RENEWABLES: CWE Morning Wind Forecast

Mar-13 07:17

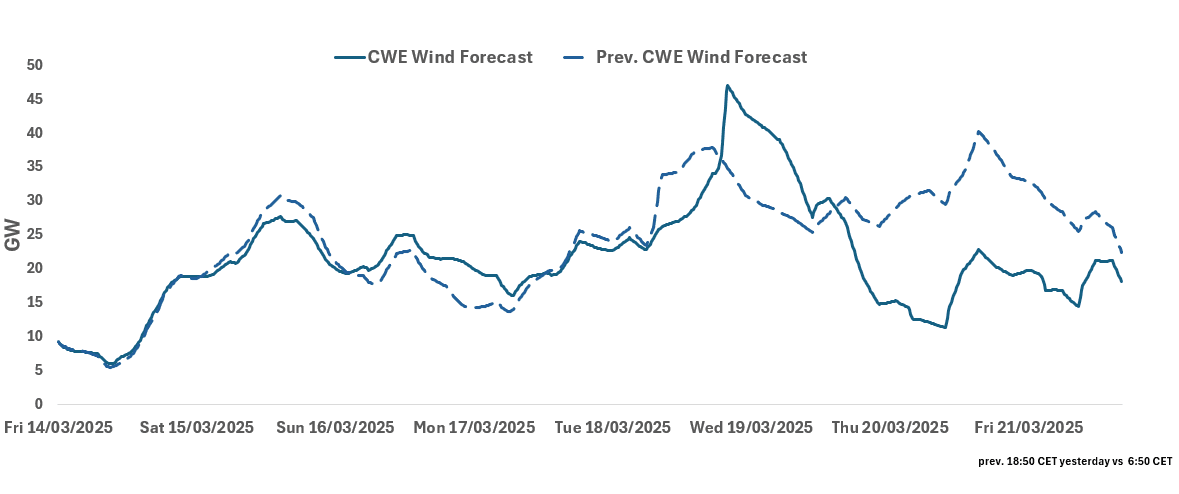

See the latest CWE Wind forecast for base-load hours from this morning for the next seven days. CWE wind is forecast to reach a weekday low on 20 March (Thur) at a 16% load factor and will rebound slightly the next day to an 18% load factor.

CWE Wind for 14-21 March

- 14 March: 10.68GW

- 15 March: 23.35GW

- 16 March: 21.71GW

- 17 March: 19.70GW

- 18 March: 26.50GW

- 19 March: 35.48GW

- 20 March: 16.14GW

21 March: 18.79GW

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUNDS: Heavy suppply and Fed Powell are in focus Today

Feb-11 07:17

- There's very little change for Bund, although the overnight session sees a slightly wider range, volumes on both sides of the Atlantic are on the low side.

- Bund and Tnotes are offered, after Trump ordered a 25% Tariff on all Steel and Aluminium Imports, but the German contract remains within the Initial support of 132.72 and resistance at 133.86.

- For the US 10yr, TYH5 is testing trendline right here at 109.03, although most desks will look for immediate support at 109.01, the fast market printed low, post NFP.

- This is a lighter Week on the Data front, with the US CPI (Wednesday) the key release, and for the UK, GDP (Thursday).

- There's no notable Data due for today.

- BoE Mann gave an Interview with the FT Yesterday, so today could be a lesser event, attention will be on Powell who testifies at the Senate.

- SUPPLY: Early focus will be on supply in Europe and later in the US, Netherlands €2bn 2047 (equates to 30.3k Bund) should weigh, Germany €5bn Bobl (equates to ~47.5k Bobl) will weigh. US Sells $58bn of 3yr Notes.

- SYNDICATION: EU 2031 Tap/2050 Green, Italy 2040, UK 2035.

- SPEAKERS: BoE Mann, Bailey, Fed Powell, Hammack, Williams, Bowman, ECB Schnabel.

MNI: NORWAY Q4 MAINLAND GDP -0.4% Q/Q

Feb-11 07:07

- MNI: NORWAY Q4 MAINLAND GDP -0.4% Q/Q

NORWAY: Q4 Mainland GDP Much Weaker Than Expected

Feb-11 07:03

Mainland GDP at -0.4% Q/Q was quite a bit weaker than both consensus and the Norges Bank December MPR projections of 0.3% Q/Q. Further details to follow.

- NOSEK is around 10 pips below pre-release levels at typing.

- A 25bp Norges Bank cut in March has already been well-signalled, but the weak reading may have dovish implications for the rate path further out the curve.