STIR: $-Bloc Markets Muted Over the Past Week Despite Tariff Headlines

Mar-28 03:01

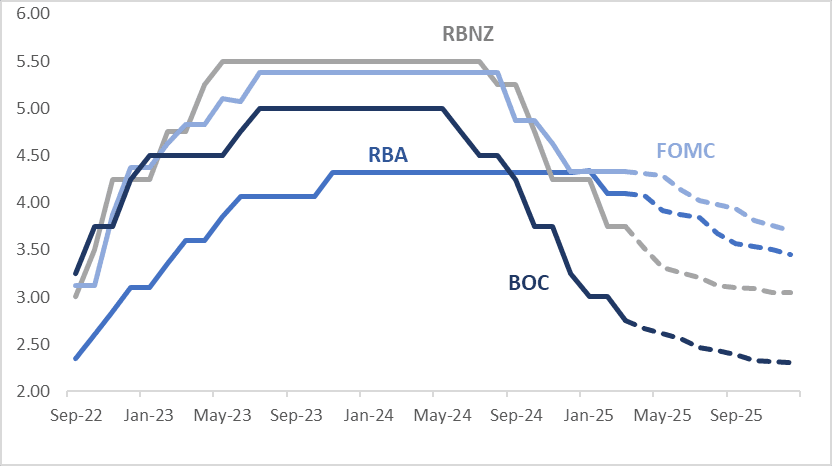

In the $-bloc, rate expectations through December 2025 remained largely stable over the past week. Pricing firmed by 2–3bps in the US, Canada, and Australia, while New Zealand saw a 4bp softening.

- Ahead of next Tuesday’s RBA policy decision, February’s headline CPI (released Wednesday) rose 0.1% m/m (seasonally adjusted), bringing year-on-year inflation to 2.4%, down from 2.5% in January. Inflation has hovered around this level for the past three months.

- With various state and federal electricity rebates in effect, attention shifted to the underlying trimmed mean, which moderated by 0.1pp to 2.7% y/y. The Q1 inflation report is due on April 30, with the RBA forecasting core inflation at 2.7%. This outcome will be a key factor in the May 20 RBA decision.

- Elsewhere in the $-bloc, it was a relatively light week for data, though US fiscal policy dynamics, particularly tariffs, remained in focus. Ongoing expectations for two US rate cuts in 2025 continue to be driven by concerns that a collapse in sentiment could trigger a recession.

- Looking ahead to December 2025, the projected official rates and cumulative easing across the $-bloc are as follows: US (FOMC): 3.68%, -65bps; Canada (BOC): 2.28%, -47bps; Australia (RBA): 3.42%, -68bps; and New Zealand (RBNZ): 3.09%, -66bps.

Figure 1: $-Bloc STIR (%)

Source: MNI – Market News / Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FLOWS: BLOCK - Likely Seller UXY

Feb-26 02:59

- -4,604 UXY at 113-19+, DV01 $406k. Contact trades -08 at 113-16+ last

- 1

CHINA: The Control of Liquidity is Pushing Yields Gently Higher

Feb-26 02:51

- On January 10 the PBOC paused their policy of purchasing government bonds in place to support liquidity.

- That week, the close for the CGB 2yr hit a low of 1.03% and the 10YR 1.59%

- Since that time two major themes have become evident. The provision of significant liquidity leading into the earlier than usual Lunar New Year holiday, and the gradual withdrawal since.

- A controlled rise in the Overnight interbank rate has accompanied this withdrawal of liquidity post Lunar New Year.

- This has resulted in a gradual, measured ascent of bond yields with the CGB 2yr today at 1.45% and the CGB 10yr at 1.76%.

- As China’s top legislature begins its annual parliamentary meeting on March 5, expectations for policy announcements are high.

- With the policy setting for monetary policy deemed accommodative going forward, China could cut its policy rates early next month.

- The controlled rise in interest rates comes at a time when demand for bonds (and bond funds) has been growing, particularly from retail investors concerned about the property market. Notwithstanding the recent rebound in local equities, which could also be drawing away funds from the local bond market.

- A cut in interest rates could see bond yields move lower again and the gradual rise in yields in advance of monetary policy changes, appears a sensible policy intervention to avoid a bubble arising in bonds.

STIR: RBA Dated OIS Pricing Mixed Vs. Pre-RBA Levels After CPI Monthly

Feb-26 02:25

RBA-dated OIS pricing is softer for late 2025 / early 2026 meetings today.

- As a result, pricing remains mixed compared to last Tuesday’s pre-RBA levels—meetings through July are flat to 4bps firmer, while those beyond are 2-8bps softer.

- January headline CPI inflation printed slightly lower than expected at 2.5% y/y, in line with December. However, the underlying trimmed mean rose 0.1pp to 2.8%, but still below the top of the RBA’s 2-3% band. The first month of the quarter has limited updates for services inflation. The seasonally adjusted data is consistent with the RBA remaining cautious with it stating that “upside risks remain”.

- Markets assign an 11% probability to a 25bp rate cut in April, with a cumulative 56bps of easing priced by year-end, based on an effective cash rate of 4.09%.

Figure 1: RBA-Dated OIS – Today Vs. Pre-RBA Levels

Source: MNI – Market News / Bloomberg