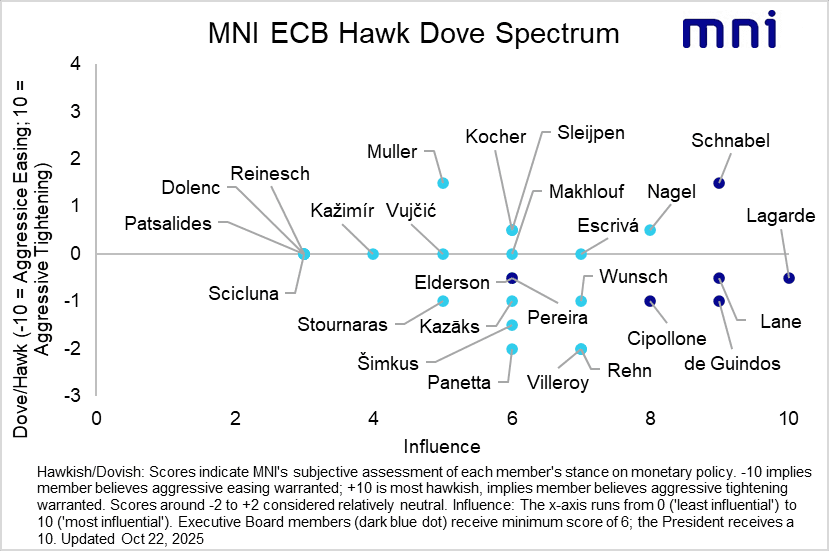

ECB: ECB Speak Wrap (Oct 31 – Nov 19) - A Few Tweaks To Hawk/Dove Matrix

The implied probability of another ECB cut this cycle has pulled back since the ECB’s October decision. OIS markets now price just 9bps of easing through September 2026 (vs ~12bps before the October decision). A combination of resilient growth signals and fairly cautious ECBspeak have factored into recent repricing, even with some Governing Council members still cognizant of downside inflation risks in the medium term.

The introduction of the EU’s ETS2 carbon pricing scheme is likely to be delayed by a year to 2028. This is expected to mechanically pull down the ECB’s 2027 inflation projection by ~0.3pp, deepening the expected undershoot of the 2% target, but policymakers have warned against relying too much on these dynamics for calibrating near-term policy.

Taking into account commentary since the October decision, we’ve made a few tweaks to our ECB hawk/dove matrix. See the full report for more

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Repo Reference Rates: Retreat

- Secured Overnight Financing Rate (SOFR): 4.18% (-0.12), volume: $3.022T

- Broad General Collateral Rate (BGCR): 4.16% (-0.09), volume: $1.180T

- Tri-Party General Collateral Rate (TCR): 4.16% (-0.09), volume: $1.145T

- (rate, volume levels reflect prior session)

SWEDEN: Mandates 2028 USD Bond Via Syndication

"*MANDATE: KINGDOM OF SWEDEN $BENCHMARK 1/2028 BOND OFFERING" Bloomberg

"*NEW DEAL: SWEDEN $BENCHMARK JAN. 2028 BOND SOFR MS+30 AREA" Bloomberg

- This is the second foreign currency syndication of the year. In June, Sweden sold E2bln (~SEK21.8bln) of the 2.00% Jun-28 Sweden EUR bond.

- Riksgalden's May borrowing report noted that "the Debt Office will issue two foreign currency bonds in 2025 instead of one. The two loans together correspond to around SEK 39 billion. In keeping with the plan from November, we are also planning a loan in 2026 corresponding to approximately SEK 19 billion".

- With the EUR sale earlier this year raising almost SEK22bln, a transaction size totalling USD1.75-2.00bln (i.e.around SEK16.5 - SEK19bln) seems reasonable.

- A reminder that Riksgalden's November borrowing report, which will have to account for the Government’s expansionary 2026 budget plans, will be released in late November.

FOREX: USD Index Hits New Daily High Into NY Crossover

The USD Index heads into the NY crossover at the highest levels of the day, topping Friday's high in the process. This puts EUR/USD briefly back below 1.1650 and has GBPUSD testing the 1.34 handle, adding to the evidence that the USD found a base on the back of Trump's optimism around a China deal, particularly as he called additional tariffs on Chinese imports as "not sustainable".

- With no tier one data due this week until Friday's rescheduled CPI print, and the Fed inside the media blackout period, market focus remains on geopolitics and leaders' meetings in the coming weeks (particularly Trump-Xi next week) and any prepwork that may take place this week.

- Vol markets are under pressure - particularly at the front-end of the curve. EURUSD one-week implied is pressured well toward YTD lows and saw very little benefit from capturing Friday's inflation print. This may signal markets seeing CPI as pretty inconsequential, particularly as the government shutdown drags on and the Fed's cutting cycle is well priced for 2 consecutive 25bps rate cuts.