LNG: Darwin LNG Plant to Restart in Next Few Months

Jul-17 13:22

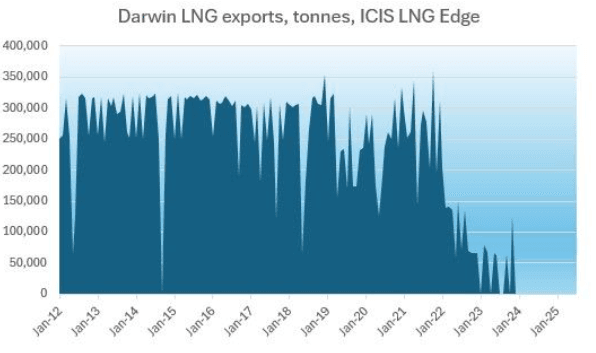

Australia’s Darwin LNG plant is restarting in the next few months, according to ICIS analyst Alex Froley.

- Darwin, in northwest Australia, used to export up to 300k tonnes per month but output started to decline sharply in 2022 as feedgas declined, with last loading in November 2023.

- Production company Santos has been investing in the Barossa project of the northwest coast of Australia as a new source of feedgas for Darwin LNG production.

- According to the company’s latest update, the project should be starting up in the third quarter of 2025.

Source: ICIS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Post-IP/Cap-U React

Jun-17 13:21

- Treasuries gain slightly after latest round of data: slightly lower Industrial Production w/ prior up-revised, Capacity Utilization and Mfg Production in-line.

- Tsy Sep'25 10Y futures trades +6 at 110-21.5 vs. 111-00 high, below key resistance and its recent high of 111-14+, a Fibonacci retracement and the Jun 5 high. Clearance of this hurdle would be bullish and highlight a stronger reversal. This would open 111-30, a Fibonacci retracement.

- Curves mixed, 2s10s -0.914 at 46.645, 5s30s +.065 at 92.111. 10Y yield at 4.4185% vs. 4.3770% low.

- Cross asset: Stocks remain weaker (SPX eminis -28.75 at 6061.0), Gold mildly higher at 3394.00, Bbg US$ index little changed at 1202.70 +0.11.

OAT: Natixis Don’t Expect Much Net Movement In OAT/Bund Spread Come Year-End

Jun-17 13:18

Natixis expect “some volatility (though less than last year) in the OAT curve by Q325, which should maintain or even strengthen the underperformance of OATs versus EGB peers”.

- Although they caution that “since H125, there have been several positive factors for the Eurozone, such as the German fiscal package and the gradual shift of non-residents' funds from the U.S. to the euro. All these factors could mitigate the risk of spreads widening”.

- They note that “regarding current idiosyncratic risk, the market needs further confidence that the French debt-to-GDP ratio will be reduced in the medium term. It will certainly take two to three years to remove the current political uncertainty premium in the spread”.

- They expect “the 10-Year OAT/Bund spread to narrow to 70bp by the end of the year, but budget discussions in autumn pose a risk of widening toward 75-80bp”.

- Spread last trades at ~71bp.

MNI: US MAY INDUSTRIAL PROD -0.2%; CAP UTIL 77.4%

Jun-17 13:15

- MNI: US MAY INDUSTRIAL PROD -0.2%; CAP UTIL 77.4%

- US APR IP REV TO +0.1%; CAP UTIL REV 77.7%

- US MAY MFG OUTPUT +0.1%