US STOCKS: Early Equities Roundup: Hawkish Data Weighing on Stocks

Sep-25 15:22

- Stocks are drifting in mildly weaker territory - off this morning's post-data lows as participants continue to digest a flood of economic data. Stocks retreated after this morning's data triggered hawkish reactions in Treasuries and projected rate cuts into year end.

- Currently, the DJIA trades down 77.59 points (-0.17%) at 46042.51, S&P E-Minis down 29 points (-0.43%) at 6663.75, the Nasdaq down 99.7 points (-0.4%) at 22401.77.

- Health Care, and Consumer Discretionary sector shares led the decline in the first half, the former weigh by GE HealthCare Technologies -5.12%, Becton Dickinson -3.72%, ResMed Inc -3.34%, Baxter International -3.21% and Align Technology -3.18%.

- CarMax -22.21%, Tapestry -4.14%, Ralph Lauren -3.36%, Tesla Inc -3.32% and Deckers Outdoor -3.08% buoyed the Discretionary sector.

- A mix of Technology, Energy and Financial sector shares outperformed in the first half:

- Intel Corp +5.96%, IBM +5.02%, Synopsys +2.74% and Palantir Technologies +2.25%

- EQT Corp +1.65%, Devon Energy Corp +1.05%, Expand Energy Corp +0.98% and Kinder Morgan +0.95%

- Charles Schwab +2.01%, CME Group +1.86%, Northern Trust +1.56% and State Street +1.37%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Larger FX Option Pipeline

Aug-26 15:16

- EUR/USD: Aug29 $1.1600(E1.3bln), $1.1625(E4.0bln), $1.1700(E1.1bln), $1.1725(E1.1bln)

- USD/JPY: Aug29 Y146.50($1.1bln)

- EUR/GBP: Aug29 Gbp0.8563-80(E2.0bln)

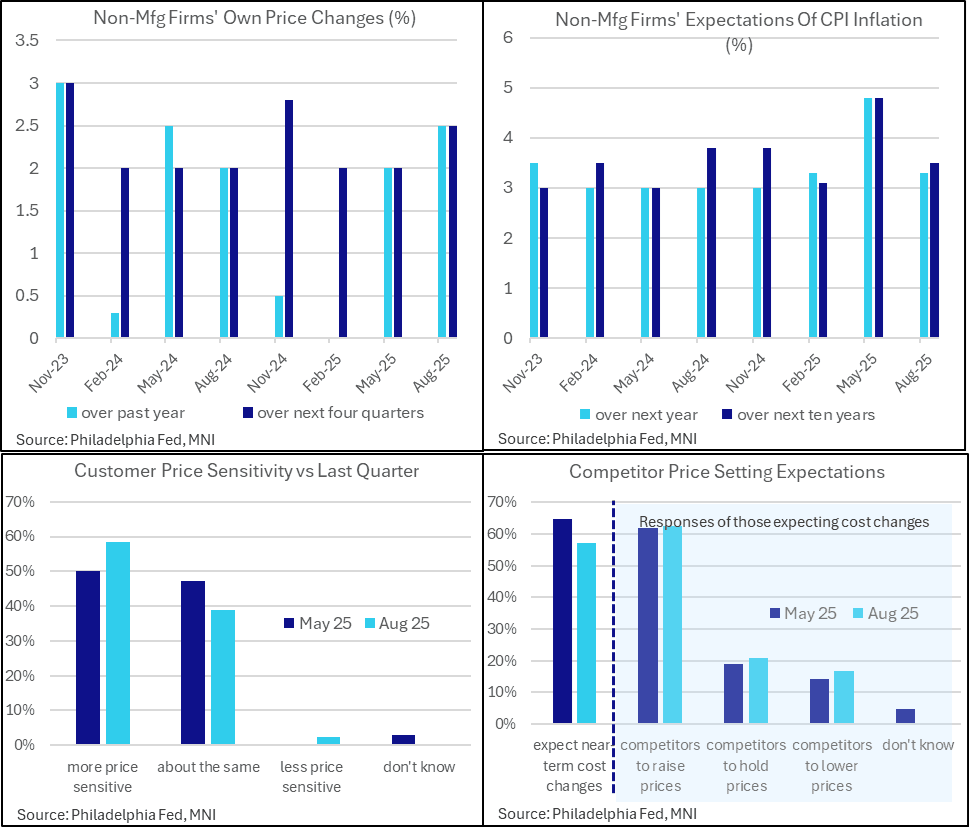

US DATA: Philly Non-Mfg Firms See Faster Price Increases Despite Sensitivity

Aug-26 15:08

- The Philly Fed non-manufacturing survey special questions on inflation expectations show a somewhat similar split in the activity indexes touched upon earlier with their historically large discrepancy between strong firms’ own activity and weak regional activity in August.

- The median firm reported increasing its own prices by 2.5% over the past year, up from 2.0% in the May question and having essentially paused annual price increases through end 2024/early 2025. It’s the strongest actual increase since the May 2024 survey.

- Own price expectations also firmed from 2.0% to 2.5%, above a typical median of 2% in surveys over the past almost two years but not an unprecedented level.

- Firms’ expectations of consumer inflation meanwhile cooled from a particularly strong May release, with those for the next year reverting to 3.3% from 4.8%. Ten-year ahead expectations also cooled to 3.5% after 4.8%, still above the 3.1% in February prior to reciprocal tariff announcements but within ranges.

- Elsewhere, these non-manufacturing firms reported greater price sensitivity over the quarter (59% reported higher sensitivity vs 50% in May) and fewer expect cost changes over the near-term (57% vs 65%). Of those that do expect cost increases, a similar almost two thirds expect those to be higher, with price changes over a median 3 months vs 2.5 months in the May survey.

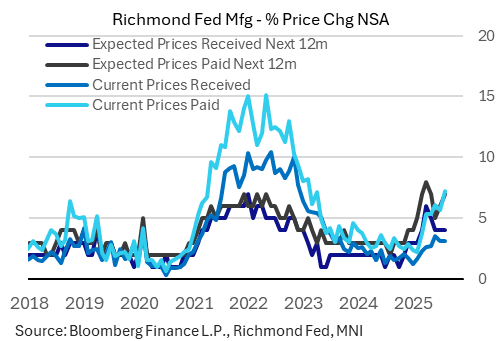

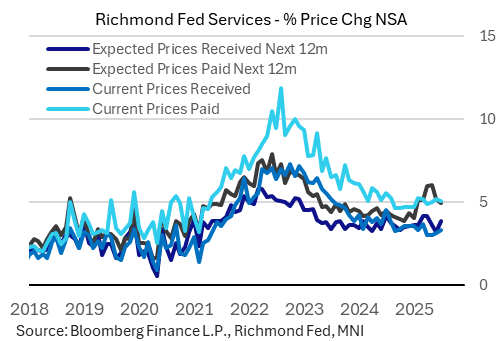

US DATA: Manufacturing Price Pressures More Acute Than For Services (2/2)

Aug-26 15:04

Looking across both the Richmond Fed's services and manufacturing surveys, there was a divergence in indicated price pressures, suggestive of tariffs feeding through to manufacturers more immediately.

- The Richmond Fed's manufacturing prices paid rose to a 28-month high 7.2% (reflecting changes over the prior 12 months), up from 5.7% prior; prices received were relatively steady at 3.1% (3.2% prior anda 2nd consecutive decline). 12-month expected prices paid rose for a 3rd consecutive month to 7.0% (6.0% prior, still below April's 8.0% high), with expected prices received at 4.0% for a 3rd month.

- For services firms, current prices paid ticked down 0.1pp to 5.1% (from 5.2%), with current received up to a 4-month high 3.3% (3.2% prior).

- Expected prices paid pulled back to a 6-monthlow 4.9% (5.2% prior), with expected received up to a 3-month high 3.9% (3.2% prior).