CNH: Downtrend Flattens Out, CNH/JPY To Fresh Highs, Dec Trade Today

Spot USD/CNH couldn't sustain sub 6.9700 levels as Tuesday trade unfolded. Broader USD sentiment was...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

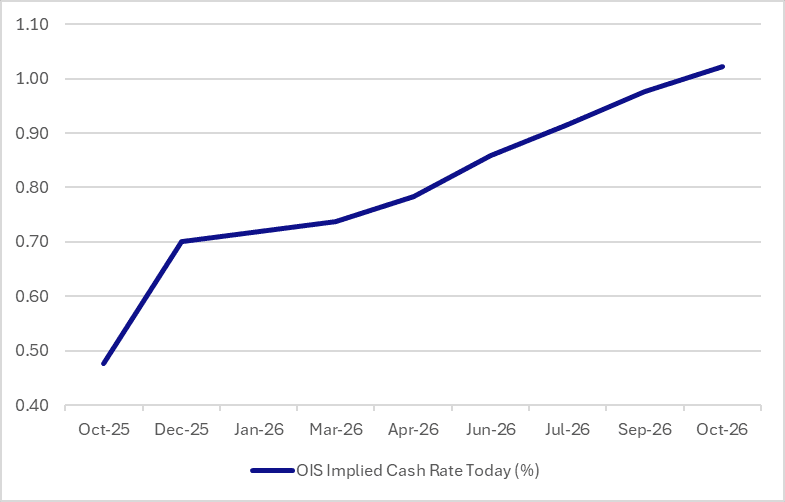

US TSYS: Curves Steepest since in 3-Years Post Fed, Ahead of This Week's Data

US bond futures finished the week last week on the back foot, down at 112-07+. This represented a -11+ decline for TYH6 as it retraced back to the mid-point of the 100-day EMA at 112-14+ at the topside and the 200-day EMA at 111-29+ as the downside resistance. TYH6 has opened at

- The 2-Yr finished at 3.52% Friday, -4bps for the week

- The 5-Yr finished at 3.743%, +3bps for the week

- The 10-Yr finished at 4.185%, +5bps for the week.

- The 30-yr finished at 4.84%, +5bps for the week.

The 2s10s curve finished +8bps up for the week at +65, the steepest since 2022. The curve steepening has extended post the FOMC as hawkish risks unwind, and markets focus on the longer term prospects for inflation. US markets will have one eye on the BOJ decision later this week also

Tonight markets will focus on Empire Manufacturing (exp 10.0 vs prior 18.7), preliminary PMIs for December, November CPI but the key event later in the week Non Farm Payrolls for November.

Tonight sees a US$86bn 13-week bill and a US$77bn 26-week bill auction.

AUSSIE 10-YEAR TECHS: (H6) Marked Lower

- RES 3: 95.982 - 76.4% retracement Sep’24 - Nov’24 downleg

- RES 2: 95.960 - High Apr 7 (cont.)

- RES 1: 95.900 - High Oct 17

- PRICE: 95.195 @ 16:03 GMT Dec 12

- SUP 1: 95.120 - Low Dec 10

- SUP 2: 95.087 - 2.0% Lower Bollinger Band

- SUP 3: 94.276 - 1.0% 10-dma envelope

Aussie 10-yr futures remain well toward the bottom of the recent range, having taken out all major support levels in the process. With 95.275 cleared, prices are pushing to new contract lows, opening vol-band support through 95.087 and into 94.276. Any recoveries need to break back above 95.900 to signal near-term bullish traction.

JGBS: Futures Closed Stronger Overnight On Friday, Tankan Survey Out Today

In post-Tokyo trade on Friday, JGB futures closed stronger, +5 compared to settlement levels, after US tsys finished with a twist-steepener, with yields 2bps lower and 4bps higher, as Fed speakers returned from the Blackout.

- MNI BOJ WATCH: The Bank of Japan Board will strongly consider raising the policy rate by 25 basis points to 0.75% at the Dec 18-19 meeting. The BOJ is also expected to maintain its stance that it will consider additional rate increases only after monitoring the impact on the economy, inflation and the financial environment for around six months. Markets see the Board raising the rate to 1% by October at the latest. Markets are focused on how the BOJ will refer to the neutral interest rate.

- Today, the local calendar will see the Tankan Survey and the Tertiary Industry Index.

- The Q4 Tankan survey comes ahead of this week's BoJ meeting outcome, but only a drastic surprise (on the downside) would shift the central bank's thinking (with a hike increasingly priced in over the past week). Still, the Tankan report will inform the 2026 outlook, with a focus on both current conditions and the capex outlook. The government recently announced a stimulus package, mostly aimed at cost-of-living measures, but it clearly has a pro-growth agenda. Market forecasts are relatively steady compared to Q3 outcomes.

Source: Bloomberg Finance LP / MNI