RIKSBANK: Decision Due At 0830GMT, Unchanged Rates and Guidance Expected

Nov-05 08:05

- The Riksbank decision is due at 0830GMT/0930CET. The Board is almost certain to remain on hold at 1.75%, while reiterating that the policy rate “is expected to remain at this level for some time to come”.

- MNI’s full preview is here

- Since September, there have been several datapoints suggesting an economic recovery is underway, supported by accommodative monetary policy, an anticipated expansion of fiscal policy and declining trade policy uncertainty.

- However, we don't think these developments are enough to shift the Board from its clearly signalled path, particularly at an interim meeting with no updated MPR and rate path projection (only a concise Monetary Policy Update document will be presented).

- Soft signals from the Riksbank's Business Survey and a lack of improvement in hard labour market data should guard against the Board sending too hawkish a signal in November.

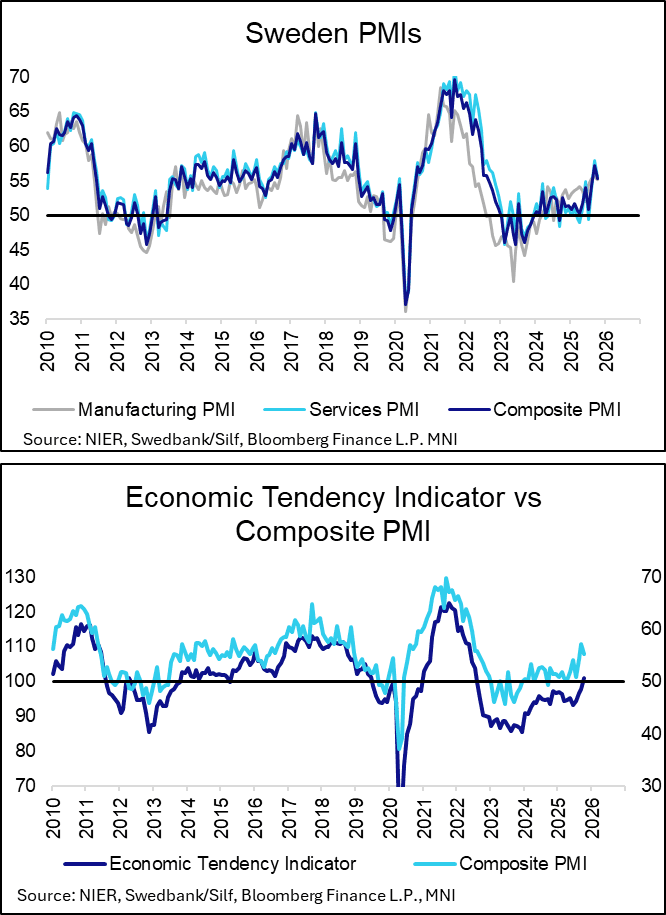

- The October services/composite PMI was released this morning. Although the services print was below the three-analyst strong consensus and last month’s reading (55.4 vs 57.1 cons, 57.9 prior), the composite PMI remains comfortably in expansionary territory (55.3 in October vs 52.7 YTD average). Note that it is still sending a slightly more optimistic signal than the Economic Tendency Indicator.

- Despite these solid aggregate PMI signals, we caveat that the employment indicators in both the manufacturing and services readings fell in October.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Bear Steepening

Oct-06 07:59

Gilts open lower on global cues, after the JGB curve steepened as a new PM was elected and with OATs struggling as French political risks deepen.

- Futures pierce Thursday’s low, basing at 90.51.

- Bears remain in technical control at this stage, particularly with UK fiscal risks lingering. Initial support and resistance in futures still located at 90.26 & 91.28, respectively.

- Yields 2-6bp higher.

- 10s still comfortably within their recent 4.60-4.80% range, last 4.73%.

- 2s10s and 5s30s stick within their respective multi-week ranges, trading ~7bp and ~10bp below their cycle closing highs. Steepening trends intact.

- BoE-dated OIS still shows ~5bp of easing through year-end and is not discounting the next 25bp cut until the end of the April MPC.

- We continue to believe that markets underprice the odds of a Q4 rate cut.

- Comments from BoE Governor Bailey are due today.

- They will be closely scrutinised (even though he spoke as recently as Friday), particularly after Deputy Governors Ramsden & Breeden failed to push back against the idea of rate cuts last week.

- We have previously suggested that Bailey and those two Deputies would probably have to join dovish dissenters Dhingra & Taylor if we were to see a cut in Q4.

- Lower tier construction PMI data is due today.

- Elsewhere, the BoE will sell GBP775mln of short bucket gilts from its APF (3- to 7-Year).

OAT: 10-year OAT/Bund Spread Pierces December 2024 Closing High

Oct-06 07:53

The 10-year OAT/Bund spread has pierced the December 2024 closing high of 87.8bps following Lecornu’s resignation. The spread is now 7bps wider on the session.

- While the timing of Lecornu’s resignation has come as a surprise, his prospects were appearing bleak amid opposition from both sides of the political spectrum during his short (less than 1 month) tenure in office.

- President Macron is now faced with a familiar dilemma in needing to appoint another PM (or face calling a fresh legislative election). Our Political Risk team will provide more colour in due course.

- Clearly, the EC’s deadline for 2026 budget drafts (October 13th) is extremely unlikely to be met by France, further delaying hopes of needed fiscal consolidation.

EUR: EUR/USD Slips Through Horizontal Support on Lecornu Resignation

Oct-06 07:52

- EUR extends losses on the back of that resignation: EUR/USD now through earlier lows as well as the Oct02 low at 1.1683. French equities also see weakness - with the CAC40 easily the underperformer in Europe.

- Lecornu's resignation opening up more criticism from other parties: National Rally's Bardella says the government have shown they have understood "nothing" regarding the country's problems.

- Next major support in EURUSD crosses at 1.1646, the late Sept low. Weakness through here snaps the weak uptrend posted off the August 1st low.