PERU: Door Still Open To BCRP Rate Cut Next Week, Amid Concerns over FX Strength

Dec-05 13:07

- With USDPEN continuing to hold near multi-year lows, the BCRP has continued to intervene in the FX market this week, buying an additional $294mn in the spot market yesterday. In addition, it rolled off approx. $230mn in FX swaps. USDPEN edged up into the close to finish the session broadly unchanged around 3.36.

- BBVA says that the BCRP’s intervention continues to cap PEN appreciation, with 3.36 remaining a strong near-term support, while 3.40 marks a robust topside resistance.

- The continued strength of the PEN remains a downside risk to the inflation outlook. With inflation already hovering close to the bottom of the central bank’s 1-3% target range, this keeps the door open to a 25bp rate cut next week – although the BCRP has emphasised that the policy rate is already very close to neutral. A slight majority of analysts currently lean towards a 25bp cut on Dec 11, according to Bloomberg.

- Separately, the government has said it has presented a suggestion to extend the Reinfo mining permit scheme for informal miners by one year. This comes amid ongoing protests by informal miners demanding an extension to the scheme, which is awaiting a debate in Congress. Last month, a congress commission approved a two-year extension to the scheme.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Repo Reference Rates

Nov-05 13:05

- Secured Overnight Financing Rate (SOFR): 4.00% (-0.13), volume: $3.147T

- Broad General Collateral Rate (BGCR): 3.98% (-0.11), volume: $1.183T

- Tri-Party General Collateral Rate (TCR): 3.98% (-0.11), volume: $1.156T

- (rate, volume levels reflect prior session)

PIPELINE: Corporate Bond Roundup: KEPCO, Santos Finance on Tap

Nov-05 13:03

- Date $MM Issuer (Priced *, Launch #)

- 11/05 $Benchmark KEPCO 3Y SOFR+62, 5Y +47

- 11/05 $Benchmark Santos Finance 10Y +195a

- $5.7B Priced Tuesday

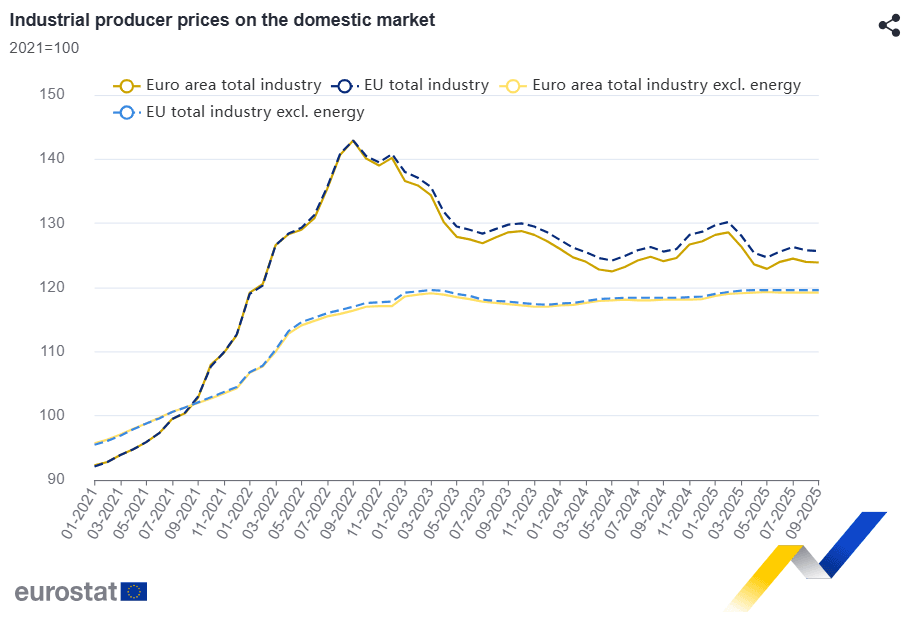

EUROPEAN INFLATION: PPI ex-Energy Continues To Hover Around 1.0% Y/Y Handle

Nov-05 13:01

Eurozone PPI inflation was as expected in September, at -0.2% Y/Y after August's -0.6% was the first negative Y/Y rate since last November.

- Energy deflation tapered off a little to -2.4% Y/Y (-4.1% August).

- This left PPI ex-energy little changed vs August, at 0.9% Y/Y, having hovered around the 1.0% handle for six months now.

- None of the underlying non-energy categories saw a directional jump in September, with the largest deviation vs August seen in Intermediate goods, printing 0.1% Y/Y (0.3% prior). Capital goods, durable consumer goods and non-durable consumer goods all remained within 0.1pp of their August prints, at 1.8%, 1.6% and 1.9% (all Y/Y), respectively.

- Analysts generally expect little pipeline pressures in HICP core goods ahead, leaving energy developments as one of the main potential directional drivers of Eurozone PPI in the coming months.