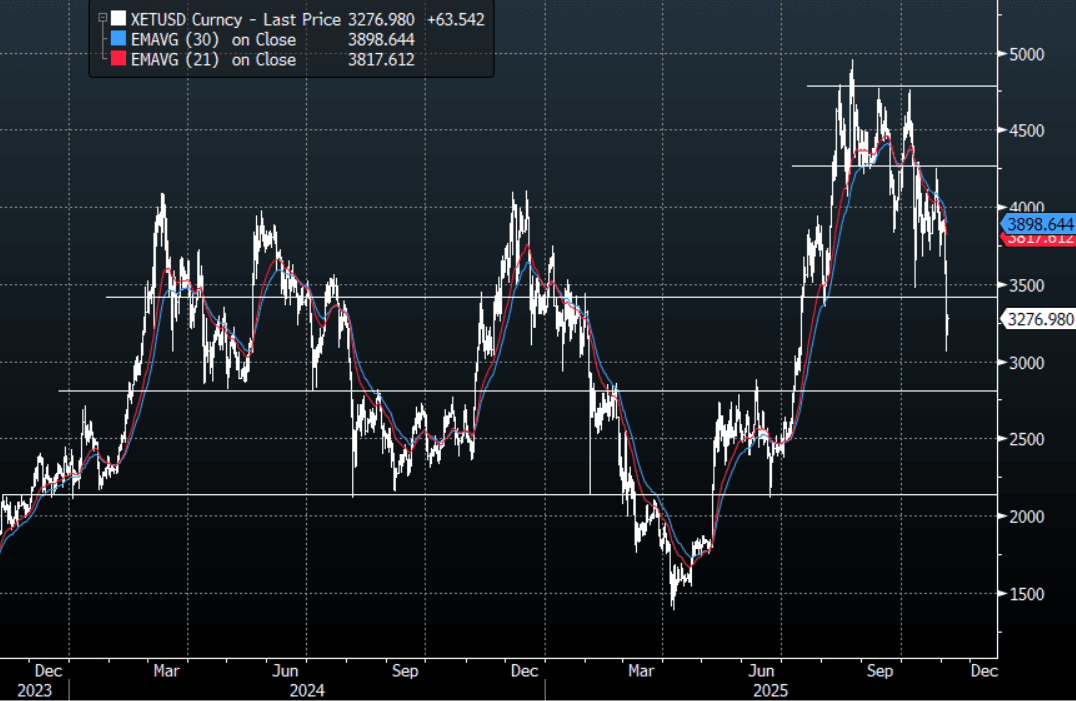

CRYPTO: Ethereum - Stops Hit Below $3400-$3500, Leads The Move Lower Down 14%

Ethereum had a range overnight of $3059.43 - $3586.03, Asia is trading around $3275, +1.85%. Ethereum like the rest of Crypto has never recovered from its crash in early October and extended its move lower overnight ending over 14% down on the day and down 22% over 2 days. Ethereum broke the support between $3300-$3500 very easily and it looks like this then triggered stops lower in very thin liquidity. As history reminds us the liquidity is always there when entering the trade but the exit door becomes very small especially in products like Crypto that trade with a very high Vol. With the USD resurgent and the risk backdrop souring dramatically I suspect rallies will continue to be used to pare back longs. The next target is back toward the $2500-$2800 area where I suspect some demand should return first up.

- Milk Road put forward his thesis of the move on X, “Markets didn’t just randomly nuke today. Three things hit at once. The Fed came out hawkish, pushing the dollar higher and sucking oxygen out of risk assets. ETFs saw heavy outflows as institutions de risked, and the Balancer exploit spooked sentiment right as liquidity was thinning. Fear, uncertainty, doubt, in that order. But underneath the chaos, nothing structural has changed. This is a shakeout, not a trend reversal.”

Fig 1: Ethereum spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSTRALIA: RBA’s Bullock Before Senate On Friday, Consumer Sentiment Tuesday

In a quiet week RBA Governor Bullock’s appearance before the Senate Economics Committee on Friday and Westpac October consumer confidence on Tuesday will be the highlights.

- RBA Governor Bullock and Assistant Governor Kent will answer questions from the Senate Economics Committee for the supplementary 2025-2026 budget at 0900 AEDT on Friday. Bullock appeared before the lower house before the 30 September decision to hold rates and so the decision as well as its inflation concerns are likely to be examined.

- Tuesday’s October Westpac consumer sentiment survey would have been taken during the week of the 30 September RBA decision and given rates were unchanged, the pre- and post-meeting breakdown will be of interest. Confidence fell 3.1% to 95.4 in September as economic and unemployment expectations deteriorated.

- ANZ September job ads also print on Tuesday. The series appears to have stabilised with it rising 1.75% y/y in August, the fastest since January 2023.

- Melbourne Institute inflation expectations for October are released on Thursday. Q3 was in line with Q2 at 4.4%. Any breaks below 4% have been short-lived. On Monday, MI’s September inflation gauge for both headline and trimmed mean rose 0.2pp, another sign of stalling disinflation.

JPY: USD/JPY 1mth RR At Fresh Highs, Option Volumes Favour Calls Above 150.00

In the options space, per DTCC (via BBG), USD/JPY is dominating early Monday volumes, at 78.6% of total traded (near$1.97bn). In terms of some of the larger volume transactions, we have seen $100mn USD/JPY calls going through at strikes ranging from 151-155. Expiries for the 155.00 strikes are in early 2026. JPY futures are elevated, last around +62.8k, against open interest of 295.8k (per BBG for JYZ5). We have been elevated for much of the morning trade period, as USD/JPY spiked higher at the open and remains supported on dips (eyeing a 150.00 test). We remain within historical norms though from an aggregate volume standpoint.

- USD/JPY implied 1 month vols are higher at 9.40% for the 1 month, but still closer to the bottom end of the 2025 range. The 1 month risk reversal is at fresh highs back to 2022, last around -0.35.

US TSYS: 2/10s Steeper, 10yr Tracking Recent Ranges As Govt Shutdown Continues

US Tsys futures are maintaining a negative bias since the open, although fresh weakness after the gap lower at the open has been modest. Spillover to the cash Tsy space is evident from the steepening bias seen in cash JGBs. The US 2/10s was last +56bps, back around Oct highs (Sep highs were +62bps). More broadly for the outright 10yr, last at 4.14%, +2bps, we remain wedged within recent 4.10-4.20% ranges. Market sentiment is somewhat mixed, with limited official data out due to the government shutdown (thereby limiting assessment on economic trends) potentially impacting sentiment. 10yr futures (TY) were last 112-17, -04+, leaving the 50-day EMA support point at 112-12+ intact.