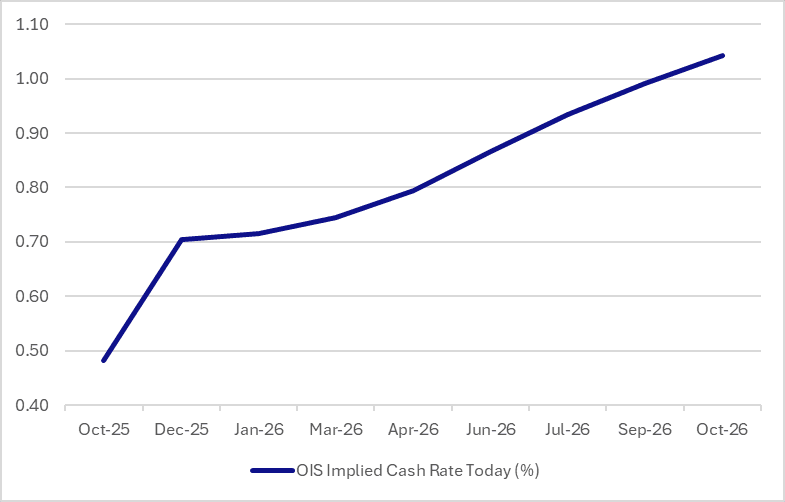

STIR: Dec-26 Leads RBA-Dated OIS' Post-CPI Softening

RBA-dated OIS pricing is 4-12bps softer than Wednesday's pre-CPI levels. * Nonetheless, pricing con...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Mostly Flat, Dec Hike Expectations ~90%

In Tokyo morning trade, JGB futures are weaker, -7 compared to settlement levels, reversing overnight strength.

- Japan’s producer price index rose 2.7% in November from a year earlier, compared with the median forecast of 2.7%. PPI rose 0.3% in November from last month, versus the median forecast of +0.3%.

- (Financial Times) “The Bank of Japan’s governor has said the country’s economy has weathered the shock of US tariffs, supporting market expectations of an interest rate rise at the central bank’s crucial meeting next week.” via BBG

- BOJ-dated OIS currently assigns an 89% probability to a 25bp hike in December, rising to 104% by March 2026 (see chart). As recently as 21 November, markets saw less than a 20% chance of a December move.

- Cash US tsys are slightly richer in today's Asia-Pac session ahead of today’s FOMC policy decision.

- Cash JGBs are flat to 2bps higher across benchmarks, with a steepening bias. The benchmark 10-year yield is 0.5bp higher at 1.970% versus the cycle high of 1.976%.

- Swap rates are ~2bps higher.

Source: Bloomberg Finance LP

USD: BBDXY - USD Drifts Higher Into The FOMC

The BBDXY range overnight was 1212.64 - 1215.70, Asia is currently trading around 1214, -0.02%. US yields continue to extend higher as we approach the FOMC, and both risk and the USD have begun to take notice. The USD continues to see decent demand back toward the 1210-1211 area and it looks like the range 1210-1230 could be here for the moment, or at least until the FOMC. On the day look for resistance again back towards the 1216-1218 area where sellers should remerge initially, a break above here would imply a test of the pivot around 1221-1223. Support remains toward 1210 which needs to be worked through and then the more important 1205 area. Will the Fed provide Christmas cheer and point to further cuts or will a hawkish cut be the Grinch who stole it.

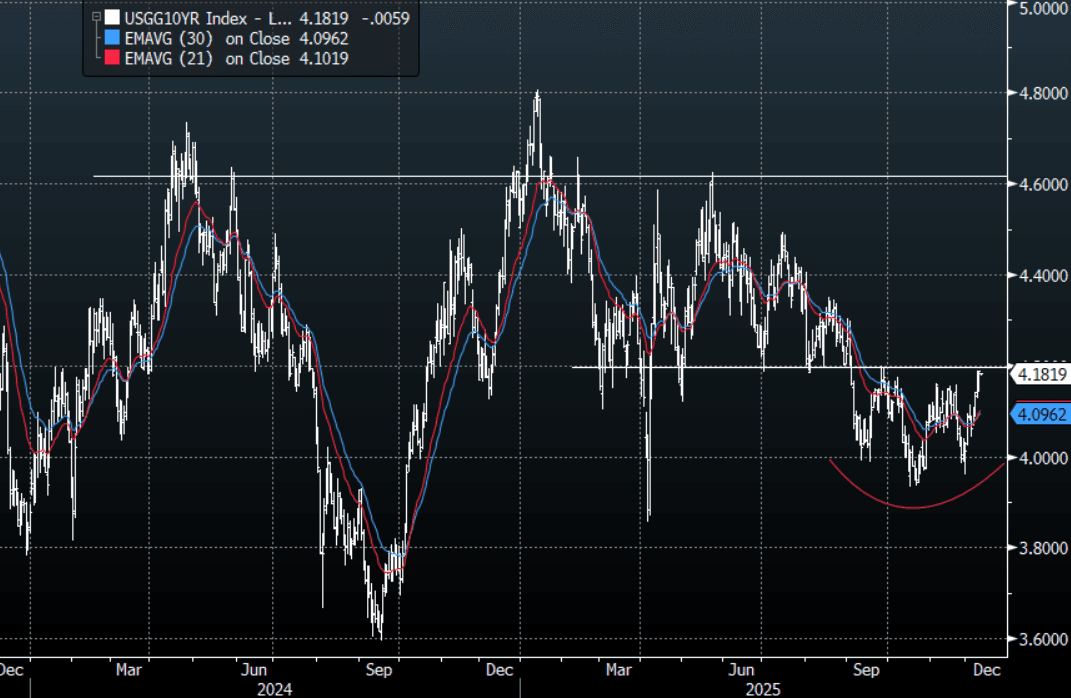

- US 10-year yield is approaching the pivotal 4.20% area so the FOMC will have a big say in whether this area breaks or caps yields going into the end of year. Which has direct implications for the fortunes of the USD.

- MNI: Fed Dots To Show 1-2 Rate Cuts Next Year - Ex-Officials. A fragile consensus for a December interest rate cut from the Federal Reserve is likely to produce a negotiated pause for early 2026, with the center of the FOMC projecting one to two more steps down toward neutral in 2026, former Fed officials told MNI.

- The BBDXY Average True Range for the last 10 Trading days: 317 Points

Fig 1: U.S. 10-Year Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSTRALIA: Nov Unemployment Rate Forecasts Split Between Rise & Unchanged

With the RBA saying this week that “recent data suggest the risks to inflation have tilted to the upside, but it will take a little longer to assess the persistence” and noting signs of capacity pressures, the data before the 4 February decision will be key to the policy outlook. This begins with Thursday’s November job figures.

- The RBA doesn’t just look at the headline employment and unemployment but also the underemployment & youth unemployment rates as well as hours worked. The split between full-time and part-time will also be important.

- Bloomberg consensus is forecasting a 20k rise in employment after October’s 42.2k. Forecasts range from 10-40k with most around 15-25k. Westpac is at consensus, while ANZ is below at +15k and CBA & NAB above at +25k.

- The series is volatile and can easily surprise in both directions but annual growth has slowed over 2025. Therefore it is important to look at the 3-month average, which RBA Governor Bullock has recommended. In October, the average was +15.1k.

- The unemployment rate is projected to rise 0.1pp to 4.4% but 9 analysts expect it to be stable at 4.3% with 15 forecasting 4.4%. Westpac is in line with consensus, while ANZ, CBA and NAB all expect it to remain at 4.3%.

- The participation rate is forecast to be unchanged at 67.0%.