EQUITY TECHS: E-MINI S&P: (Z5) Trades Through The 20-day EMA

- RES 4: 7000.00 Psychological round number

- RES 3: 6993.12 3.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6974.04 3.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 1: 6953.75 High Oct 30 and the bull trigger

- PRICE: 6789.25 @ 07:25 GMT Nov 5

- SUP 1:6748.50 Intraday low

- SUP 2: 6702.18 50-day EMA

- SUP 3: 6690.75 Low Oct 22

- SUP 4: 6571.25 Low Oct 17

The trend condition in S&P E-Minis is unchanged, it remains bullish and the latest pullback appears corrective. Support at the 20-day EMA, at 6803.81, has been breached. A clear break of this average signals scope for a deeper retracement and exposes the 50-day EMA at 6702.18 - a key pivot support. The bull trigger has been defined at 6953.75, the Oct 30 high. Clearance of this hurdle would confirm a resumption of the uptrend.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY OPTIONS: Estoxx Put Spread

SX5E (21st Nov) 5550/4800ps, bought for 66.3 in 4k vs 1.24k at 5660.00.

MNI: EUROZONE SEP CONSTRUCTION PMI 46.0 (46.7 AUG)

- MNI: EUROZONE SEP CONSTRUCTION PMI 46.0 (46.7 AUG)

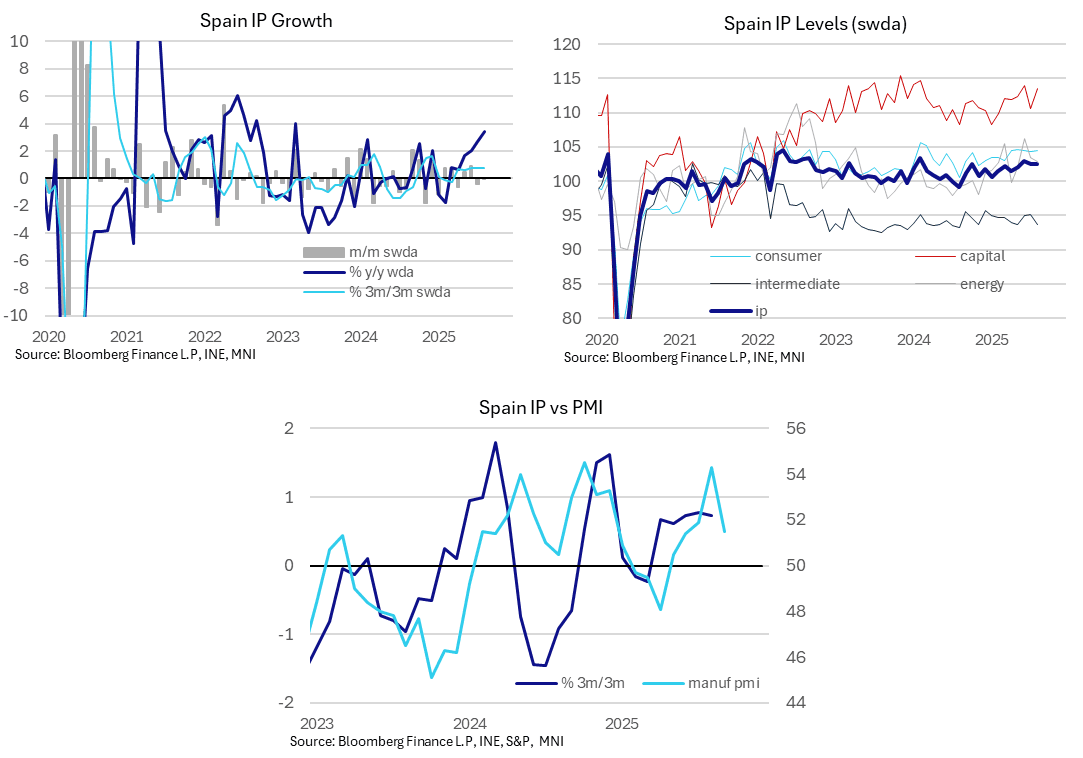

SPAIN DATA: Another Small Decline In IP, But Underlying Signals Remain Positive

Spanish industrial production fell 0.1% M/M SA in August, the second consecutive sequential decline. Only three analysts had submitted forecasts for the print, with estimates ranging from -0.2% to +0.7% M/M. Though sequential growth rates have been negative for two months now, 3m/3m and Y/Y comparisons remain in positive territory. Furthermore, signals from the manufacturing PMI suggests underlying IP momentum remains positive.

- Across sub-components, August’s M/M fall was centred in intermediate goods (-1.5% M/M) and energy (-0.7% M/M). There was a solid 2.6% increase in capital goods production, but this followed a 2.9% fall in July. Consumer goods production was +0.2% M/M, after -0.1% in July and -0.3% in June.

- Annual SA industrial production growth was 3.4% in August, up from 2.7% in July (revised up from 2.5% initial). This was the strongest Y/Y rate in over two years.