EURIBOR OPTIONS: ERM6 98.12/25/37 Call Fly Lifted

ERM6 98.12/25/37 call fly paper paid 1 on 6K

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Early SOFR/Treasury Option Roundup

SOFR & Treasury option volumes very limited overnight volume, any accounts present ahead of the Christmas holiday are plying the sidelines ahead of this morning's data. Underlying futures unwound Monday's losses overnight, currently near Friday's close. Projected rate cut pricing gains slightly vs. late Monday levels (*): Jan'26 at -4.4bp, Mar'26 at -14.8bp (-14.3bp), Apr'26 at -21.9bp (-21.5bp), Jun'26 at -34.8bp (-34.1bp).

- SOFR Options:

- 4,200 SFRM6 96.62/97.00 strangles, 18.5 ref 96.695

- 4,600 SFRG6 96.50 calls, 6.0 last

- -2,000 SFRH6 96.18/96.37/96.43/96.68 put condors, 15.25 ref 96.495

- Treasury Options:

- +1,000 TYH6 112.5 calls, 49 vs. 112-14.5/0.45%

- +1,700 TYH6 113.5 calls, 27 ref 112-16.5/0.30%

- over -4,700 TYG6 110.5 puts, 3 last

- 2,100 USG6 113 puts, 19 last

GILTS: Run Of Net Long Cover Extended On Monday

OI data points to a third consecutive session of net long cover in gilt futures as the contract softened on Monday, with OI now ~16.5K or ~1.4% lower than levels seen on Tuesday of last week.

- We have previously pointed to relatively low conviction trade (as evidenced by OI data) in the post-Budget window. This adds credence to that idea.

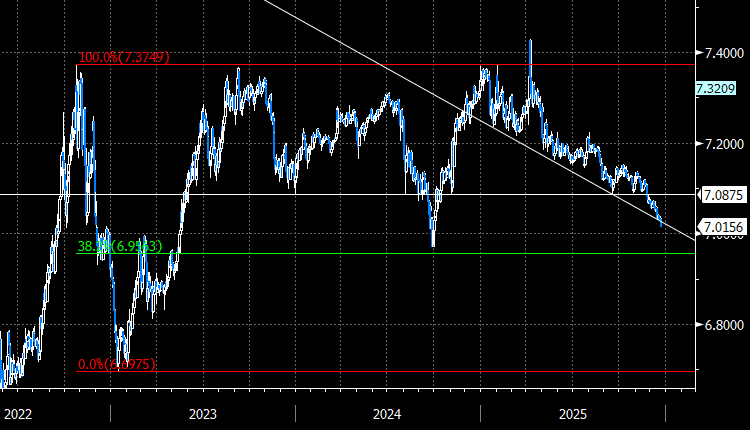

CHINA: Tools Available to Slow USDCNY Decline; But L-T Trend Still Looks Down

- USDCNH and USDCNY both today his their lowest levels since September 2024 and are raising the risk of a test of levels below 7.00 as the USD depreciates more broadly and as onshore Chinese equities look to lock-in returns of 20% for 2025.

- The rally in CNH and CNY bolsters and may embolden the Chinese authorities calls for proactive monetary policy in 2026 (as evidenced in a report in today's Shanghai Securities News arguing in favour of easier interest rates and reserve requirement ratios in Q1), but other more direct tools remain available to smooth untoward CNY strength.

- In early December, there was strong evidence of intervention through buying USD - but with a new approach. Instead of recycling the bought USD in the FX swaps market, the state-backed lenders conducting the intervention held the USD for a longer period, thereby tightening onshore USD liquidity and pressuring markets to a more acute negative carry for USD/CNY shorts.

- This method not only helps support the spot price, but it also squeezes speculation and provides a strong disincentive for exporters to accumulate CNY as a hedge to lock in profit margins. This method, if used in sufficient size, should help slow any undesired USDCNY losses through the end of the month and headed into the particularly sensitive Lunar New Year period in mid-February.

- While these tools can slow any pace of appreciation in the short-term - the recognition of the need for natural currency strength (largely to address strong external balances) is clear, hence the recent CEWC statement that argued for "stable" exchange rates, rather than calling out currency strength in particular. This makes USDCNY losses beyond 7.00 far more likely longer-term, even as the depth of the Fed easing cycle continues to be unwound.

Figure 1: USDCNH through key support; downtrend accelerates

Source: MNI / Bloomberg Finance L.P.