US DATA: Dallas Fed Weekly Activity Index Suggests Solid Pace Of Q3 Growth

Sep-04 17:33

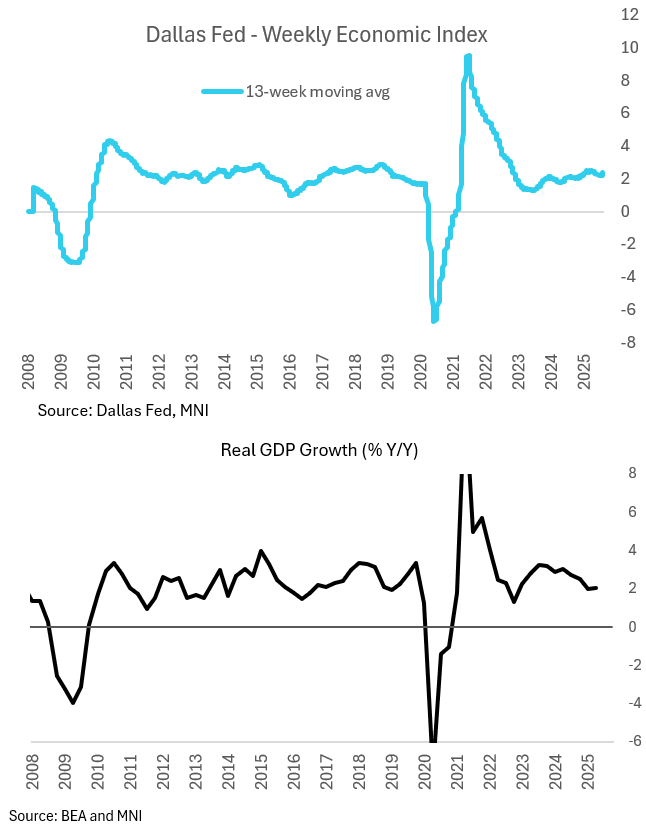

The Dallas Fed's Weekly Economic Index (WEI) continues to portray accelerating strength in economic growth vs a summer nadir.

- The latest reading for Aug 30 is for 2.52% 4-quarter real GDP growth.

- That is a slight pullback from 2.61% in the prior week but brings the 13-week (ie quarterly) reading up to 2.38% from 2.32%, for the 6th consecutive weekly acceleration for the fastest rate since mid-May. That compares to 2.07% in Q2.

- If this quarterly pace seen through the first two months of Q3 holds, it would suggest upside risks to the Atlanta Fed's GDPNow estimate for Q3 (of 3.0% Q/Q SAAR - which would represent "just" 2.0% Y/Y growth as represented by the WEI 13-week average), closer to the 3.3% Q/Q SAAR seen in Q2.

- While initial jobless claims data ticked higher in the latest week, potentially accounting for the retracement in the one-week measure, other components including Redbook retail sales remained robust in the latest week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBPUSD TECHS: Maintains A Softer Tone

Aug-05 17:30

- RES 4: 1.3681 High Jul 4

- RES 3: 1.3620 High Jul 10

- RES 2: 1.3448/1.3589 50-day EMA / High Jul 24

- RES 1: 1.3365 Low Jul 16

- PRICE: 1.3304 @ 16:47 BST Aug 5

- SUP 1: 1.3144 38.2% retracement of the Jan 13 - Jul 1 bull cycle

- SUP 2: 1.3041 Low Apr 14

- SUP 3: 1.3000 Round number support

- SUP 4: 1.2945 50.0% retracement of the Jan 13 - Jul 1 bull cycle

A bearish theme in GBPUSD remains intact for now - despite Friday’s rally. Last week’s sell-off resulted in a breach of the bear trigger at 1.3365, the Jul 16 low. The break confirms a resumption of the downleg that started Jul 1 and highlights a clear breach of the trendline drawn from the Jan 13 low. Sights are on 1.3144, a Fibonacci retracement, and 1.3041, the Apr 14 low. Firm resistance is 1.3448, the 50-day EMA. A break of this average is required to signal a reversal.

SOFR OPTIONS: Large Dec'25 SOFR Put Condor Spread & Midcurve Call Spread

Aug-05 17:24

- +20,000 SFRZ5 96.25/96.37/96.50/96.62 put condors vs. 95.75/95.87/96.00/96.12 put condor, .25 net

- -8,000 0QZ5 97.25/97.50 call spds, 5.62 ref 96.95

US TSYS/SUPPLY: Review 3Y Note Auction: Another Small Tail

Aug-05 17:03

- Treasury futures remain weaker, little react after $58B 3Y note auction (91282CNU1) tails yet again: drawing 3.669% high yield vs. 3.662% WI; 2.53x bid-to-cover vs. 2.51x prior.

- Peripheral stats see indirect take-up slips to 53.99% vs. 54.11% prior; direct bidder take-up 28.13% from 29.38% prior; primary dealer take-up rises to 17.88% vs. 16.51% prior.

- The next 3Y auction is tentatively scheduled for September 9.