CZECHIA: Economic Growth Tops Bloomberg Consensus, Money Supply Data Eyed

- The Czech economy expanded by 2.6% Y/Y in Q2, according to preliminary data released by the CZSO this morning, exceeding Bloomberg median estimate of +2.4%. In sequential terms, GDP rose by 0.5% Q/Q versus +0.2% expected. The CNB is expected to comment on GDP figures at 12:00BST/13:00CEST. The central bank's Summer Forecast projected a +2.7% Y/Y GDP growth rate for 2Q25.

- The CNB will release July money supply data at the top of the hour (09:00BST/10:00CEST). CNB Governor Aleš Michl repeatedly drew attention to money growth and told Central Banking that he likes to monitor 'trends in various defined aggregates of M, particularly the three-month average of M2'.

- President Petr Pavel and Prime Minister Petr Fiala reaffirmed their unity on key foreign policy issues, including Ukraine and the Middle East. In a recent interview, Pavel indicated that his stance on the situation in Gaza deviates from the Prime Minister's 'unconditional support' for Israel.

- Seznam Zprávy reached out to over 50 ANO MPs, asking them if they would prefer their party to govern in a coalition with one of the members of the post-2021 ruling coalition (Spolu, STAN, Pirates) or with one of the anti-establishment parties (SPD, Stačilo!, Motoristy). Around 30 did not reply and most of the others gave ambiguous answers.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Euribor Futures Off Session Lows, Upside Risks To Q2 GDP Print

Euribor futures have moved away from session lows since the European cash open, currently flat to -1.5 ticks through the blues. Trendline support in ERH6, drawn from the May 2024 low, remains intact. National data released so far suggests there may be upside risks to analysts’ 0.0% Q/Q Eurozone-wide GDP projection (released 1000BST today). However, we would argue that markets have already incorporated a slightly better-than-expected growth picture following last week’s ECB decision/press conference. A reminder that the ECB projected a 0.2% Q/Q reading in its June macroeconomic projections.

- French Q2 flash GDP was 0.3% Q/Q, above the 0.1% consensus. Although skewed higher by inventories, the French data follows a stronger-than-expected reading in Spain yesterday (0.7% Q/Q vs 0.6% cons) and only a modest 1.0% Q/Q fall in Ireland. Some analysts had pencilled in a more severe reversal of Q1 Irish tariff frontloading.

- Meanwhile, the Eurozone July flash inflation round kicked off with a slightly higher-than-expected reading in Spain (2.7% Y/Y vs 2.6% prior). Other major countries’ prints are due tomorrow. MNI preview here .

- Markets still lean in favour of one more 25bp cut this cycle, with OIS pricing 20bps of easing through March 2026. Some more dovish rhetoric from the likes of Rehn and Villeroy last week, alongside the MNI Policy Team’s latest sources piece, have limited further hawkish repricing in EUR STIRs for now.

- Other regional data shouldn’t be as market moving as GDP (ECB wage tracker, EC July survey). Broader macro focus remains on today’s US refunding announcement and the BOC/Fed decisions.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Sep-25 | 1.891 | -3.2 |

| Oct-25 | 1.856 | -6.7 |

| Dec-25 | 1.772 | -15.1 |

| Feb-26 | 1.754 | -16.9 |

| Mar-26 | 1.724 | -19.9 |

| Apr-26 | 1.727 | -19.6 |

| Jun-26 | 1.733 | -19.1 |

| Jul-26 | 1.736 | -18.7 |

| Source: MNI/Bloomberg Finance L.P. | ||

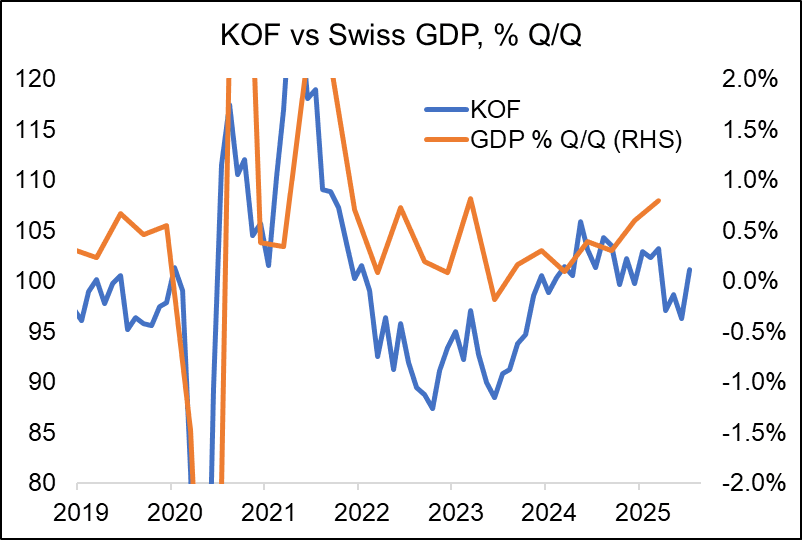

SWITZERLAND DATA: KOF Recovers In July As US-Swiss Deal Remains In Pipeline

The Swiss KOF Economic Barometer recovered in July to 101.1, above consensus of 97.9 and following June's 96.3 (revised from 96.1). The improved sentiment comes amid a US-Swiss trade deal remaining in the pipeline for now.

- “Among the indicator bundles included in the Economic Barometer, the indicators for manufacturing, for hospitality as well as for other services particularly reflect the positive developments. The indicators for foreign demand and for financial and insurance services, however, are under downward pressure”, the KOF institute comments.

- The 15% US-EU trade deal appears to be seen negatively in Switzerland on balance, with fears that the country also will end up with less favourable export conditions going forward. A trade agreement with the US seen as detrimental for Switzerland would have the potential to weigh on sentiment in the country going forward.

- From a monetary policy perspective, today's print will be of limited significance as the SNB's main focus is on inflation amid the continued CPI Y/Y readings around 0% in the country.

AUDNZD: Westpac Maintain Long Bias

Westpac remain “biased towards buying AUD/NZD on dips.”

- They’d look to enter longs around 1.0860, targeting 1.1050, with a trailing stop at 1.0810.

- Westpac note that “Australian Q2 CPI was softer than expected, locking in an RBA rate cut for 12 August. Further afield, developments in China have been encouraging. Iron ore has risen 10% during the past month, amid infrastructure announcements such the large hydro dam in Tibet. And the Shanghai Composite is up 9%. Regarding U.S.-China negotiations for an extended tariff truce, the mood is reportedly constructive, awaiting President Trump’s decision”.