OIL: Crude Watching & Waiting Middle East Situation

Oil is little changed today continuing to hold onto gains made since Friday as the situation in the Middle East remains tense and uncertain. Currently the main impact on oil from the conflict is on shipping but concerns are heightened that supply could be more severely impacted if Israel strikes Iran’s main export hubs or if Iran blocks the Strait of Hormuz. Israel and Iran continue to strike each other’s territory.

- WTI is down slightly to $73.48/bbl after falling to $72.63 earlier, while Brent is 0.2% lower at $76.52/bbl off the intraday low of $75.67. The USD is slightly higher.

- Goldman Sachs is assuming that the geopolitical risk premium on Brent is around $10/bbl, according to Bloomberg, but expects it to fall to $60 in Q4 assuming no supply issues.

- US President Trump said on Wednesday that he has approved a plan but is still hoping that Tehran will agree to abandon its nuclear programme. However, supreme leader Khamenei said they would “never surrender” in response to Trump’s demand for an unconditional surrender. The market is nervously waiting to see if the US will act and in what capacity.

- In a Bloomberg interview, the President of the API said that he doesn’t expect Iran to impact the Strait of Hormuz but given its situation the waterway should be monitored.

- Later the SNB and BoE announce decisions. The ECB’s Lagarde, de Guindos and Buch speak. April euro area construction prints. The US is closed for a holiday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUND TECHS: (M5) Bull Cycle

- RES 4: 132.56 High Feb 28 and a key resistance

- RES 3: 131.72/132.03 High May 7 / High Apr 7 and the bull trigger

- RES 2: 130.86 High May 9 Round number resistance

- RES 1: 130.67 Intraday high

- PRICE: 130.52 @ 05:37 BST May 20

- SUP 1: 129.72/13 Low May 19 / 15 and key short-term support

- SUP 2: 129.02 Low Apr 10

- SUP 3: 128.60 Low Apr 9 and a key support

- SUP 4: 128.19 Low Mar 27

Bund futures continue to trade above last week’s low print. The move higher undermines the recent bearish theme and suggests the move down between Apr 22 - May 15, has been a correction. An extension higher would strengthen the reversal and open 130.86 next, the May 9 high. Further out, scope would be seen for an extension towards 132.03, the Apr 7 high. Key short-term support has been defined at 129.13, the May 15 low.

AUSSIE BONDS: Rallies After Cut & Dovish Tilt By RBA

ACGBs (YM +7.0 & XM +7.5) are sharply stronger on the day and richening 4-6bps after the RBA Policy Decision.

- The RBA cut the cash rate, as expected, by 25bps to 3.85% and left a dovish first impression in terms of the statement, by trimming its inflation (trimmed mean) and growth forecasts slightly.

- Last para of RBA Statement: “The Board will be attentive to the data and the evolving assessment of risks to guide its decisions. In doing so, it will pay close attention to developments in the global economy and financial markets, trends in domestic demand, and the outlook for inflation and the labour market. The Board is focused on its mandate to deliver price stability and full employment and will do what it considers necessary to achieve that outcome."

- Cash ACGBs are 7bps richer with the AU-US 10-year yield differential at flat.

- The bills strip has extended its strengthening after the RBA decision, led by late whites, with pricing +4 to +8.

- RBA-dated OIS pricing is flat to 7bps softer across meetings after the decision. A 25bp rate cut today was given a 95% probability. A cumulative 81bps of easing is now priced by year-end (-75bps before the data).

- Tomorrow, the local calendar will see the Westpac Leading Index.

- The AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond tomorrow and A$800mn of the 2.75% 21 November 2028 bond on Friday.

FOREX: Asia FX Wrap - Risk Sees Some Reversion, The USD Holds Steady

The BBDXY has had a range of 1224.40 - 1226.87 in the Asia-Pac session, it is currently trading around 1225. China Prime Rates Lowered As Expected: The 1 and 5 year Loan Prime Rates were reduced in line with expectations. The move lower by 10bps for each sees the 1-year LPR to 3.00% and the 5-year LPR to 3.50%, the lowest they have been since inception. CATL’s huge listing on the Hong Kong exchange produced an early jump for the shares, which is lifting the Hang Seng Index as the trading debut will also encourage more IPOs to list in the city on attractive valuations.(BBG)

- EUR/USD - Asian range 1.1218 - 1.1251, Asia is currently trading 1.1245.The market is still expected to use dips as a buying opportunity with dips back towards 1.09/1.10 well supported.

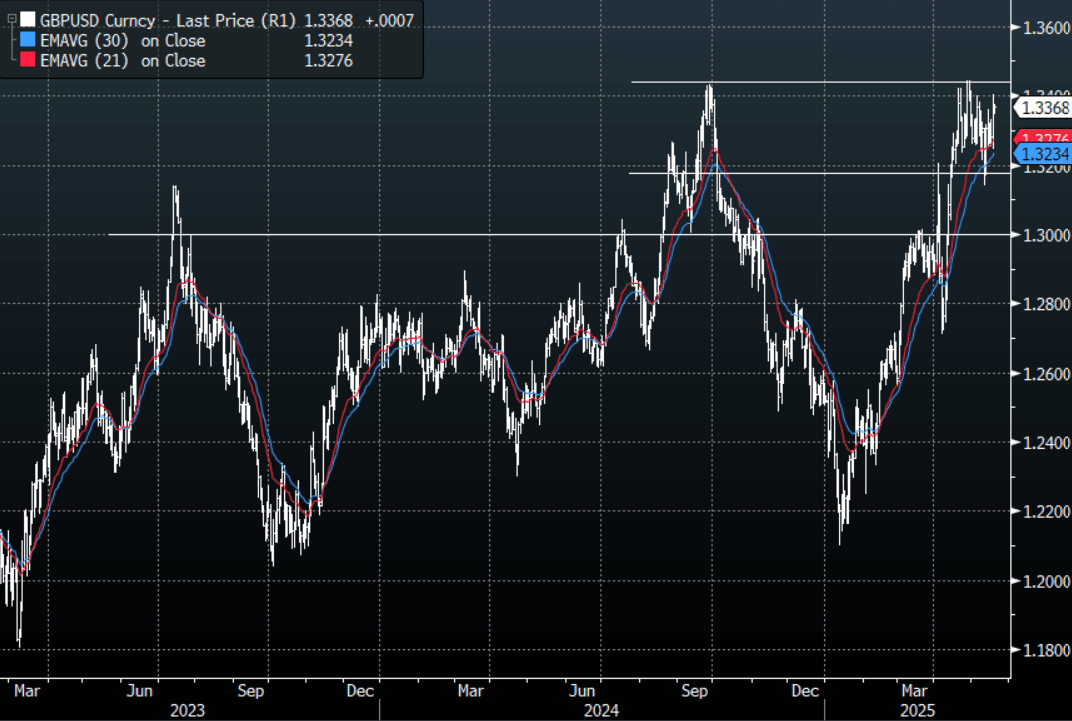

- GBP/USD - Asian range 1.3345 - 1.3376, Asia is currently dealing around 1.3370. Decent demand for GBP sub 1.3200 has seen it bounce back and it looks likely to test the upper bounds of its range above 1.3400. Like the EUR the market prefers to buy on dips.

- USD/CNH - Asian range 7.2128 - 7.2263, the USD/CNY fix printed 7.1931. Asia is currently dealing around 7.2230. Sellers should be found on a bounce back towards 7.24/25 again.

- Cross asset : SPX -0.3%, Gold $3215, US 10-Year 4.45%, BBDXY 1225, Crude oil $62.72

Data/Events : Ger PPI, EZ Current A/C, EZ Construction Output, EZ Consumer Confidence, Philly Fed nonmanufacturing survey

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg