US BASIC INDUSTRIES: Eastman Chemical: 4Q25 Results

Modest Credit Negative - 2026 cost initiatives imply HSD% EBITDA growth and leverage of ~3.0x. The c...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

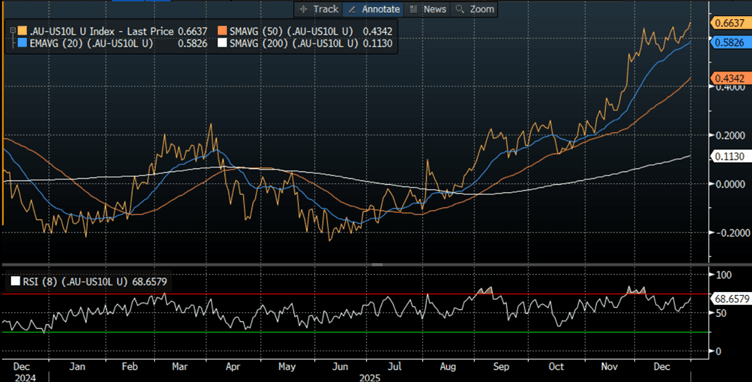

AUSSIE BONDS: Modestly Cheaper, AU-US 10Y Diff At Fresh High

ACGBs (YM -3.0 & XM -3.0) are modestly cheaper in today’s pre-holiday shortened session.

- Cash US tsys showed little reaction to the FOMC minutes release for the December meeting yesterday. The key paragraph from the December FOMC meeting minutes (link here) indicates (as did the meeting Dot Plot) a sizeable minority of members seeing no further easing through end-2026, but a base case among a solid if narrow majority that further limited cuts would ensue if the data cooperate.

- Cash ACGBs are 3bps cheaper with the AU-US 10-year yield differential at +65bps, a fresh cycle high.

- The bills strip is cheaper, with pricing -2 to -4 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 40% for February to 108% by June and 163% by December 2026.

- By the end of January, Australians should have a clearer picture of whether they can expect interest rate hikes in 2026. Quarterly inflation data, due to be released on January 28, will confirm or allay RBA fears that upward price pressures are entrenched in the economy.

Bloomberg Finance LP

US TSYS: Slightly Weaker Ahead Of NY Holiday

TYH6 is dealing at 112-20+, -0-02+ from closing levels in today's Asia-Pac session

- Yesterday, US tsys closed modestly mixed after the bell, curves twist steeper with the short end outperforming: 2s10s +2.168 at 67.531, 5s30s +0.409 at 113.113.

- Inside session ranges on lighter volumes (TYH6 just over 900k, despite some chunky block sales in 5s and 10

- s) as those present digest the Dec FOMC minutes release with varying opinions on labour, inflation outlooks and risk metrics.

- TYH6 trades 112-20.5 (-2.5) vs. 112-17 low / 112-25.5 high, 10Y yld at 4.1258% (+.0156). Trend theme remains bearish and a break of 111-29 would confirm a resumption of the bear cycle. This would open 111-19, a Fibonacci projection.

- Key short-term resistance has been defined at 112-31, the Dec 18 high, where a break would undermine a bear theme and signal scope for a stronger recovery instead.

- Markets will close early (1300ET; 1600ET Globex) Wednesday for New Years eve, re-open/electronic trade Thursday evening for Friday's order of business. Tomorrow's shortened session sees Weekly Jobless Claims (0830ET). Followed by US Treasury supply: 4W, 8W & 17W bills at 1130ET.

FOREX: G10 Weaker As US$ Strengthens, A$ Outperforms On Higher Metals

The US dollar strengthened through the European/US sessions with the BBDXY index finishing up 0.1% to 1203.13. The G10 was broadly softer against the greenback except for Aussie which was unchanged supported by stronger metal prices. The December FOMC minutes showed that most members expect to cut rates further “if inflation declined over time as expected” after the meeting’s decision to ease 25bp. However, Chair Powell remained cautious and a number of members thought it “would likely be appropriate to keep the target range unchanged for some time after a lowering of the range”.

- AUDUSD reached 0.6718 in late APAC trading and then trended lower to 0.6688 before returning to around 0.6700. It is currently around 0.6695 to be little changed.

- The yen underperformed along with the pound and Swiss franc. USDJPY rose 0.2% to 156.42 after a high of 155.75 and has started today around 156.38. It has been in a range around 155.50/156.50 since it peaked at 157.78 on 19 December. AUDJPY finished up 0.3% to 104.73 after falling below 104.50 briefly.

- With kiwi’s underperformance, AUDNZD continued its uptrend reaching a high of 1.1564. It finished up 0.2% to 1.1560 and is 1.2% higher in December. It is now at 1.1558. The pair is up 7.2% since the end of June as central bank policy stances diverged.

- NZDUSD fell 0.2% to 0.5792 just off the intraday low at 0.5789.

- Equities were mixed with the Euro stoxx up 0.8% but S&P down 0.1%. Silver rose 5.8% and copper 3.2% with iron ore stable around $106/t. Oil was slightly softer.

- Today is another quiet day with no data or events in Australia, NZ or Japan ahead of the January 1 holidays.