TURKEY: End of KKM Scheme Solidifies Shift to Orthodoxy, But Challenges Remain

Aug-28 11:13

Policymakers formally ended the FX-protected deposit scheme (KKM) over the weekend, halting new account openings as of 23 August. Analysts estimate that the program accumulated a fiscal burden of roughly $60bln, noting that shutting KKM is symbolically significant because it represents a step towards exit from unconventional policies.

- The program has been gradually phased out over the past year, so there is unlikely to be a significant market impact. USD/TRY breached the 41.00 handle this week, and Commerzbank have argued that challenges for Turkey lie ahead.

- They say underlying inflation momentum is nowhere near target yet, and some imbalances – for example, the trade deficit – are worsening once again. Against this background, they anticipate the exchange rate to keep depreciating at a fast pace.

- Commentary from CBRT Governor Karahan sounded more optimistic earlier in the week. He said the disinflation process continues despite financial market volatility, and that the July inflation acceleration on a monthly basis was temporary.

- The CBRT said following its 300bp cut in July that the step size will be “reviewed prudently on a meeting-by-meeting basis with a focus on the inflation outlook.” A more benign outlook would support sell-side calls for continued rate cuts through year-end, with the one-week repo rate generally expected to end the year in the mid-30s.

- A columnist for Ekonomi noted that GDP and inflation data to be released next week will be decisive in determining whether this scenario remains valid. Should there be a deviation in the macroeconomic outlook, the central bank will need to respond early and adequately to maintain credibility of its targets. They said this may require slowing down rate cuts and reviewing the macroprudential framework.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

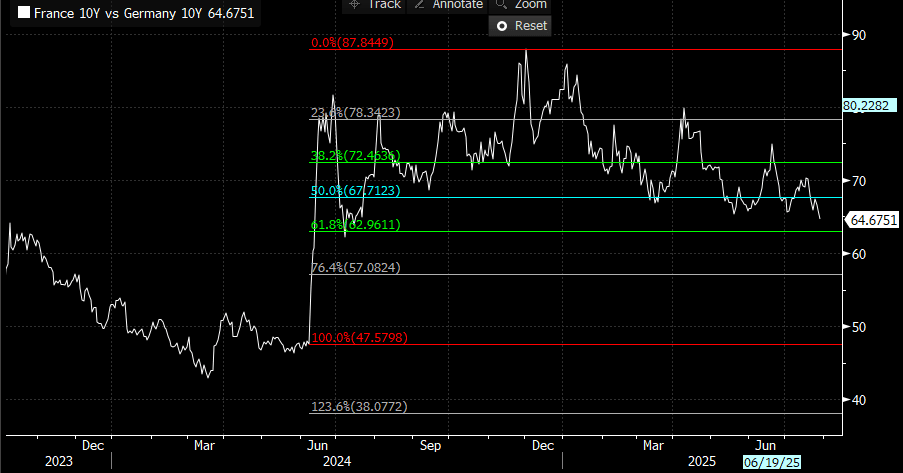

BONDS: OAT/Bund spread lowest in over a Year

Jul-29 11:05

- The OAT/Bund spread follows the BTP/Bund, and now test its tightest level in just over a Year, since the 15th July 2024.

- Next immediate support area is seen at ~63.00bps, the 61.8% retracement of Macron's sudden snap election announcement in June 2024.

(Chart source: MNI/Bloomberg).

US TSYS: Modestly Firmer Ahead Of JOLTS, Conference Board and 7Y Supply

Jul-29 10:56

- Treasuries have reversed losses in the opposite turn of events to yesterday’s US crossover.

- It leaves benchmark tenors mildly firmer across the curve ahead of a session with multiple points of interest such as JOLTS and Conference Board data before 7Y issuance. These will assessed with Refunding, the Fed, GDP, PCE and payrolls all looming ahead through Wed-Fri.

- Yesterday's Treasury borrowing estimates were almost exactly in line with MNI's estimates. We would characterize the current quarter as slightly on the high side of the median analyst expectation, with the latter quarter fairly close to expectations given what is usually a wide range for the further-out quarter. It should have little to no impact on expectations for Wednesday's Refunding announcement.

- Cash yields are 0.5-2bp lower, with 20s and 30s leading declines.

- TYU5 trades at session highs of 110-29 (+ 04+) on particularly thin cumulative volumes of just 180k.

- It has mostly remained within yesterday’s range overnight with a low of 110-24. Support is being monitored at 110-19+ (Jul 24 low) after which lies 110-08+ (Jul 14/15 lows), whilst resistance is seen at 111-14+ (Jul 22 high)

- Data: Advance trade balance Jun (0830ET), Wholesale/retail inventories Jun P/Jun (0830ET), FHFA and S&P CoreLogic May (0900ET), JOLTS Jun (1000ET), Conference Board consumer survey Jul (1000ET)

- Politics: President Trump has departed Scotland heading to The White House, set to arrive at 1920ET but with scope for updates along the way.

- Coupon issuance: US Tsy $30B 2Y FRN Note - 91282CNQ0 (1130ET), US Tsy $44B 7Y Note auction - 91282CNR8 (1300ET)

- Yesterday’s 2Y stopped through by 0.5bp before the 5Y tailed by 1bp. Peripheral stats were notably weak for the 5Y, with indirect take falling from 64.7% to 58.3% and primary dealer take jumping from 10.9% to 22.2%.

- Bill issuance: US Tsy $80B 6W bill auction (1130ET)

OUTLOOK: Price Signal Summary - Corrective Pullback In Gold

Jul-29 10:55

- On the commodity front, Gold has pulled back from its Jul 23 high. Short-term weakness is considered corrective - for now. However, the yellow metal has traded through support at $3322.9, the 50-day EMA. A clear break of this level would signal scope for a deeper retracement and expose the next key support at $3282.8, the Jul 9 low. Key short-term resistance is $3439.0, the Jul 23 high. A break of this hurdle would be bullish.

- In the oil space, a bearish theme in WTI remains intact. The sharp reversal from the Jun 23 high continues to highlight scope for an extension lower. Support to watch is the 50-day EMA, at $64.85. A clear break of it would expose $58.17, the May 30 low. On the upside, initial resistance to watch is $69.41, the 50.0% retracement of the Jun 23 - 24 high-low range.