RENEWABLES: CWE Morning Wind Forecast

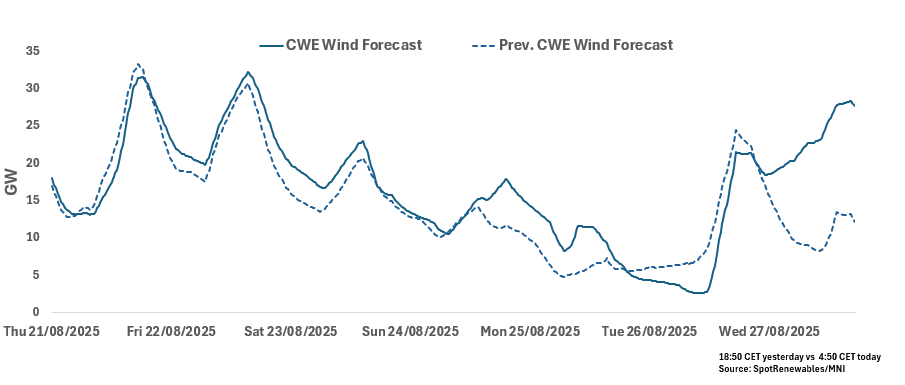

See the latest CWE wind forecast for base-load hours from this morning for the next seven days. CWE wind output will peak on 22 August at a 23% load factor before being on a general downward trend over 23-26 August.

CWE Wind for 21-27 August

- 21 August: 20.26GW

- 22 August: 25.04GW

- 23 August: 18.85GW

- 24 August: 13.69GW

- 25 August: 11.18GW

- 26 August: 6.36GW

27 August: 22.48GW

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BRENT TECHS: (U5) Still Looking For Weakness

- RES 4: $85.00 - Round number resistance

- RES 3: $81.99 - 2.764 proj of the Apr 9 - 23 - May 5 price swing

- RES 2: $80.72 - 2.618 proj of the Apr 9 - 23 - May 5 price swing

- RES 1: $72.66/79.40 - 50.0% of the Jun 23-30 range / High Jun 23

- PRICE: $69.51 @ 07:09 BST Jul 21

- SUP 1: $65.92 - Low Jun 30

- SUP 2: $61.39 - Low May 30

- SUP 3: $58.00 - Low May 5

- SUP 4: $57.70 - Low Apr 9 and a key support

A bearish theme in Brent futures remains present and this month's recovery is considered corrective. The sell-off on Jun 23 continues to highlight a bearish threat. Recent weakness has resulted in a print below the 50-day EMA and note too that $66.17, 61.8% of the May 5 - Jun 23 bull leg, has been pierced. A resumption of the downtrend would expose $61.39, the May 30 low. Initial resistance to watch is $72.66, a Fibonacci retracement point.

EGBS: Early Extension Higher Ahead of Busier Weekly Regional Calendar

Bund futures have extended higher over the last 20 minutes, after trading in a contained 13 tick range overnight with volumes limited by a public holiday in Japan. Now +52 ticks at 130.07, Bunds have pierced resistance at the 20-day EMA (129.92). However, a clear breach of the 50-day EMA at 130.21 is required to highlight a possible reversal of the current bearish theme. Initial support remains the July 14 low at 129.08.

- The early rally also sees OAT futures up 53 ticks and BTPs up 58 ticks from Friday’s settlement levels.

- Progress on an EU-US trade deal remains limited. Bloomberg reported that EU officials are formulating a retaliation plan for a no-deal scenario. This comes after the FT reported on Friday that President Trump was pushing for a minimum tariff of 15-20% on EU goods.

- No EGB supply scheduled today, with Germany set to come to the market tomorrow and Wednesday, and Italy to sell bonds on Thursday.

- A group of German companies and investors (the “Made for Germany” initiative) says it plans E631bln in investments in the country by 2028.

- This week’s regional calendar includes the ECB’s Q2 BLS, July flash PMIs and ECB decision. Our full ECB preview will be released later this week.

- Japan’s ruling coalition lost its majority in the Upper House following yesterday’s election (broadly in line with expectations), but PM Ishiba has said he will stay in office for now. The JGB market has been closed today, muddying the market’s interpretation of the results.

- Cash Treasuries were also closed overnight. Yields have opened up to 1.5bp lower across the curve, lightly bull flattening (see above for more).

US TSYS: A Little Firmer

Tsys look to EGBs for cues, after tight ranges were seen in futures during Asia-Pac hours. No clear driver for the rally at this stage.

- Perhaps some wider focus on Japanese PM Ishiba’s comments re: staying in power, despite losing control of the Upper House over the weekend.

- TY futures to fresh session highs.

- Cash Tsy yields are little changed to 1bp lower, curve flatter, after being closed in Asia hours, owing to a Japanese holiday.

- Some Asia focus fell on a report from the China Daily, with comments noting that it is a 'strategic necessity' to scale back on holdings of U.S. Treasuries, given the declining confidence in the dollar as the reserve global currency.