EM CEEMEA CREDIT: ESKOM H1 results - Headlines

“*ESKOM: TO WRITE OFF 3.6B RAND OF FUNDS OWED BY MUNICIPALITIES

*ESKOM 1H PROFIT 24.3B RAND VS 17.8B RAND YEAR EARLIER” - BBG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

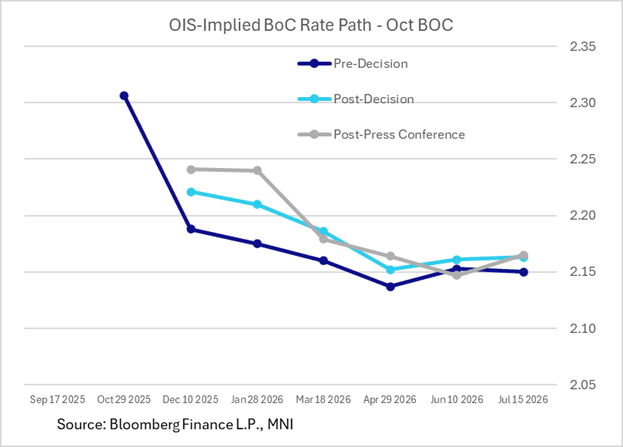

BOC: MNI BoC Review-Oct 2025: Pause Seen With Rates “About Right”

We've just published our review of the October Bank of Canada meeting - Download Full Report Here

- Along with the expected 25bp cut to an overnight rate of 2.25%, a key phrase from the BOC’s October policy statement drove a mildly hawkish market reaction by signalling an intention to hold rates steady at upcoming meetings (vs market/analyst expectations split between a further 25bp cut or a post-October pause coming into this meeting).

- The key phrase in the statement was: "If inflation and economic activity evolve broadly in line with the October projection, Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment."

- Though Governing Council didn’t close the door to another cut ("If the outlook changes, we are prepared to respond. Governing Council will be assessing incoming data carefully relative to the Bank’s forecast”), the language about rates being “about right” was repeated a few times in the post-meeting press conference, reinforcing the perception that the BOC envisages holding rates in future meetings in its base case, after having reduced policy rates by 275bp in this cycle.

- Terminal BOC overnight rate expectations concluded the press conference at around 2.15%, versus 2.12-2.13% coming into the meeting – suggesting expectations are now leaning more toward an indefinite hold rather than another cut in the cycle.

- The Canadian dollar benefited as well, with USDCAD extending losses through the press conference to move through the 1.3900 handle.

- We haven’t seen any Canada bank analyst view changes as yet. Coming into the meeting, 7 Canadian banks had been split 3/4 in favour of another cut in this cycle beyond October; BMO analysts wrote after the decision they still anticipate another 25bp reduction though we await Desjardins’ and National’s verdicts.

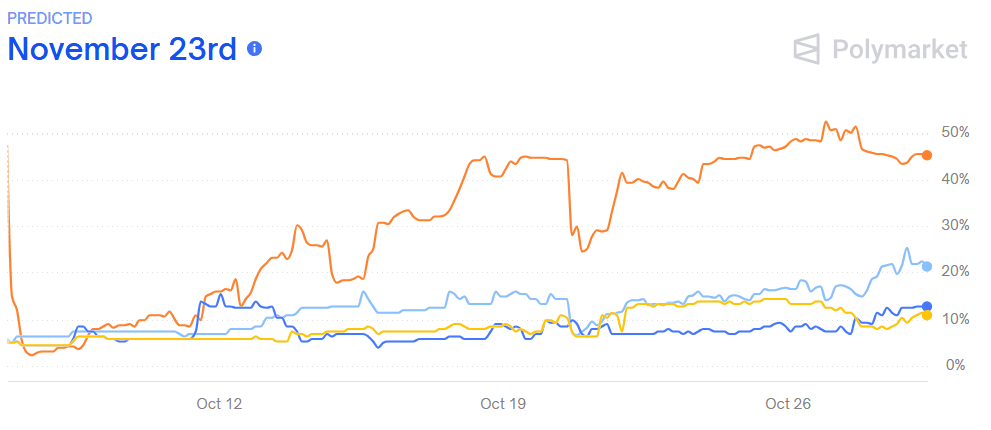

US: Speaker Johnson Won't Bring House Back To Pass New CR As Shutdown Continues

House Speaker Mike Johnson (R-LA) has ruled out bringing the House of Representatives, which has been recessed for 40 days, back into session to pass a new funding bill.

- Johnson told reporters, "Wouldn't that be a futile exercise when we have a CR that's been sitting over there since Sept. 19? If I brought the House back and we passed another CR, it would meet the exact same fate from [Senate Minority Leader] Chuck Schumer [D-NY]. He would mock it, they would spike it, and they would try to blame it on us. So, what would be the point of that?"

- Senate Majority Leader John Thune (R-SD) indicated to reporters yesterday that bipartisan talks have “picked up”, but there doesn’t appear to be an immediate offramp out of the shutdown as the two sides remain dug in on healthcare.

- Thune is likely to recess the Senate after a 14th vote on the House-passed CR on Thursday. The shutdown will enter its 35th day on Tuesday, November 4, equalling the record for the longest ever US government shutdown.

- According to Polymarket, the most likely shutdown end date is November 23. That is beyond the timeframe for the Continuing Resolution passed by the House in late September, which extends funding until November 21.

Figure 1: When will the Government Shutdown End?

- Source: Polymarket

EGBS: 10-year BTP/Bund Spread Ignoring Pullback In Euro Equities

This afternoon’s pullback in European equity futures has not spilt over into the 10-year BTP/Bund spread. A stronger-than-expected set of Italian GDP data tomorrow could set the stage for a fresh round of tightening, with the 70bp figure the next downside target.

- The spread has been steadily grinding lower since yesterday morning, now at a fresh year-to-date (and multi-year) low of 76bps.

- Note that EUR 3m10y vol has also moved to its lowest since Q4 2021, fully unwinding the modest uptick seen in the first two weeks of October. BTPs remain a popular vehicle for carry trades, which are favoured in lower vol environments.

- Note that our latest Europe Pi publication saw BTP futures remain in their habitual “very long” territory. See here for more: https://media.marketnews.com/MNI_P28102025_e9a1a7977a.pdf

- Consensus sees Italian Q3 flash GDP at 0.1% Q/Q (vs -0.1% prior). The September unemployment rate is also due tomorrow, with analysts expecting an unchanged reading of 6.0%.