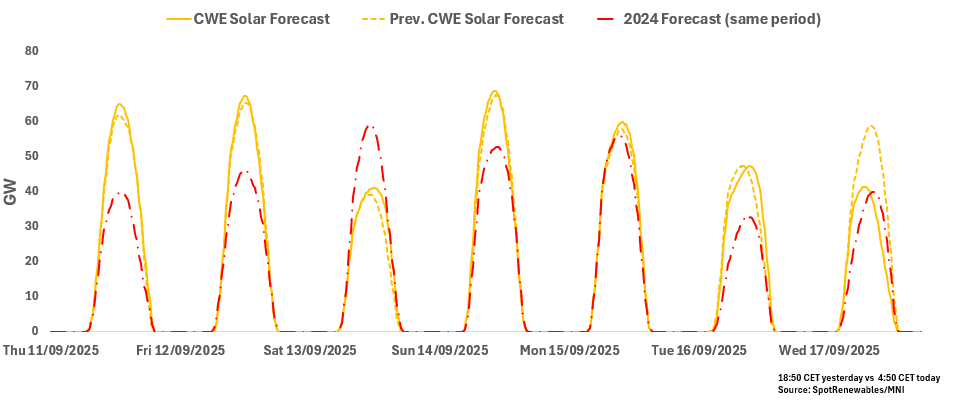

RENEWABLES: CWE Morning Solar Forecast

See the latest CWE solar forecast for peak-load hours starting this morning for the next seven days. CWE peak solar output will be on a general downward trend over 14-17 September, reaching as low as 15% load factor.

CWE Solar for 11-17 September

- 11 September: 40.14GW

- 12 September: 40.15GW

- 13 September: 26.82GW

- 14 September: 41.59GW

- 15 September: 37.87GW

- 16 September: 30.87GW

17 September: 23.94GW

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

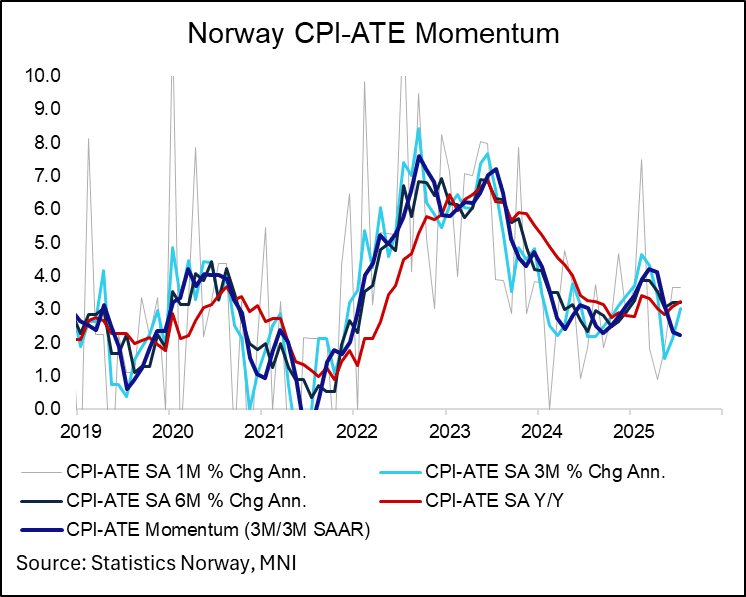

NORWAY: Inflation Momentum At 4 Year Low In July, But Will Likely Rebound

Norwegian inflation momentum, measured as a 3m/3m seasonally adjusted annualised rate (using Stats Norway data) eased to 2.22% in July (vs 2.33% prior), the lowest since December 2021. However, this measure will likely rebound in August barring a significant downward surprise, as February’s 0.61% M/M SA reading drops out of the calculation. Between March and May, SA CPI-ATE inflation averaged 0.13% M/M. Sequential inflation has been 0.30% M/M in both June and July.

- This is consistent with the view that while CPI-ATE inflation has been dragged around by volatile components during the Summer, underlying inflation remains a little persistent.

- While Norges Bank’s guidance that “the policy rate will be reduced further in the course of 2025” remains intact for Thursday’s decision, there is still a risk that the policy rate is only cut once more this year (and not twice, as several analysts are projecting).

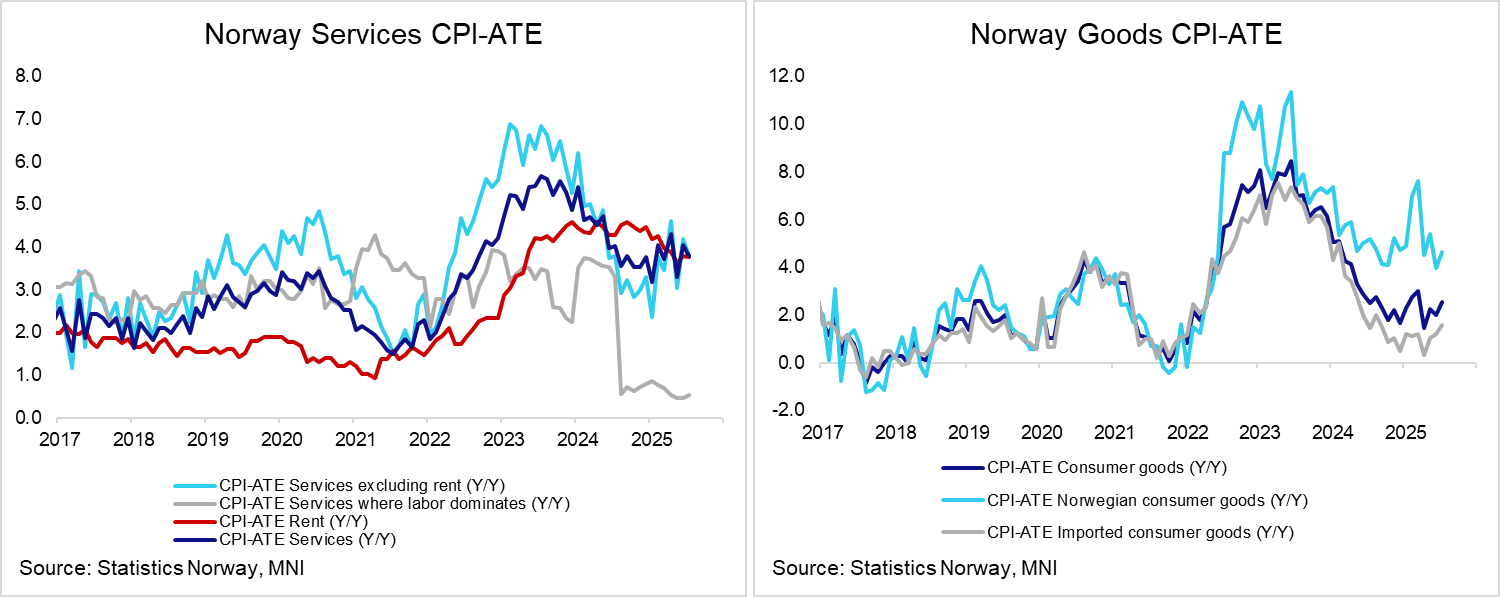

NORWAY: July CPI - Uptick In Food Alongside Persistent Underlying Services

- Food prices rose 4.53% M/M and 5.57% Y/Y (vs 4.35% prior) – above some of the estimates we had seen, and likely the main driver behind the higher-than-expected CPI-ATE reading (at least versus analyst projections).

- Rents remain a source of persistent inflationary pressure, rising 0.32% M/M for the second consecutive month with an annual rate of 3.77% Y/Y (vs 3.78% prior).

- Services excluding rents eased to 3.80% Y/Y (vs 4.19% prior).

- A pullback in airfares (-0.18% Y/Y vs 7.36% prior) and package holiday (1.24% Y/Y (vs 6.94% prior), which drove a large part of the upward inflation surprise in June, were offset by rises in accommodation (6.83% Y/Y (vs 3.66% prior) .

- Otherwise, there were some signs of persistence in the likes of insurance (14.31% Y/Y vs 13.24% prior), personal care (3.66% Y/Y vs 2.92% prior), restaurant services (3.35% Y/Y vs 3.37% prior) and recreation and culture (3.93% Y/Y vs 3.87% prior). Services inflation where labour dominates and excluding regulated prices ricked up to 4.26% Y/Y (vs 4.20% prior).

- Domestic goods inflation excluding agricultural products rose to 4.56% Y/Y (vs 4.18% prior). Alongside food, there were accelerations in a broad range of goods components (clothing, footwear, furniture, household textiles). Imported inflation ex agriculture was steady at 0.80% Y/Y. Including agricultural products, imported inflation is back on a gradually rising trend.

- Electricity prices fell 2.19% M/M, but this still saw the annual rate rise to 11.31% Y/Y (vs 8.34% prior), seemingly driving the headline inflation increase to 3.27% Y/Y (vs 2.99% prior).

RBA: MNI RBA Preview-Aug 2025: Cautious Augut Rate Cut

- Download Full Report Here

- The RBA’s Monetary Policy Board is unlikely to surprise economists and the market again in August when its decision is announced on Tuesday August 12. Bloomberg consensus is unanimous forecasting a 25bp rate cut to 3.60% given the further moderation in underlying inflation in Q2 towards the band mid-point, which should increase confidence that it is now sustainably within target, and signs that the labour market has reached a turning point.

- Thus, the “timing” this month is likely to be more suitable than last month possibly resulting in a 9-0 vote after July’s 6-3 split in favour of holding.

- With the economy broadly developing as the Board expected in May, there are unlikely to be material changes to the updated forecasts accompanying the August statement.

- The tone of the decision and Governor Bullock's press conference is likely to reiterate the bank's gradual and cautious approach to easing. We expect any further cuts to coincide with forecasting meetings.