EUROPEAN INFLATION: Energy Drives Upward Revision To Italian June HICP

Italian final June HICP was revised up a tenth on a rounded basis to 1.8% Y/Y (vs 1.7% in May). Energy inflation was revised up three tenths to -2.1% Y/Y (vs -1.9% in May), while services was revised up a tenth to 3.0% Y/Y (vs 2.9% in May). This was mostly offset by a three tenth downward revision to processed food inflation to 2.8% Y/Y (vs 2.8% in May). Non-energy industrial goods was unrevised at 0.5% Y/Y (vs 0.4% in May), as was unprocessed foods at 4.5% Y/Y (vs 3.9% in May).

- Within services, there were accelerations in the restaurant and hotels, recreation and culture and transport services components.

- Package holidays rose 7.5% Y/Y (vs 6.3% prior), which was partially offset by a pullback in recreation and cultural services inflation (5.5% Y/Y vs 6.6% prior).

- Airfares inflation decelerated to 2.9% Y/Y (vs 4.6% prior). Although airfares rose 9% M/M on an NSA sequential basis in June, this was below last year’s reading and also some of the analyst expectations we had seen. As such, the rise in transport services was due to non-airfare (i.e. less volatile) components.

- Communication services were 0.5% Y/Y (vs 0.6% prior), while miscellaneous services were steady at 1.9% Y/Y. A pullback in insurance inflation was offset by a rise in personal care.

- Core goods inflation trends remain subdued – as is also seen in the broader Eurozone basket. In June, there was a small uptick in clothing and household appliance inflation, offset by a pullback in household textiles.

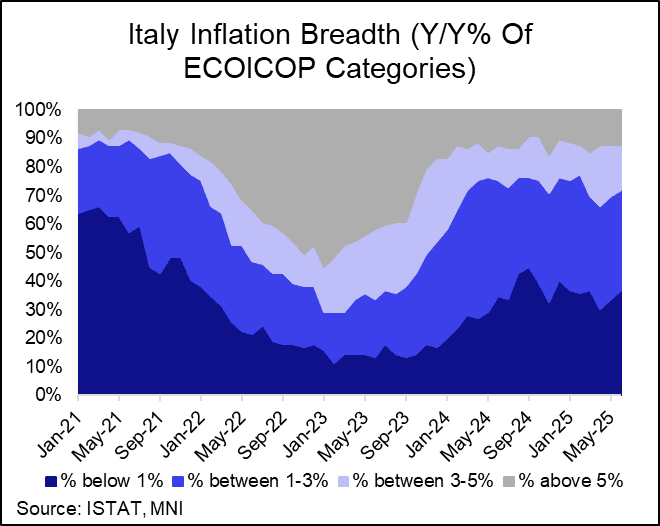

- The proportion of HICP sub-components with inflation rates between 1-3% Y/Y was steady at 35% (vs 36% prior).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: Alberta Premier Smith On Wildfires, Pipelines

MNI spoke with Alberta Premier Danielle Smith about the Canadian province's plan to build energy pipelines to the Pacific and Arctic coasts, and on the impact of recent wildfires on energy production and the economy as the central bank weighs another rate cut. On MNI Main Policy Wire now, see sales@marketnews.com for details.

PIPELINE: Corporate Bond Roundup: EIB, IBK, Hungary on TAP

- Date $MM Issuer (Priced *, Launch #)

- 06/16 $Benchmark EIB 7Y SOFR+53a

- 06/16 $Benchmark IBK 3Y SOFR+58a, 5Y +45a

- 06/16 $Benchmark Hungary +5Y, +10Y, +30Y

- 06/13 No new issuance Friday, $22.8B total on week

OUTLOOK: Price Signal Summary - Bund Support Remains Intact

- In the FI space, Bund futures have traded lower today, extending the reversal from Friday’s session high. For now, the move down is considered corrective and key short-term support to watch lies at 130.12, the Jun 5 low. A break of this level would highlight a stronger reversal and undermine the bullish theme. Key short-term resistance and the bull trigger, has been defined at 131.95, the Jun 13 high.

- A bullish condition in Gilt futures remains intact and Friday’s steep sell-off from the session high is for now, considered corrective. The move higher last week marks an extension of the recent breach of resistance at 91.87, the May 20 high. This signals scope for a test of 93.73, a 1.764 projection of the May 22 - 27 - 29 price swing. Note the uptrend is in overbought territory, a deeper pullback would unwind this position. First firm support lies at 92.04, the 20-day EMA.