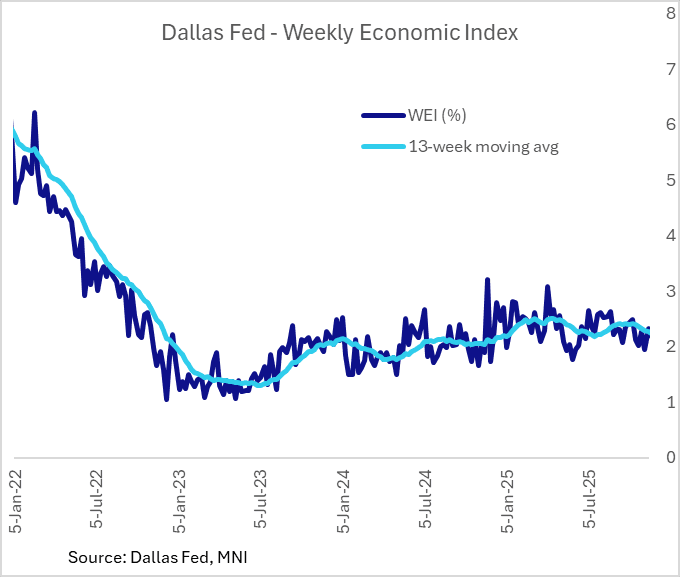

US DATA: Dallas Fed Weekly Index Ends Year Tracking Solid Q4 GDP Growth

The Dallas Fed's Weekly Economic Index concluded 2026 on a bright note, with the 4-quarter-scaled GDP growth rate ticking up in the Dec 27 week to 2.23% Y/Y from 2.21% prior.

- This should be caveated slightly by the fact that railroad traffic, electricity output, and fuel sales were not released for the latest week due to holidays, but it kept the 13-week (ie quarterly) moving average rate at 2.24% for a 6th consecutive week between 2.24-2.25%.

- The WEI was consistent with real GDP growth of 4+% Q/Q SAAR in Q3, which was closer to the mark than most (the official reading was 4.3%).

- Its final reading of Q4 means it tracked the equivalent of 2.5-3.0% Q/Q SAAR growth for the quarter, a little below the Atlanta Fed GDPNow estimate of 3.0%. We get the next Atlanta Fed reading on Monday after the ISM Manufacturing release for December.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

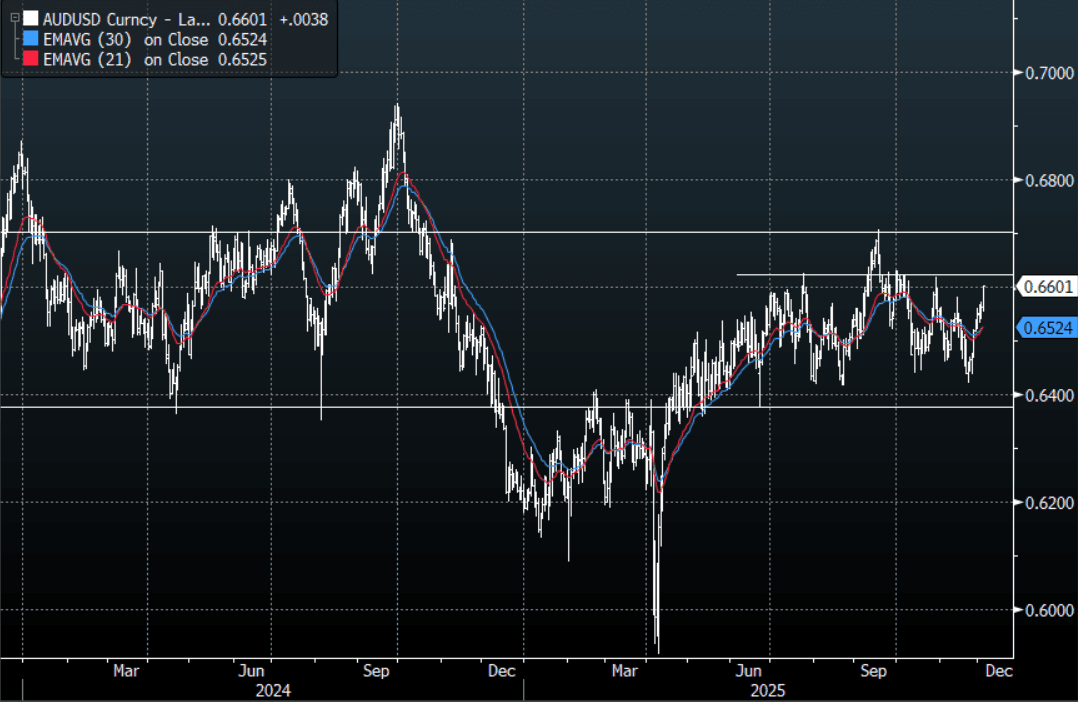

AUD: AUD/USD - Turns Focus To 0.6630, Looking To Build Momentum

The AUD/USD had a range overnight of 0.6574-0.6602, Asia is trading around 0.6600. The AUD continues to grind higher with dips shallow and supported, risk has managed to turn the poor start to the week around as the market eyes further potential U.S. rate cuts. The AUD price action was very constructive and indicative of a market with solid buying interest as it pushed through the 0.6580 pivot area. In the Asian session, I suspect dips back toward the 0.6560-0.6580 area could now be supported. The AUD is now looking to build some momentum to once again test the top end of its recent range, first target 0.6630 and then 0.6700.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6475(AUD357m), 0.6490(AUD710m). Upcoming Close Strikes : 0.6475(AUD814m Dec 8 ), 0.6500(AUD1.11b Dec 5), 0.6635(AUD651m Dec 9) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 41 Points

- Data/Event: October Trade Balance is due today and forecast to show a widening of the trade surplus to $4.5bn from $3.94bn.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

USDCAD TECHS: Has Cleared Short-Term Trendline Resistance

- RES 4: 0.6660 High Sep 18

- RES 3: 0.6640 76.4% retracement of the Sep 17 - Nov 21 bear leg

- RES 2: 0.6618 High Oct 29 and a key near-term resistance

- RES 1: 0.6600/6598 High Dec 03 / 61.8% retracement of the Sep 17 - Nov 21 bear leg

- PRICE: 0.6596 @ 16:44 GMT Dec 3

- SUP 1: 0.6517 20-day EMA

- SUP 2: 0.6466/21 Low Nov 26 / 21

- SUP 3: 0.6415 Low Aug 21 / 22 and a bear trigger

- SUP 4: 0.6404 38.2% retracement of the Apr 9 - Sep 17 bull cycle

AUDUSD continues to appreciate and price action remains above the 20- and 50-day EMAs. This week’s gains have resulted in a breach of a short-term trendline resistance at 0.6544, drawn from the Sep 17 high. The break strengthens a bull theme and highlights a stronger reversal, testing 0.6598 next, a Fibonacci retracement. First support is at 0.6512, the 20-day EMA. A move below this average would signal a possible reversal.

US TSYS: Tsys Grind Off Midmorning Lows, Mixed Data Ahead Thursday Weekly Claims

- Treasuries look to finish moderately firmer Wednesday - off early morning highs following a flurry of economic data.

- TYH6 currently +7.5 at 113-04 vs. 113-07 high, initial technical resistance at 113-11/22+ High Dec 1 / High Nov 25.

- The ISM services index was stronger than expected in November as it inched higher to 52.6 (cons 52.0) after 52.4 in October, marking its highest since February. The S&P Global US services PMI continues to offer a more optimistic assessment of current activity despite being revised down in its final November release to 54.1.

- ADP employment growth “surprised” lower at -32k (Bloomberg cons 10k) in November whilst the October increase was revised up from 42k to 47k.

- The S&P Global US services PMI was revised lower in the final November release 54.1 (flash & cons 55.0) in Nov final after 54.8 in Oct, dipping to its lowest since June rather than confirming what had been its highest since July.

- Stocks continue to plow higher Wednesday, recovering from early session lows after Microsoft denied a write-up from "The Information" they had lowered "AI software sales quotas". Pretty specific, nevertheless, while market concerns over stretched AI-tied valuations are on full display.

- Charles Gasparino at Fox Business reports on X that there is a 'last-ditch' effort by Wall Street and corporate America insiders to caution President Donald Trump against nominating National Economic Council Director Kevin Hassett as Federal Reserve Chair.

- Look Ahead Thursday Data Calendar: Challenger Job Cuts, Weekly Claims, Revelio & Regional Fed Data.