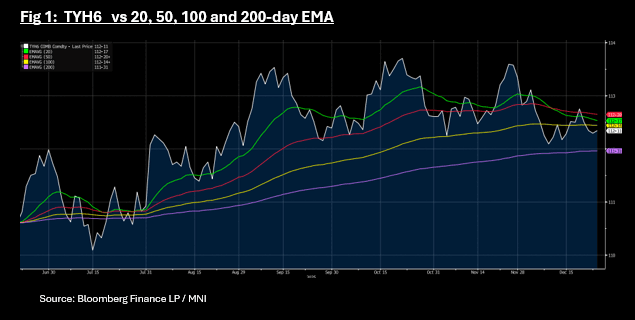

US TSYS: Data Pushes Yields Higher Overnight, Market Looks to June for Next Cut

The US 10-Yr bond future finished down -01 at 112-09+ overnight, with most moves seen in cash trading. TYH6 remains wedged between the topside resistance of the 100-day EMA of 112-14+ and the downside resistance of the 200-day EMA at 111-31. TYH6 has opened up in the Asia trading day at 112-09 with volumes extremely low and has edged higher to 112-11+. TYH6 remains wedged between the topside resistance from the 100 day EMA of 112-14+ and the downside resistance from the 200-day EMA of 111-31.

Treasuries finished mixed overnight, curves twist flatter (2s10s -1.733 at 63.666) with 2s-10s weaker vs. modest gains in Bonds. Futures gapped lower after stronger than expected economic data while projected rate cut pricing in-turn consolidated with the June '26 now the first FOMC date to price in a 25bp cut.

Cash is modestly better today with yields -0.5 -0.8bps lower, with volumes low.

- The 2-Yr was up +3.1bps overnight to 3.534%, and is currently 3.533%

- The 5-Yr was up +2.3bps to 3.737%, and is currently 3.731%

- The 10-Yr was flat at 4.167%, and is currently 41.59%

- The 30-Yr was down -1.2bps at 4.826%, and is currently 4.82%

- The US$70bn 5-Yr auction was in line with yield expectations as yields crept higher during the day with a bid to cover of 2.35x, weaker than the last 5-Yr auction.

- Key last night was 3Q GDP which topped expectations at 4.3% annualized, the fastest pace in two years with resilient consumer and business spending. Exports jumped 8.8%, while imports decreased by 4.7%, providing a significant 1.59 percentage point boost to the headline GDP. Government spending recovered to a 2.2% growth rate, supported by increased national defense expenditures.

- Treasury Secretary Bessent covered multiple topics of interest on the future of the Federal Reserve in a recording of the "All-In Podcast" out Monday. The first point of interest was a hint that the White House would select a non-current Fed official as its next Fed Chair. Bessent, who is leading the search on behalf of the White House, said that Fed Gov Miran will be "going back to CEA [White House Council of Economic Advisers], probably in February or March".

- Projected rate cut pricing vs. early US morning levels (*): Jan'26 at -3.3bp (-4.4bp), Mar'26 at -11.3bp (-14.8bp), Apr'26 at -17.3bp (-21.9bp), Jun'26 at -30bp (-34.8bp).

- Markets close early (1315ET) Wednesday for Christmas eve, re-open for electronic trade Thursday evening for Friday:

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

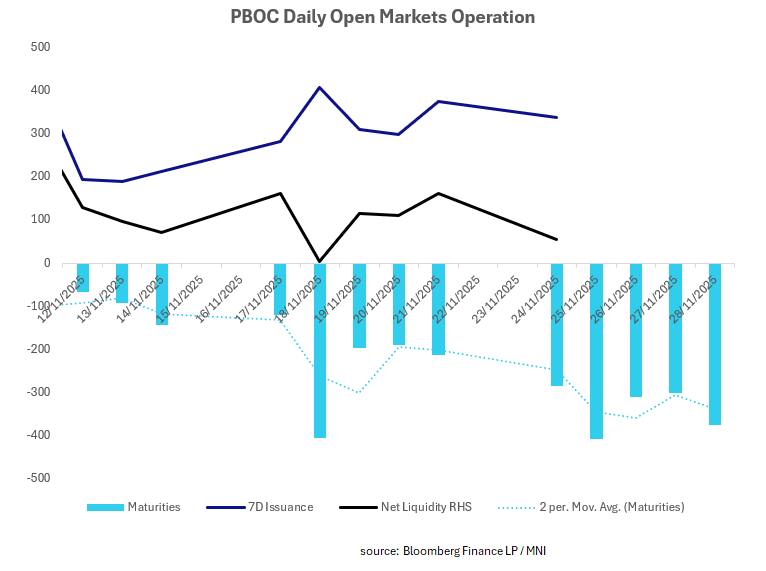

CHINA: Central Bank Injects CNY55.7bn via OMO

The CFETS Pledged Repo Deposit Institutions 7 Day Weighted Average declined throughout the week last week as the PBOC injected over CNY 550bn of liquidity via the daily OMO. With sizeable maturities ahead this week, and market sentiment finely balanced, markets will watch closely for liquidity movements as a useful catalyst for the broader market outlook.

- The PBOC issued CNY338.7bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY283bn.

- Net liquidity injection CNY55.7bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.40%, from prior close of 1.44%.

- The China overnight interbank repo rate is at 1.30%, from the prior close of 1.30%.

- The China 7-day interbank repo rate is at 1.40%, from the prior close of 1.45%.

CNH: USD/CNY Fixing Lower But Above Recent Troughs, Fixing Error Steady

The USD/CNY fix moved lower, back to 7.0847, but this is above recent lows (7.0816). The fixing error was little changed at -289pips, versus -315pips on Friday. The fixing outcome shouldn't change broader USD/CNH trends, where the bias remains to fade upticks. Downside focus will rest on a renewed test under 7.1000, but we are little changed post today's fixing (last around 7.1075, up a touch on end Friday levels). Broader USD trends are a little firmer, with the BBDXY up close to 0.10%.

MNI: CHINA PBOC CONDUCTS CNY338.7 BLN VIA 7-DAY REVERSE REPO MON

- CHINA PBOC CONDUCTS CNY338.7 BLN VIA 7-DAY REVERSE REPO MON