EUROZONE ISSUANCE: EGB Supply Daily

Finland is likely to hold a 10-year Sep-36 RFGB syndication today while Spain will also hold an auct...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Yields Brush Off Oil Decline with Further Rise; 10-Yr Above 4.10%

US yields ignored positivity elsewhere and rose again during the Asian trading day. Yields were higher by 1-2.5bps with the short end underperforming as the curve flattened by -2.6bps to 55.4bps. The 10-Yr has consolidated above 4.10% and should the inflation led volatility continue, could test 4.20%

- The 2-Yr is up +2.3bps at 3.565%

- The 5-Yr is up +2.1bps at 3.708%

- The 10-Yr is up +1.5bps at 4.115%

- The 30-Yr is up +1.1bps at 4.727%

Futures are however higher on relatively light volumes Tuesday with the 10-Yr up +05 to 112-17+. TYH6 is wedged between the converged 50-day / 200-day EMA at 112-15+ as lower resistance and the upper resistance via the 20-day EMA at 112-22+. A convergence of the 50-day and 200-day Exponential Moving Averages (EMAs) suggests a period of indecision and a lack of definitive market momentum.

Key out this week is CPI for February. Forecasts expect the annual inflation rate to hold steady at 2.4%, matching the January reading. This February report covers the period before recent energy price spikes caused by geopolitical conflicts meaning it may appear tamer than current real-time costs suggest.

Other data out include Existing Home Sales, ADP employment whilst Dallas Fed President Lorie Logan is scheduled to speak at 1:00 PM.

There is a US$90bn 6-week auction and US$58bn 3-Yr scheduled. Auctions Monday saw bid to covers' lower than prior

ASIA STOCKS: Asian Stocks Higher as Oil Slides / Geopolitical Tensions Ease

- Asian equity markets staged a sharp broad-based rebound today recovering from a massive sell-off in the previous session.

- The historic plunge in oil prices, which fell over 10% toward $90 per barrel after Trump suggested the Middle East conflict could "end soon".

- Nikkei 225 jumped 2.07% to close near 53,821, clawing back roughly half of Monday's 6% plunge. It had reached 54,694 earlier before profit takers took over sending the index back to more moderate gains. Key AI tech stocks are strong today with Keyance Corp up +3.5% and Advantest up +4.5% whilst Softbank lagged with only modest gains of +.40%.

- The KOSPI surged over 6% initially, settling back to gains of 4.8%, triggering a trading curb after futures rose more than 5%. SK Hynix is flying Tuesday up +10.4% and Samsung up +8.5% whilst key energy stocks like Daesung Energy fell -12.5%

- The Hang Seng is up +1.5% as onshore bourses are up around 1% supported by tech and travel gains. Sentiment was bolstered by China’s exports surged 21.8% in the January-February period, far exceeding forecasts.

- SE Asia's bourses have bounced also with the JCI, FTSE Malay and SE Thai up +.70, +1.4% and +1.17% respectively. For each the additionally catalyst was a stronger day for the respective currencies having been suffering under USD strength in recent days.

- Markets will remain pinned to headlines regarding the U.S.-Israel-Iran conflict. Sentiment currently hinges on whether Trump’s signal of a "very soon" resolution holds true.

JGBS: Bull-Flattener, Market Prices Little Chance Of BOJ Hike Until June

JGB futures are slightly stronger, +4 compared to settlement levels.

- (Bloomberg) "War in the Middle East stands to hit Japan’s economy hard, given its reliance on crude oil imports from the region. A key question is whether the Bank of Japan delays its process of gradual stimulus reduction to cushion demand or moves swiftly with a rate increase to protect consumer-price stability. We expect the latter, and have brought forward our rate-hike call to April from July.”

- “Policymakers are mindful of Japan's painful experience during the oil shocks in the 1970s - and the lesson that the right response is to tighten policy. What's more, there are few signs that the BOJ's hikes to date have slowed growth.”

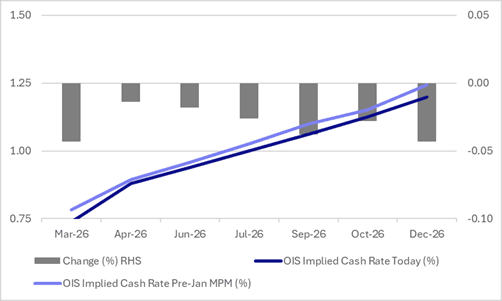

- However, BOJ-dated OIS remains slightly 1-4bps softer across meetings than pre-January MPM levels.

- Current pricing assigns a 5% probability of a 25bp hike in March, rising to 85% by June, 159% by October, signalling expectations for more than one hike by late 2026.

- Cash US tsys are 2-3bps cheaper in today's Asia-Pac session.

- Cash JGBs are flat to 4bps richer across benchmarks, with a flattening bias.

- Swaps curve has twist-flattened, with rates +3bps to -1bp.

- Tomorrow, the local calendar will see PPI data alongside 5-year supply.

Source: Bloomberg Finance LP / MNI