EU CONSUMER STAPLES: Diageo (DGELN) / Asahi (ASABRE): Asset Sale

Dec-17 09:32

Marginal positive for Diageo; reduces ratings risk, although we did not see that particularly reflected in spreads.

Slightly negative for Asahi; it continues to push leverage boundaries, persisting with buybacks following the recent cyberattack. It may exceed ratings thresholds marginally on this but should be able to ride that out if it wishes, with mild deleveraging commitment. Some risk premium is already reflected in spreads.

- Diageo has agreed the sale of stakes in East African beer (EABL) and spirits (UDVK) assets to Asahi for $3bn cash proceeds.

- It sees 0.25x deleveraging from the deal. It targets 2.5-3x and reported 3.4x adjusted as of June 2025. It had expected to reach target by June 2027.

- Asahi acknowledged leverage may exceed its 2.5-3x guidelines; we see 3.7x proforma for FY25, from 3x previously expected. It was already likely to exceed on share buybacks and did not distance itself from continuing that: “we will continue to work to improve financial soundness and enhance capital efficiency, including shareholder returns.”

- It will request exemption from a mandatory takeover of EABL as required under local capital market rules. As minority shareholders position doesn’t change materially, it seems logical to grant that.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

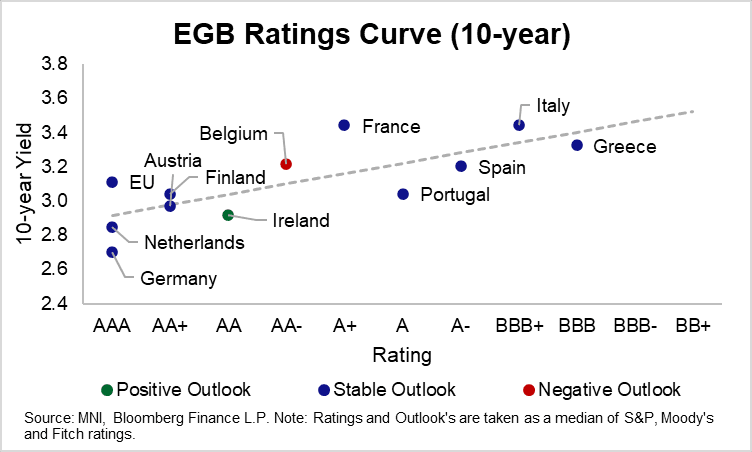

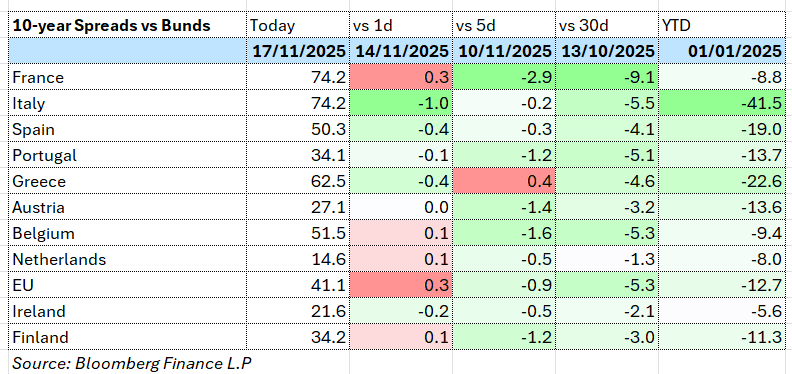

GREECE: Limited Market Impact From Fitch Upgrade; Ratings Trajectory Positive

Nov-17 09:26

- The 10-year GGB/Bund spread is marginally, but not materially, tighter versus Friday's close (around -0.5bps at typing). Fitch's rating upgrade to BBB (Outlook Stable) on Friday was in line with our expectations, and mostly in the price already. GGBs now screen as less rich than before on a simple 10-year yield vs ratings chart.

- The base case is for continued positive ratings action in the coming years. Speaking to the MNI Policy Team last week, a Greek Treasury source said that the next surge in [GGB] demand could come in one or two years’ time, and include Asian investors, “when we will be at BBB+ levels or close to BBB+”.

- Fitch expects Greek debt GDP to fall towards 120% by 2030 - in line with the signals provided by the finance minister last week.

- Meanwhile, planned easing measures in the 2026 budget such as personal income tax cuts "will boost real disposable income of primarily middle-income households, which will in turn support growth"

- Fitch continues to view Greece's commitment to fiscal prudence as "highly credible".

- The conditions for further positive ratings action are unchanged relative to the May review: "Further significant decline in general government debt/GDP over the medium term" and "Improvement in medium-term growth potential and performance".

US TSY FUTURES: FV/WN Steepener Blocked

Nov-17 09:25

Latest block trades lodged at 09:03:49 London/04:03:49 NY:

- FVZ5 4,500 lots blocked at 109-07.25, looks like a buyer.

- WNZ5 1,050 lots blocked at 120-06, looks like a seller.

- Points to a ~$195K DV01 FV/WN steepener.

- 5s30s cash Tsy curve last 101.7bp, set for the highest close seen since October 16.

US TSY OPTIONS: TYF6 112/110 Put Spread Bought

Nov-17 09:09

TYF6 112/110 put spread paper paid 0-27 on 3,550 vs. 112-20 (29% delta).