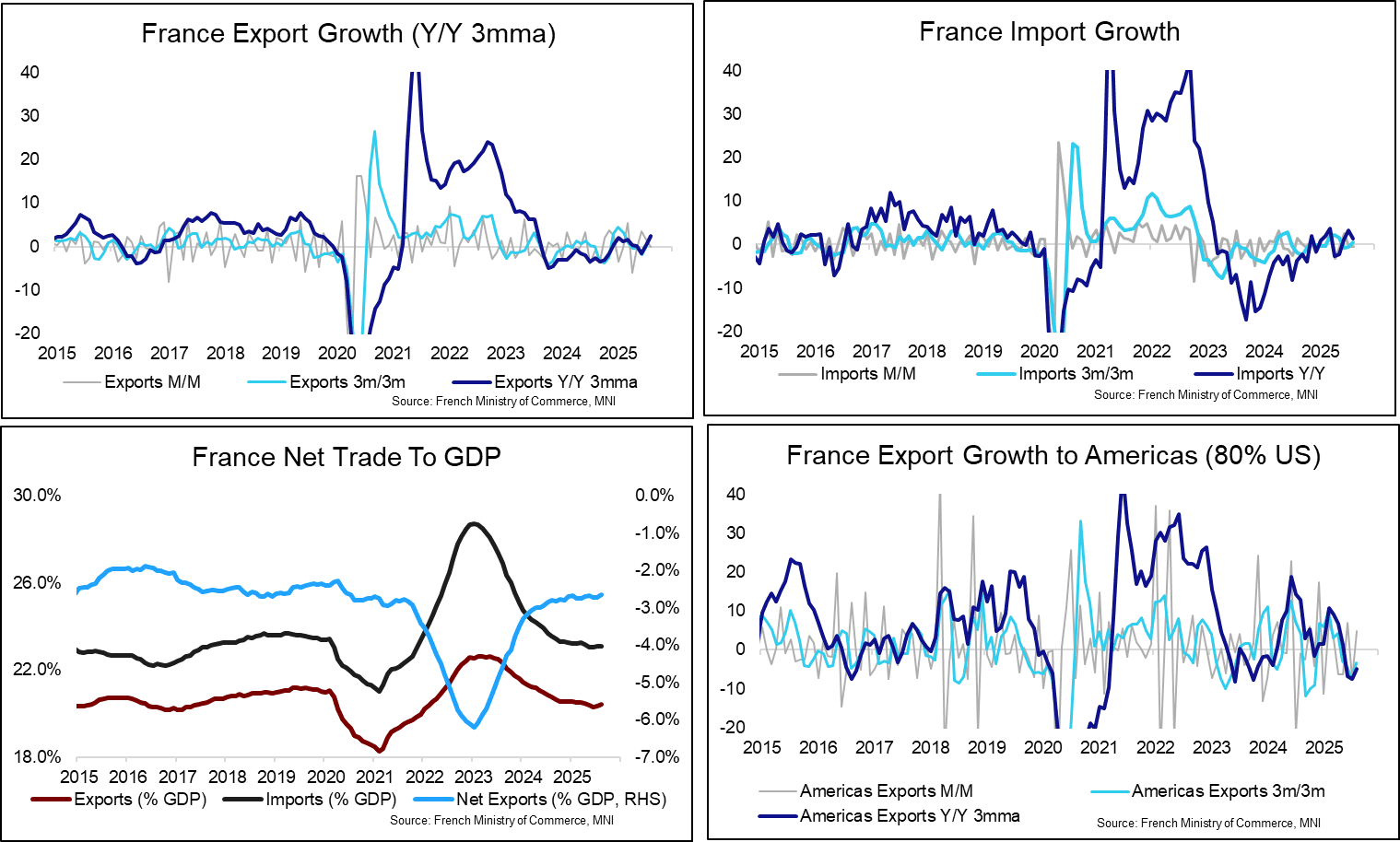

FRANCE DATA: Export Growth Recovering But Momentum Weak

The French trade deficit was E5.53bln in August, down from E5.74bln in July (revised from E5.56bln initial) and a year-to-date high of E7.42bln in February. Assuming unchanged nominal GDP growth of ~0.5% Q/Q in Q3, this implies a steady goods trade deficit of around 2.7% GDP.

- Imports fell 0.4% M/M for the second consecutive month, a sign of continued weakness in domestic demand against a backdrop of ongoing political/fiscal/economic uncertainty. However, Y/Y import growth continues to slowly recover from the 2023 lows, trending back toward pre-covid growth rates.

- Total exports fell 0.1% M/M in August, after two solid months of 3.5% and 1.7% growth in June and July. Like imports, a recovery in annual export growth from the 2023 lows is intact, though momentum is lacking. This may reflect the direct impact of US tariffs, even with trade policy uncertainty having declined since the EU-US trade agreement was struck in August. Although exports to the US rose 4.9% M/M in August, 3m/3m and Y/Y 3mma growth remains negative.

- September’s PMI round was in fitting with this theme:

- Manufacturing PMI: “Exports were also a drag on overall orders during the latest survey period, with companies mentioning US tariffs and generally sluggish market conditions as reasons for lower overseas demand.”

- Services PMI: “French service providers closed out the third quarter with another decline in new business from abroad. Albeit softer than August's year-to-date record, the contraction remained solid”.

BUNDS: Block trade

Bund Block trade, suggest buyer:

- RXZ5 3k at 128.37.

EGBs are lifted off their lows, Bobl is bought in 5k cumulative Volumes, BTP 1.7k and OAT 1k.