US DATA: Earnings The Only ‘Strong’ Side Of Payrolls Report

Aug-01 16:32

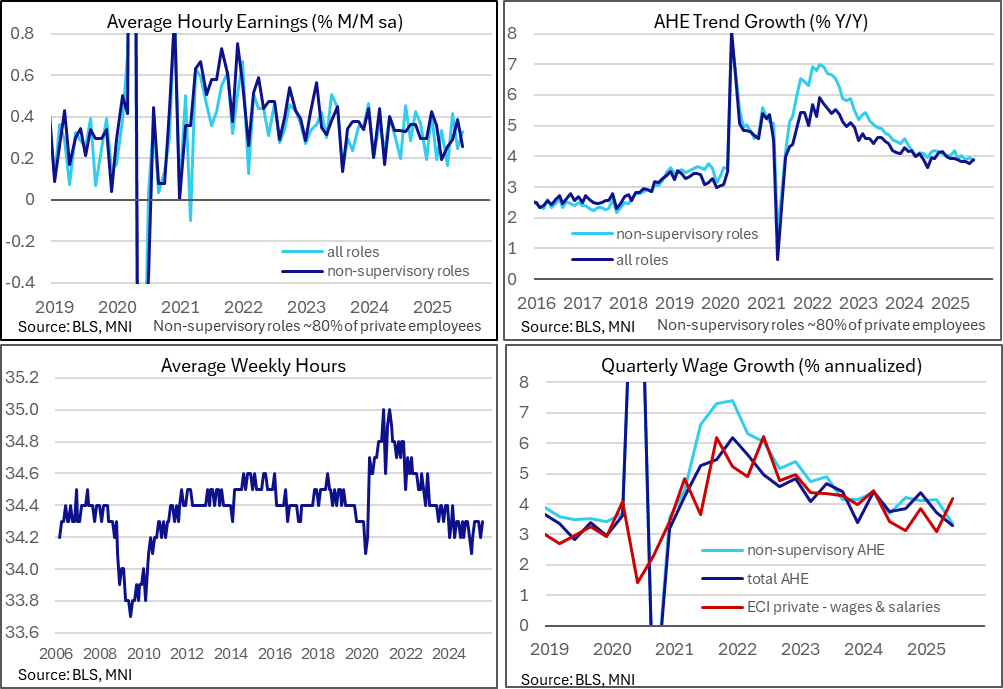

The earnings side of the nonfarm payrolls report was the only area that surprised positively in July. It adds to Thursday’s stronger than expected ECI for Q2 although the recent souring in payrolls growth will likely be expected to dampen wage growth ahead if its maintained.

- The earnings side of the July report was the only area to moderately surprise in a hawkish direction, and it was clearly dominated by softer cues from payrolls growth.

- Nevertheless, average hourly earnings growth accelerated to 0.33% M/M (cons 0.3) after an upward revised 0.25% (initial 0.22) in June and 0.42% (initial 0.39%) in May.

- That left AHE growth at 3.91% Y/Y (cons 3.8) for its highest since February.

- Within this, the non-supervisory category saw 0.26% M/M after a solidly upward revised 0.385% (initial 0.29%) in June that more than offset the downward revised 0.29% (initial 0.32%) in May.

- That left the non-supervisory Y/Y at a similar 3.89% although that’s its softest since early 2021.

- This mild upside surprise came despite the mechanical drag that should have been seen from average weekly hours increasing back a tenth to 34.3 (cons 34.2) to avoid a rare second month at a low 34.2.

- This relatively stronger wage angle follows yesterday’s stronger than expected Employment Cost Index for Q2, which at 0.94% Q/Q was a reasonable beat of 0.8% consensus considering it’s a non-annualized rate. The 3.8% annualized is the fastest quarterly rate since 1Q24, led by the private sector wages & salaries component rising 4.2%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Midday Update: Extending Lows

Jul-02 16:13

- Treasuries are extending midday lows currently, no obvious headline driver, more flow driven amid robust volumes (TYU5 over 1.2M).

- The Sep'25 10Y contract trades -10 at 111-17.5, session and 1W lows at the moment. First key support to watch is 111.07.5, the 20-day EMA.

- Curves remain steeper but off highs: 2s10s +4.251 at 50.964 (52.814H), 5s30s +3.403 at 96.167 (98.661H).

- Cross asset: Bbg US$ index off midmorning high: 1190.19 (+0.68), stocks mildly firmer (SPX eminis +15.00 at 6263.75, crude firmer (WTI +1.0 at 66.45), Gold firmer at 3345.58.

FOREX: GBP Under Significant Pressure as Political Uncertainty Ramps Up

Jul-02 16:12

- Political uncertainty in the UK heavily weighed on sterling Wednesday, as markets speculated that Rachel Reeves’ term as Chancellor of the Exchequer might be coming to an end. Prime Minister Sir Keir Starmer refused to publicly back his Chancellor, in a testing session of PMQs in the House of Commons, heightening the market’s fiscal concerns.

- GBPUSD remains roughly 1% lower on the session as we approach the APAC crossover, having traded as low as 1.3563 amid the tumult, during which the 30-yr gilt yield rose as much as 22bps at its extreme. 20-day EMA support was pierced below 1.3586 and a sustained break of this average would signal scope for a more pronounced corrective pullback. The 50-day, which has supported dips well in recent months, intersects at 1.3439.

- For EURGBP, this week’s gains are reinforcing current bullish conditions. 0.8592, 61.8% of the Apr 11 - May 29 downleg, has been broken, as well as 0.8624, the Apr 21 high. Above here, the next significant targets are 0.8694 and 0.8738, the Apr 14 & 11 highs respectively. GBPJPY is also extending towards an important area, located around 195.00.

- Elsewhere, the dollar index trades on a slightly firmer footing, up around 0.25% on the session as markets await the significant US employment report on Thursday. Two key factors have helped stabilise the greenback: the reversal higher for US yields from dovish extremes and an important technical support holding for the DXY, a trendline drawn across the 2011 and 2021 lows.

- Aside from the GBP weakness, NZD moderately underperforms its G10 peers, down 0.40% and consolidating back below 0.6100. Despite the moderate losses for both Aussie and Kiwi today, the medium-term bullish trends for both AUDUSD and NZDUSD have been bolstered this week ahead of RBA and RNBZ central bank decisions next week. For AUD, sights remain on key resistance at 0.6688, the US election related highs.

- US employment report and ISM services headline a packed US calendar on Thursday.

LOOK AHEAD: Thursday Data Calendar: Jam-Packed

Jul-02 16:00

Busy day tomorrow: Aside from weekly claims, Thursday's session includes the June employment report due to Friday's 4th of July holiday closure.

- US Data/Speaker Calendar (prior, estimate)

- 07/03 0830 Trade Balance (-$61.6B, -$71.0B)

- 07/03 0830 Initial Jobless Claims (236k, 241k), Continuing Claims (1.974M, 1.962M)

- 07/03 0830 Change in Nonfarm Payrolls (139k, 110k), Private Payrolls (140k, 102k)

- 07/03 0830 Unemployment Rate (4.2%, 4.3%), Participation Rate (62.4%, 62.5%)

- 07/03 0945 S&P Global US Services PMI (53.1, 53.1), Comp (52.8, --)

- 07/03 1000 ISM Services Index (49.9, 50.7), Prices Paid (68.7, 68.6)

- 07/03 1000 ISM Services New Orders (46.4, --), Employ (50.7, --)

- 07/03 1000 Factory Orders (-0.5%, 0.2%), Ex-Trans (-0.5%, 0.2%)

- 07/03 1000 Durable Goods Orders (16.4%, 16.4%), Ex-Trans (0.5%, 0.5%)

- 07/03 1000 Cap Goods Orders Nondef Ex Air (1.7%, 1.7%), Ship (0.5%, 0.5%)

- 07/03 1130 Atl Fed Bostic on monetary policy, Frankfurt (text, Q&A)

- 07/03 1000 US Tsy $55B 4W & $45B 8W bill auctions

- Source: Bloomberg Finance L.P. / MNI