COMMODITIES: Crude Rebounds, Precious Metals Extend Decline

* WTI crude has risen today, more than reversing yesterday's losses, as the market assesses height...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

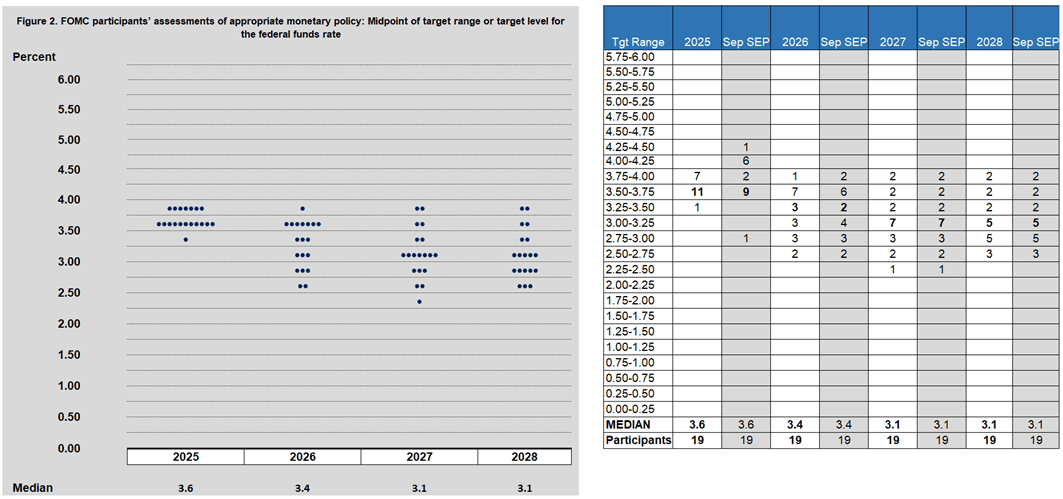

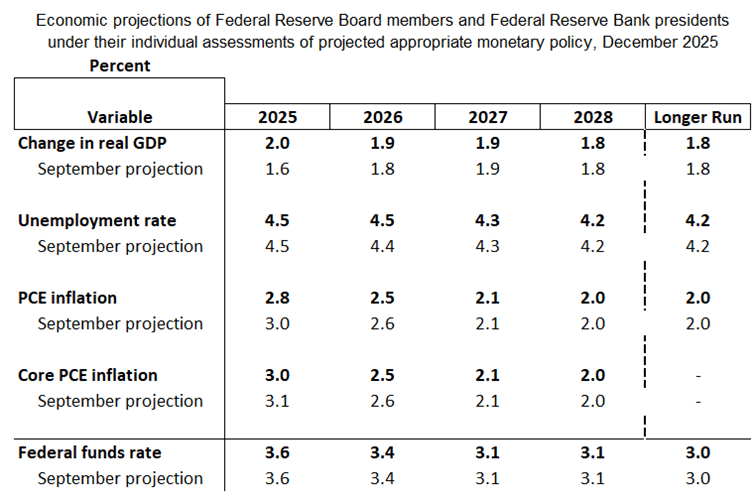

FED: SEP/Dot Plot: Slight Upgrade To GDP, Downshift To Inflation (2/2)

As for the new macroeconomic projections, there’s likely to be a slight upgrade to GDP forecasts with some downshifting of PCE inflation in 2025/2026.

- There is some risk that the unemployment rate forecast shifts up slightly for 2025 but anything above 4.5% would be a major surprise.

USDJPY TECHS: Support To Watch Lies At The 50-Day EMA

- RES 4: 158.87 High Jan 10 and a key resistance

- RES 3: 158.29 2.618 projection of the Sep 17 - 26 - Oct 1 price swing

- RES 2: 158.00 Round number resistance

- RES 1: 157.89 High Nov 20 and bull trigger

- PRICE: 156.87 @ 16:47 GMT Dec 9

- SUP 1: 154.35 Low Dec 5

- SUP 2: 153.58 50-day EMA

- SUP 3: 152.82 Low Nov 7

- SUP 4: 151.54 Low Oct 29

Recent weakness in USDJPY is considered corrective and the deeper retracement has allowed an overbought condition to unwind. Key short-term support to watch lies at the 50-day EMA at 153.58. A clear breach of the average would signal scope for a deeper retracement. Moving average studies remain in a bull-mode position, highlighting a dominant medium-term uptrend. A resumption of the uptrend would open 158.00.

FED: SEP/Dot Plot: Steady Course (1/2)

The lack of major data since the September projections round portends only limited changes to the macro and rate forecasts in the December edition out Wednesday.

- None of the rate dot medians are expected to change, with 2025 confirmed at 3.6% (though with an unusual amount of disagreement in the dot distribution for an end-year SEP in a form of "soft dissent" against the cut), 2026 at 3.4% (implying one 25bp cut), with 2027 at 3.1% (another 25bp cut).

- In short, we expect most of the attention to be on the rate distribution. For 2026, the September dots were closely poised between 3.4% and 3.1% (10 above 3.25% vs 9 below 3.25%). We don’t see much change here but if anything the risks to the median skew to the downside. For example, if one member who put their dot at 3.4% in September also saw rates ending 2025 at 3.9%, they might mark-to-market the rate view one notch lower.

- We’ll also be watching for any dots implying a 2026 hike (we would expect at least one seeing rates higher than 3.6%) with the solidity of a 2026 “hold” also in focus.

- The longer-run dot is broadly expected to remain at 3.0%. But once again with 10 at 3.00% or below and 9 above that level, it would only take 1 moving from 3.00% or below to above 3.00% to move the median higher, likely to 3.1%. That shift will happen at some point and it wouldn’t be a shock to see it come this week.