POWER: End of Day Power Summary: FR-DE Feb Discount Narrows to Mid-December Low

The French-German January discount is at €25.72/MWh at the time of writing – the lowest since 16 December 2025 – as French power costs are being supported further by extended nuclear works and revised lower temperatures, while upward price movements of the German equivalent are tracking gains in TTF and EU ETS.

- Nordic Base Power FEB 26 up 6.5% at 66.3 EUR/MWh

- France Base Power FEB 26 up 4.4% at 73.94 EUR/MWh

- Germany Base Power FEB 26 up 2.7% at 99.66 EUR/MWh

- EUA DEC 26 up 1.1% at 88.31 EUR/MT

- TTF Gas FEB 26 up 3.1% at 29.04 EUR/MWh

- TTF front month has risen to its highest since late-November, unwinding December losses amid a cooler temperature forecast for early-January and above-normal net withdrawals from storage.

- EUAs Dec26 are rising today and are on track for weekly gains of nearly 0.5%, nearing the highest level since Aug 2023, amid bullish sentiment on tightening supply in 2026. The return of market participants from the holiday period is likely to lift buying interest.

- AquaVentus is urging Germany to speed up regulatory reforms for offshore wind, calling for hybrid electricity and hydrogen connections to cut costs.

- Swiss hydropower reserves last week – calendar week 52 – continued to fall from the previous week, albeit at a slower rate, dropping by 1.1 percentage points to 54.1% of capacity, slightly narrowing the deficit to the five-year average and flipping to small premium to last year’s level.

- Spain’s electricity demand rose by around 2.6% YoY in 2025, with coal output projected to cover just 0.6% of generation mix, down by around 50% on the year.

- Nordic hydropower reserves last week – calendar week 52 – dropped by 1.8 percentage points to end at 71.5% of capacity, declining to their lowest since week 26 of 2025. Stocks narrowed their surplus to 10-year average but widened the deficit to the same week in 2024.

- Finland’s 890MW Olkiluoto 2 nuke will be completely halted until 3 January 01:00 CET, extended from 2 January 15:00 CET.

- Severe weather linked to Storm Johannes has knocked out power to parts of Sweden, leaving about 6,100 customers without electricity as of 11:00CET, while the national grid remains stable.

- The Czech 2GW Dukovany nuclear power plant generated 14.68TWh of electricity in 2025, helping Cez’s Czech nuclear plants to reach 32TWh, supplying over 20% of the country’s power.

- Poland’s PGE has scrapped a PLN 1.3bn (€310mn) contract to modernise the 500MW Porabka-Zar pumped-storage hydropower plant, accusing contractors of delays and faulty execution.

- Poland’s climate ministry is renewing support for biogas and biomethane production, proposing auctions for facilities above 1MW, while streamlining rules for onshore wind farms.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Pullbacks Remain Shallow, Outperformance Vs. Bunds Extends

A pullback in Tsys spills over to gilts before fading in more recent trade. UK yields remain little changed to 5bp lower on the day, with the long end outperforming.

- Futures have filled Monday’s opening gap lower, with bulls remaining in technical control. Contract trades as high as 91.76.

- Initial support and resistance in the contract remain located at 90.87 & 91.93, respectively.

- Outperformance vs. Bunds develops further, with the 10-Year yield spread set to close below 170bp for the first time this year. Gilt bulls now eye the September ’24 closing low (~162bp).

- Long end outperformance vs. swaps noted and detailed earlier, with the 30-Year spread set to close above -75bp for the first time this year. Bulls now target the resistance cluster at -70b, -69.96bp and -69.71bp.

- While medium-term fiscal risks remain evident (with a particular focus on the backloaded nature of the fiscal tightening outlined in the Budget) the market has welcomed the (questionable) increase in fiscal headroom and ongoing WAM reduction in issuance, promoting swap spread widening. It seems that a fresh gilt-negative catalyst is a pre-requisite for any fresh spread narrowing at this point e.g. slower-than-envisaged UK growth, political unrest or fresh questions surrounding the UK fiscal outlook.

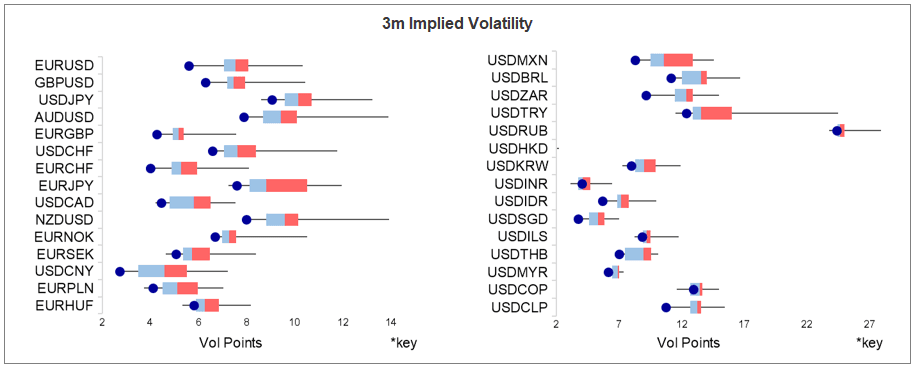

FOREX: Spiralling Vols Leave Year-End Options Cost Among Lowest of the Century

FX vol markets remain heavily pressured, particularly in the front-end of the curve and even when excluding December seasonality. Low outright vol (and vol-of-vol) coincides with solid pricing for the various rate decisions due between now and year-end (~90% for Fed & BoE cut, 80% for BoJ hike, ~100% for ECB, RBA & SNB hold), leaving minimal odds for event-driven vol.

- As a result, 3m implied vols across both G10 and EM FX heads through early December at comfortably the lowest levels of the past 12 months - as shown in this histogram:

- More notably, however, even on a 25-year look back, vols look historically extremely cheap: GBP, EUR, NZD, CAD, SEK vols are at their second lowest level for December 3rd in 25 years, NOK the third lowest and AUD the fifth lowest.

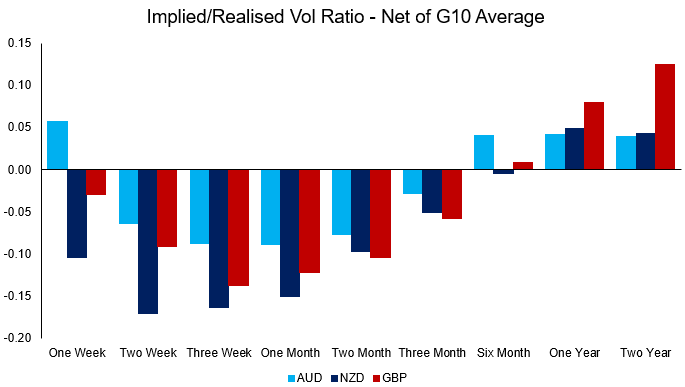

- Hotspots of vol are declining as we approach year-end (we identified JPY as one of the last currencies in focus and the implied/realised vol ratio across currencies suggests further subdued gamma demand in the likes of NZD, GBP and AUD (see bar chart below).

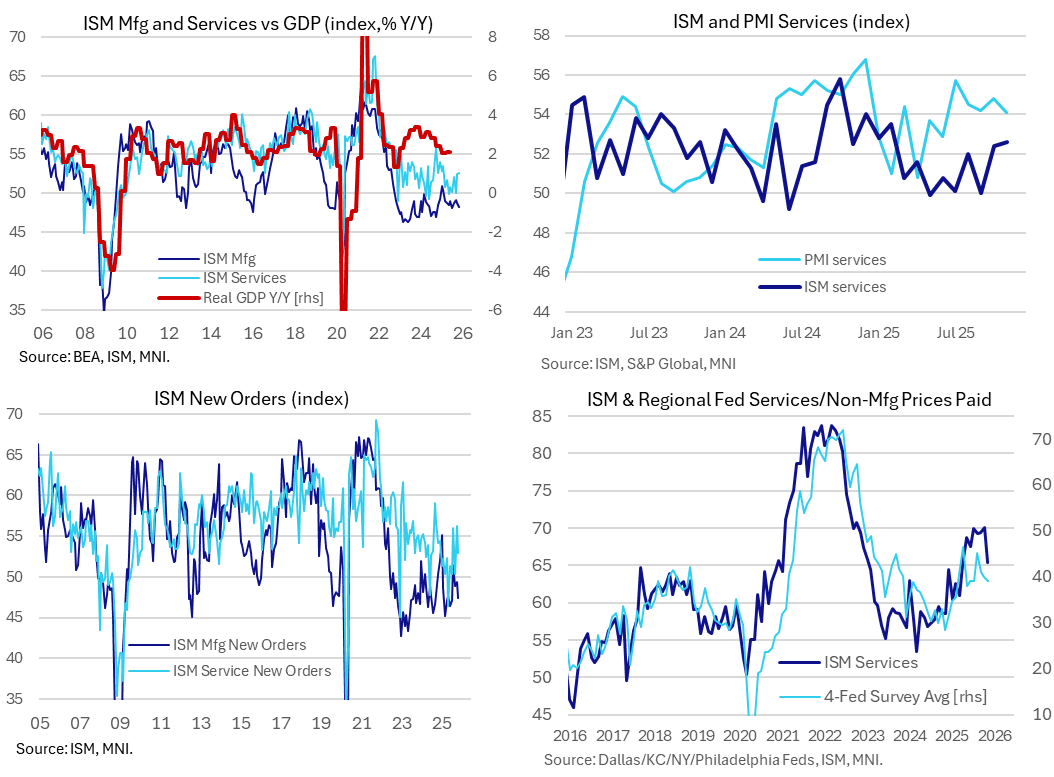

US DATA: ISM Services Beat Countered By Declines In Some Key Components

The ISM services report was stronger than expected in November although saw some conflicting developments in the main components, with new orders and prices paid slipping but employment increasing to a six-month high (albeit still in contractionary territory).

- The ISM services index was stronger than expected in November as it inched higher to 52.6 (cons 52.0) after 52.4 in October, marking its highest since February.

- The S&P Global US services PMI continues to offer a more optimistic assessment of current activity despite being revised down in its final November release to 54.1. That said, the 1.5pt outperformance is the smallest gap since the ISM survey briefly overshot it in April.

- Twelve industries reported growth last month, led by retail trade, entertainment and recreation, and accommodation and food services. Five contracted, including construction.

- New orders fell 3.3pts to 52.9 after a twelve-month high of 56.2 in October, but it’s hard to take a signal from here after some particularly volatile months where it’s swung between 50 to 56 handles in each month since July.

- Orders are a clear area when the PMI report is more optimistic, noting "Activity was supported by the firmest rise in new work of 2025 so far, whilst confidence in the outlook strengthened following the end of the government shutdown and expectations of improved economic growth in the year ahead."

- Prices paid saw a more notable 4.6pt decline to 65.4 after the 70.0 in October poked above 69.9 in July for the highest since Oct 2022. It’s the lowest since April but is still elevated historically, for instance following 58.7 in 2024 and 57.5 in 2019 for longer-term context).

- As noted beforehand, regional Fed service surveys pointed to downside risk for prices paid, as has been the case through 2H25, but the services PMI saw a sharp uptick in input cost inflation, even after a downward revision in the final S&P Global release just before the ISM release.

- The employment index meanwhile logged a fourth consecutive monthly increase to 48.9 (+0.7pts), still in contractionary territory but a six-month high.