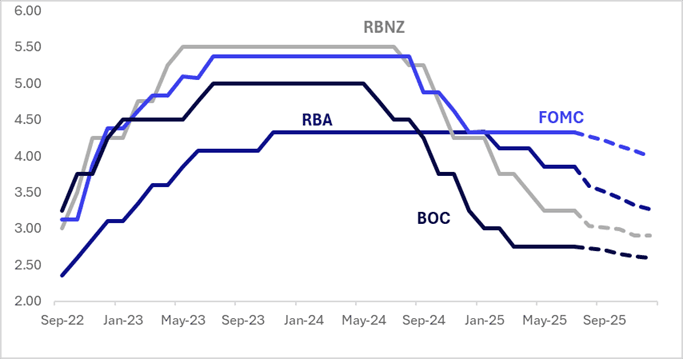

STIR: $-Bloc Markets Little Changed over Past Week Apart From US Firming

Interest rate expectations across the$-bloc economies were broadly stable over the past week, except for the U.S., where rates firmed by 11bps.

- The July FOMC decision included a subtle shift, hinting that the Committee may be laying the groundwork for a potential rate cut in September. However, Chair Powell used much of the post-meeting press conference to downplay that possibility. As a result, markets scaled back expectations for near-term easing, with the probability of a September cut falling to around 50% by the end of the session, down from roughly 60% beforehand.

- In Canada, the Bank of Canada (BoC) held its overnight rate steady at 2.75% in July, as expected. Markets interpreted the decision as mildly dovish, with a modest increase in the likelihood of a rate cut by year-end. Although Governor Macklem stated that little had changed since the June meeting, the accompanying statement struck a more dovish tone when reviewing developments since the start of the year.

- Looking ahead, the next key regional event is the RBA decision on August 8. After this week’s Q2 underlying CPI undershoot, the market is assigning a 97% probability to a 25bp rate cut at the upcoming meeting.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 4.00%, -33bps; Canada (BOC): 2.60%, -16bps; Australia (RBA): 3.26%, -59bps; and New Zealand (RBNZ): 2.90%, -35bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

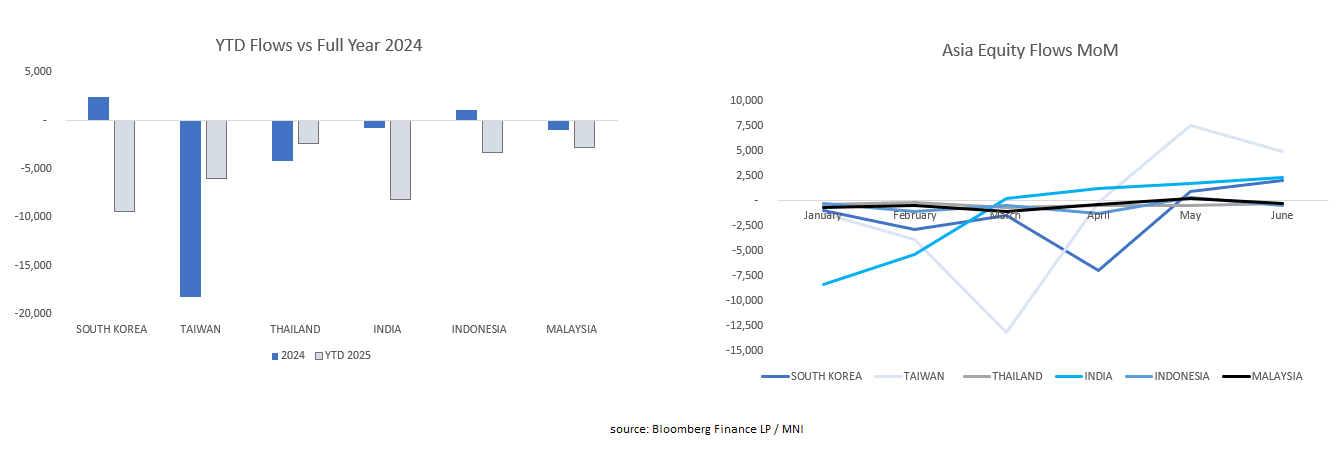

ASIA STOCKS: Is the tide Coming Back in for Asia Stock Flows

- We report each day the flow data for major regional bourses which suffered heavily under the threat of tariffs.

- However in recent months we have seen strong inflows into Taiwan, India and South Korea, and whilst year to date flows remain negative there appears sufficient evidence to ask whether the worst is over for outflows for major regional bourses.

- The flows began to turn positive when tariffs were paused in April with Taiwan the biggest beneficiary thanks to its semi-conductor manufacturers.

- USD weakness is a potential positive catalyst for the second half of 2025 for Asia flows, particularly if trade agreements are reached.

AUSSIE BONDS: Cheaper, Narrow Ranges, Heavy US Calendar Today & Tomorrow

ACGBs (YM -3.0 & XM -3.0) are modestly weaker on another subdued day of trading.

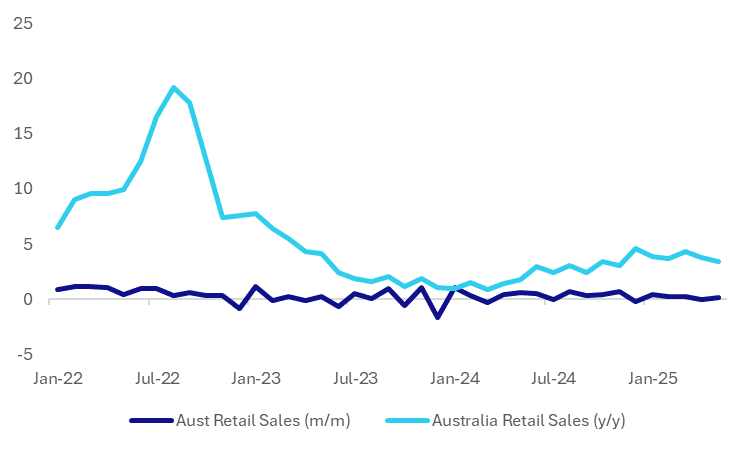

- Australian retail sales rose a modest 0.2%m/m in May, after a revised flat outcome in April (originally reported as a -0.1% dip). The market consensus for the May outcome was a +0.5% rise. Other data showed May building approvals up 3.2%m/m, which was slightly below the 4.0% forecast. The April fall was revised to -4.1%m/m.

- Building approvals rose 3.2% m/m (estimate +4.0%) in May versus a revised -4.1% in April.

- Cash US tsys are little changed in today’s Asia-Pac session after yesterday’s twist-flattener. Wednesday's US data focus is on MBA Mortgage Applications at 0700ET, Challenger Jobs at 0730ET followed by ADP Employment Change at 0815ET. No Fed scheduled Fed speakers. Thursday is a heavy data day with NFP added due to Independence Day holiday closure on Friday.

- Cash ACGBs are 2-3bps cheaper with the AU-US 10-year yield differential at -11bps.

- The bills strip has bear-flattened, with pricing -1 to -4.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in July is given a 95% probability, with a cumulative 82bps of easing priced by year-end (based on an effective cash rate of 3.84%).

AUSTRALIA DATA: Retail Momentum Softens Further In May, Despite Clothing Bounce

Australian retail sales rose a modest 0.2%m/m in May, after a revised flat outcome in April (originally reported as a -0.1% dip). The market consensus for the May outcome was a +0.5% rise. Other data showed May building approvals up 3.2%m/m, which was slightly below the 4.0% forecast. The April fall was revised to -4.1%m/m.

- By sub category we had strong rebounds in both apparel retail sales and department store spending. Both categories were up close to 3%m/m, but this follows similar falls in April.

- The ABS noted: "‘Clothing retailers and department stores were boosted by people buying winter clothes, having held off on those purchases with the warmer-than-usual weather last month,’ Mr Ewing said."

- Otherwise, spending trends were either flat or down a touch. Notably food retailing fell by 0.4%m/m, after declining 0.2% in April.

- The y/y pace eased to 3.4% from 3.8% in April, see the chart below. The general trend in spending momentum is too moderate after last year's fiscal impulse for households helped drive a brief strengthening.

- The RBA meets next week, and the market has a 25bps cut priced in. Today's data is likely to reinforce easing expectations at the margin.

- Note this is the second last retail sales release, with the release to be replaced by the household spending series (the next update for this print is on Friday).

Fig 1: Australia Retail Sales Momentum Eases Further

Source: Bloomberg Finance L.P./MNI