HUNGARY: Dec Inflation Report a More Significant Risk Event After NBH Minutes

- The NBH minutes are rarely a market mover as they tend to repeat guidance from the policy statements/post-decision press conferences. However, this month’s edition offered one particularly interesting line – “The Council was in agreement that the projection in the December issue of the Inflation Report was going to be crucial from the perspective of next year’s monetary policy stance”.

- Although it adds that “tight monetary policy had to be contained”, associating the stance of monetary policy for 2026 with the December Inflation Report could set the stage for a notable dovish shift in tone from the central bank before year-end, and could be contributing to the latest move for EURHUF to new session highs.

- While this is still unlikely to translate into a rate cut before the Spring 2026 elections – particularly given the uncertainty posed by the government’s profit cap measures – the evolution of NBH communication will certainly be worth watching. The central bank meet next on December 16 – and the policy statement will include the key highlights from the quarterly Inflation Report.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

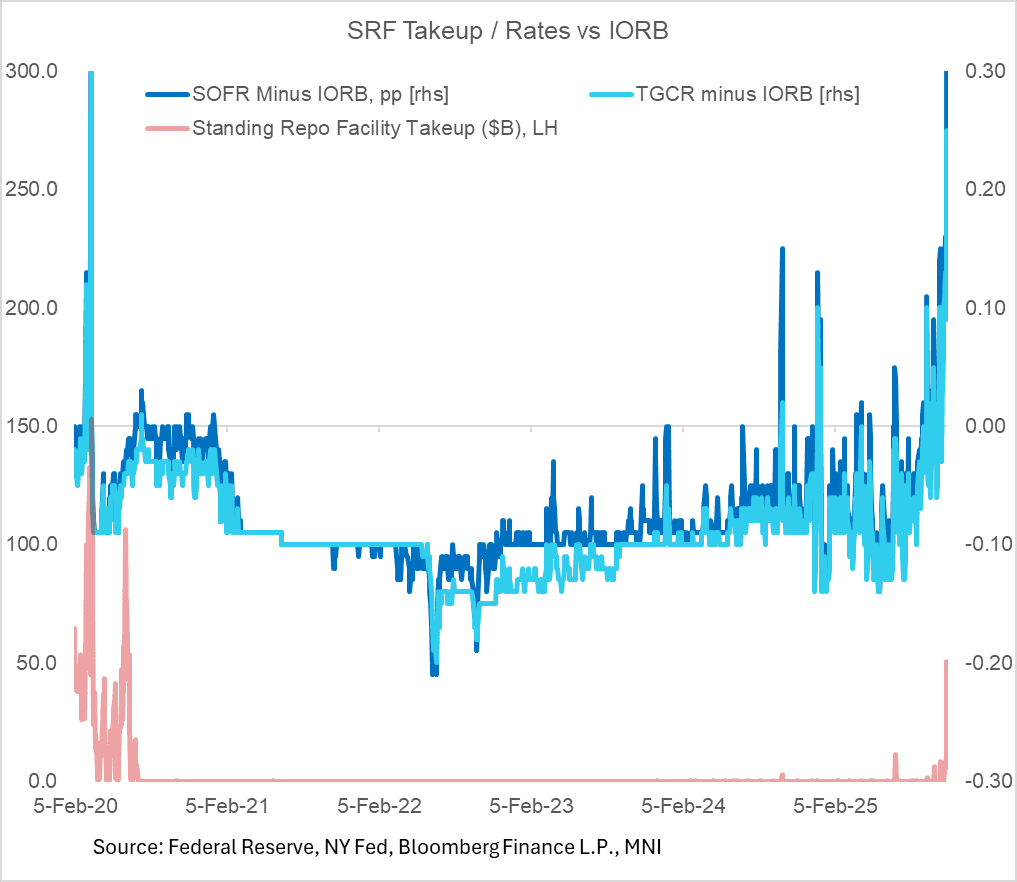

US TSYS/OVERNIGHT REPO: Month-End Secured Rates Soar, To Subside But Not Fully

Funding market rates saw their biggest jump vs Fed administered rates since 2020 on Friday with an 18bp rise in SOFR to 4.22%, well above the Fed's administered rates including the Standing Repo Facility minimum bid rate of 4.00% (takeup in SRF jumped to over $50B Friday, with a similar amount of takeup in the Fed's overnight reverse repo facility).

- SOFR minus IORB (which is 3.90%) jumped from 14bp to 32bp; TGCR minus IORB (arguably watched more closely by some Fed officials) was better behaved but went from 9bp to 25bp. These are bigger increases than most/everyone had expected (we thought SOFR could print somewhere closer to 4.10%).

- This was of course in large part due to month-end pressures as well as $58.3B of net Treasury coupon auction settlements, and we should also mention the Treasury's cash pile rising above $1T which is reserve-draining.

- Secured rates will fall back this week now that month-end is over but SOFR may remain above IORB, with SRF takeup this morning coming in at $15B suggestive of continued market tightness.

- The Fed's end to QT is effective Dec 1, and while they won't be particularly panicked by the month-end surge, we again wonder whether the FOMC will second-guess not announcing that it would conduct temporary open market operations around month-end as some had speculated.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.22%, 0.18%, $3211B

* Broad General Collateral Rate (BGCR): 4.15%, 0.16%, $1153B

* Tri-Party General Collateral Rate (TGCR): 4.15%, 0.16%, $1117B

PIPELINE: Corporate Bond Update: Novartis Capital 7Pt Adding Pressure to Tsys

Adding Novartis 7Pt issuance with prior for comparison:

- Date $MM Issuer (Priced *, Launch #)

- 11/03 $Benchmark Alphabet 8-pt jumbo**: 3Y +60a, 3Y SOFR, +5Y +70a, 7Y +80a, 10Y +90a, 20Y +100a, 30Y +110a, 50Y +135a (massive debt issuance includes $6.5B over 6 tranches: 3Y, 6Y, 7Y, 13Y, 19Y and 39Y).

11/03 $1B Neptune Bidco 5.5NC2 - 11/03 $Benchmark Novartis Capital 7Pt**: 3Y +55a, 3Y SOFR, 5Y +70a, 7Y +75a, 10Y +80a, 20Y +80a, 30Y +90a

- 11/03 $Benchmark UBS 8NC7 +120a, 21.5NC20.5 +115a

- 11/03 $Benchmark Peoples Republic of China 3Y, 5Y

- 11/03 $Benchmark Qatar 3Y +45a, 10Y Sukuk +55a

- 11/03 $Benchmark Kingdom of Jordan 7Y investor calls

- **Piror Alphabet issuance for comparison: $5B on April 28 of this year ($750M 5Y +32, $1.25B 10Y +47, $1.5B 30Y +62, $1.5B 40Y +70) a long stretch since issuing $10B on Aug 3 2020 ($1B 5Y +25, $1B 7Y +45, $2.25B 10Y +58, $1.25B 20Y +73, $2.5B 30Y +88 and $2B 40Y +108)

- **Prior Novartis issuance for comparison: $3.7B on September 16, 2024 ($1B 5Y +45, $850M 7Y +57, $1.1B 10Y +67, $750M 30Y +77)

EURIBOR OPTIONS: Put Condor buyer

0RH6 97.87/97.75/97.68/97.56p condor, bought for 2.5 in 4k.