US FISCAL: DISP Extension, June Tax Take Puts September X-Date In Focus

Treasury informed Congress late Wednesday that it is required to extend its debt issuance suspension period ("DISP") from a Jun 27 end-date, to Jul 24. This is a technicality in which Treasury has to inform Congress that it will have to continue to make use of "extraordinary" measures using various federal worker retirement trusts to avoid a debt default so long as the debt limit impasse continues.

- The letter from Treasury Secretary Bessent (PDF here) reiterates that "Based on our current estimates, we continue to believe that Congress must act to increase or suspend the debt limit as soon as possible before its scheduled August recess to protect the full faith and credit of the United States." That recess runs from Aug 4 to Sep 1.

- This is the 2nd extension of the DISP: the first one ran from Jan 21 to Mar 14, which was then extended to Jun 27. The decision to extend to Jul 24, which is less than a month away, suggests to some degree that Treasury anticipates having the debt limit issue wrapped up before the end of July, likely in the reconciliation bill making its way through Congress, though of course they always have the option of extending again at least another week if the fiscal package hits a major obstacle.

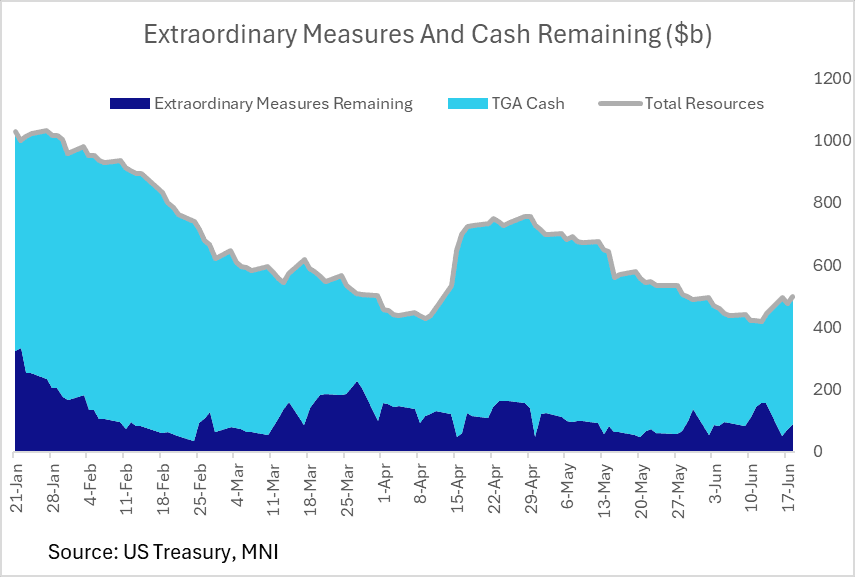

- Realistically, fiscal dynamics so far this year point to potential for Treasury to get into September without running out of cash or extraordinary measures. As of 17 June, Treasury had $409B in cash on hand (up from $260B on Jun 12 due to a key mid-month tax date), which combined with $89B of "extraordinary" measures as of Jun 18 (of $365B total available) makes for around $500B in total resources available asof last week.

- Both JPMorgan and Wrightson ICAP updated on their expected "x-dates" this week - expectations appear to center around early/mid-September in the first instance.

- JPMorgan: "total taxes collected MTD have been tracking close to last year’s, despite our expectation for somewhat weaker receipts....we now think Treasury can make it through August without risking a technical default. We now project the “x-date” to fall on September 2nd, but recognize that given the magnitude of outlays at the beginning of the month, it is possible the “x date” push back further into the second week of September." They also note that SOFR/T-Bill spreads suggest that markets believe the x-date will be in August (bills with August maturities trading relatively cheap to Jul/Sep counterparts).

- Wrightson ICAP: "Our best guess continues to be that the Treasury would be able to scrape by until the September 15 tax date without Congressional action. If so, the influx of quarterly tax receipts would push the X-date back to the beginning of October. As always, though, the range of uncertainty around that forecast is large. We think it is unlikely that the Treasury would actually run out of resources during the Congressional recess in August, but it is not impossible. (And even in our forecast, it’s a close call whether the crunch would come just before mid-September or at the start of October.)"

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: MOF Holding Primary Dealers Meeting June 20: Nikkei

Nikkei reports: "Japan's Finance Ministry will hold a meeting for primary dealers of Japanese government bonds on June 20, Nikkei has learned, and what may be on the agenda is spurring speculation over cutbacks to the ultralong-term bond supply."

- That's of potentially heightened interest given Reuters earlier reporting the MOF will consider skewing the composition of its current issuance programme away from super-long-end instruments (which saw a strong JGB rally overnight).

US: Trump's Approval Rating Continues To Stabilise Amid Low Volume Of Polling

Silver Bulletin notes that President Donald Trump’s approval rating “has improved slightly since the end of April”, noting that the rise is “due in part to a lower-than-usual volume of new polls.”

- Silver Bulletin notes that the positive trend has “reversed over the past few days. He’s 14 points underwater in the latest American Research Group poll, 5 points underwater in the latest Civiqs poll, and 8 points underwater in the latest YouGov/Economist poll. But overall, most pollsters show little change in Trump’s approval rating over the last month.”

- Ruth Igielnik at the New York Times notes: “Our average has shown a slight uptick in President Trump’s approval rating recently. But there have been few high-quality polls in recent weeks, and the ones we have show little change in either direction between April and May.”

Figure 1: President Donald Trump Approval Rating

Source: Silver Bulletin

GERMAN DATA: IFO Sees Slower Pace Of Job Cuts

Released yesterday, the IFO's May Employment Barometer rose to the highest reading since July 2024, at 95.2 points from 94.0 in April. “The labor market is showing initial signs of stabilizing [...] “Whether this turns into a real trend reversal depends largely on further economic developments.”, IFO comments.

- "In industry, the barometer rose for the fifth consecutive month. Overall, however, the majority of companies are continuing to cut jobs. By contrast, service providers are slightly increasing their headcount, with cautious optimism emerging particularly in the temporary employment sector. In the retail sector, however, job cuts continue to predominate. Most companies in the construction industry are also still planning to have fewer employees, although the number of job cuts is also decreasing here."

- A slowing of the deterioration in German labour market conditions was also observed in the hard data recently (see the bottom chart for contributions of quarterly employment growth), with that milder deterioration most notable in sectors other than public services, education and healthcare.

- Monthly German labour data will be released tomorrow - consensus is for unemployment to have ticked up by 12k in May (vs 4k April) and the u/e rate to remain unchanged at 6.3%.