FOREX: Dollar Index Erases Gains as Equities Reverse Lower

Jan-02 15:48

- A sharp move lower for major equity benchmarks has been highlighted by the e-mini S&P briefly slipping into negative territory on the session in recent trade. With appetite in the currency markets limited following the holiday break and ahead of the weekend, this dynamic has weighed on the dollar, with the DXY erasing its prior moderate gains.

- This has helped USDJPY edge away from short-term resistance at 157.00, while EURUSD now stands 25 pips above the 1.1713 session lows. GBPUSD has had the most notable bounce, rising around 50 pips to approach the 1.35 handle once more.

- GBPUSD’s pause in late December appears to be a flag formation - a bullish continuation pattern. This theme has been bolstered by the pair holding the 20-day EMA in recent sessions, which currently intersects at 1.3425. Note that moving average studies have recently crossed and are in a bull-mode position, highlighting a dominant uptrend.

- Softer equity price action has relatively weighed on AUDUSD, which has been unable to extend its rally amid the weaker greenback. Despite this, AUD remains the best performer across the G10 complex, keeping sights on the recent cycle highs at 0.6728.

- In emerging markets, both MXN and ZAR have remained resilient through the equity turnaround, both rising ~0.6% on the session. For USDMXN, a move below 17.8816 would place spot at the lowest level since July 2024.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

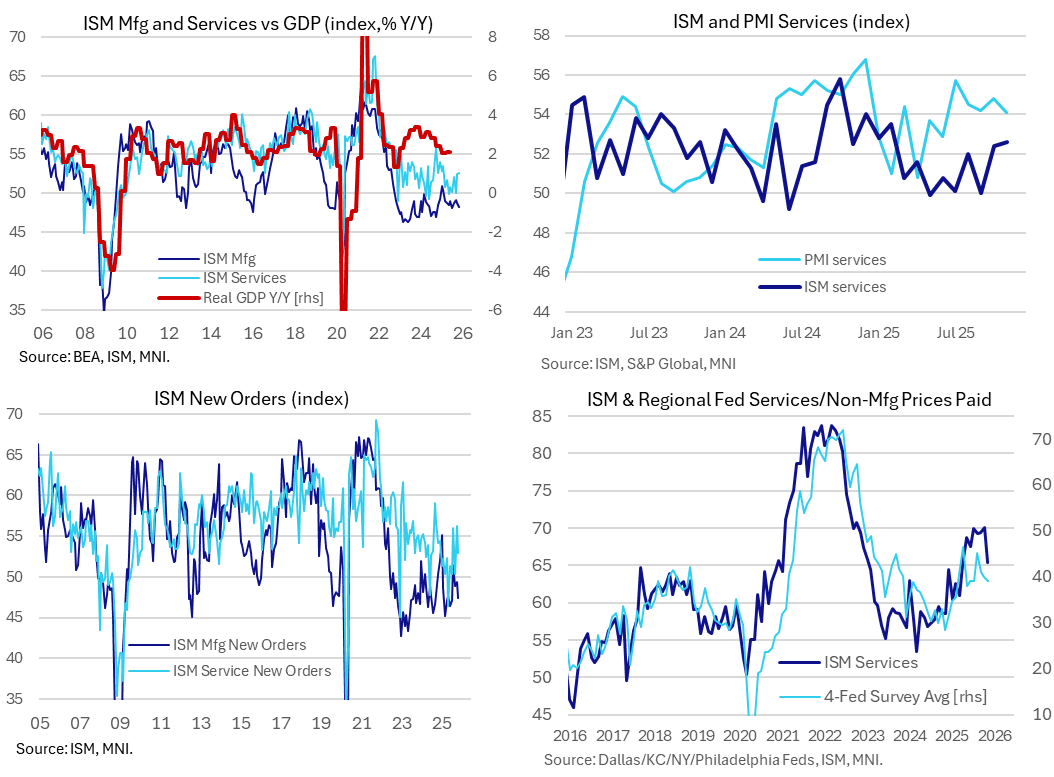

US DATA: ISM Services Beat Countered By Declines In Some Key Components

Dec-03 15:34

The ISM services report was stronger than expected in November although saw some conflicting developments in the main components, with new orders and prices paid slipping but employment increasing to a six-month high (albeit still in contractionary territory).

- The ISM services index was stronger than expected in November as it inched higher to 52.6 (cons 52.0) after 52.4 in October, marking its highest since February.

- The S&P Global US services PMI continues to offer a more optimistic assessment of current activity despite being revised down in its final November release to 54.1. That said, the 1.5pt outperformance is the smallest gap since the ISM survey briefly overshot it in April.

- Twelve industries reported growth last month, led by retail trade, entertainment and recreation, and accommodation and food services. Five contracted, including construction.

- New orders fell 3.3pts to 52.9 after a twelve-month high of 56.2 in October, but it’s hard to take a signal from here after some particularly volatile months where it’s swung between 50 to 56 handles in each month since July.

- Orders are a clear area when the PMI report is more optimistic, noting "Activity was supported by the firmest rise in new work of 2025 so far, whilst confidence in the outlook strengthened following the end of the government shutdown and expectations of improved economic growth in the year ahead."

- Prices paid saw a more notable 4.6pt decline to 65.4 after the 70.0 in October poked above 69.9 in July for the highest since Oct 2022. It’s the lowest since April but is still elevated historically, for instance following 58.7 in 2024 and 57.5 in 2019 for longer-term context).

- As noted beforehand, regional Fed service surveys pointed to downside risk for prices paid, as has been the case through 2H25, but the services PMI saw a sharp uptick in input cost inflation, even after a downward revision in the final S&P Global release just before the ISM release.

- The employment index meanwhile logged a fourth consecutive monthly increase to 48.9 (+0.7pts), still in contractionary territory but a six-month high.

GILT AUCTION PREVIEW: On offer next week

Dec-03 15:32

The DMO has announced it will be looking to sell GBP4.5bln of the 4.75% Oct-35 Gilt (ISIN: GB00BTXS1K06) at its auction next Wednesday, December 10.

STIR: Market Still Prices Over 90% Odds Of Dec Cut, No Reaction To ISM

Dec-03 15:26

Little net reaction in the USD short end following the mixed ISM services report, which won’t have changed the picture for the Fed (with elevated inflation and questions surrounding the health of the labor market remaining intact).

- To recap, while the headline index and was firmer-than-expected, the prices paid component (while still elevated at 65.4) came in on the softer side of expectations. Meanwhile, the new orders subindex showed a slower rate of expansion and the employment subindex showed a slightly reduced rate of contraction.

- Fed Funds continue to indicate 23.5bp of easing for this month, 32bp through January, 40bp through March, 48bp through April and 62.5bp through June.

- SOFR futures 0.25-3.0 firmer on the day vs. 0.25-3.5 firmer heading into the ISM release.

- Implied terminal rare pricing 3.025% after threatening to break below 3.00% earlier.