OIL: Crude Rallies As US-Venezuelan Tensions Rise

After falling earlier in the week on renewed excess supply worries, crude rose 1.2% on Wednesday boosted by the Fed cutting rates, which is supportive of energy demand, but also the US seizure of a tanker off the coast of Venezuela, with 2mn barrel capacity, which according to the US attorney general was carrying sanctioned crude from Venezuela and Iran. Thus geopolitics are impacting oil markets again but Thursday sees OPEC and IEA reports released, which could refocus it on fundamentals.

- The US has been taking action against Venezuela due to its drug shipments and Maduro’s autocratic regime. The appropriation of the tanker is likely to dissuade other shippers from carrying Venezuelan crude reducing global supply. China is the main buyer of Venezuelan and Iranian oil.

- Although shipments have risen through 2025, Venezuela was only the 17th largest exporter in 2023, according to the IEA, despite having the largest known reserves.

- Chevron said that its Venezuelan operations have been unaffected by the latest developments. President Trump has been pressuring the company to reduce its operations in the country and discussions continue.

- WTI rose 1.2% to $58.96/bbl but is still down 1.9% this week. It fell to $57.66 and then rallied to $59.05, below resistance at $61.84, but struggled to hold the break above $59. It is currently around $58.85. Short-term gains continue to be seen as corrective with a bearish threat present. The bear trigger is at $55.99, 20 October low.

- Brent is up 1.1% to $62.64 but 1.7% lower this week. It rose to $62.73 after an intraday low of $61.35. The benchmark remains in a downtrend with the bear trigger at $59.33. It failed to breach resistance at $65.25, 24 October high, on Wednesday.

- EIA reported a 1.81mn barrel US crude drawdown last week but products rose with gasoline up 6.4mn, highest since end December 2024, and distillate 2.5mn. Refining utilisation rose 0.4pp to 94.5%, 2.1pp above same time last year. It is usual for product inventories to be built up through December/January.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LNG: Cold Drives US Prices Up, Europe Down On High LNG Imports

The cold snap across the eastern US drove gas prices higher at the start of Monday reaching a peak of $4.509 during the European session it then fell to a low of $4.262 but finished up 1.4% to $4.375, around where it is Tuesday, and is now around 6% higher in November. Temperatures are now forecast also to be lower across most of the US mid-month increasing heating consumption, while demand for LNG exports is strong.

- US LNG exports reached around 18bcf/d on the weekend, a record (Bloomberg), but US output was also at a record. Europe has become a favoured destination for non-contracted shipments.

- BNEF data showed that US lower-48 gas demand rose 30.6% y/y on Monday to its highest since the start of March as the Polar Vortex impacted the east of the country. Production was up 12.1% y/y. Flows to LNG export facilities +5.3% w/w.

- European gas continued to trade in a narrow range as it waits for information on the outlook for the upcoming winter and changes to supply developments. They fell 0.6% to EUR 31.01 on Monday to be down slightly in November as LNG imports remain strong, especially from the US. They have been trending higher since mid-Q3. Prices reached EUR 31.44 early in the session before falling to EUR 30.765.

AUSSIE 10-YEAR TECHS: (Z5) Returns Lower

- RES 3: 95.982 - 76.4% retracement Sep’24 - Nov’24 downleg

- RES 2: 95.960 - High Apr 7 (cont.)

- RES 1: 95.900 - High Oct 17

- PRICE: 95.620 @ 15:43 GMT Nov 10

- SUP 1: 95.510 - Low Sep 3

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

Aussie 10-yr futures slipped lower last week on the back of hotter-than-expected inflation data. This returned prices lower despite nascent signs of a technical recovery as recently as late October. The sustainability of the pullback will be dependent on prices holding above key short-term support at 95.510, the Sep 3 low. Near-term resistance remains 95.780, the Sep 12 high. A clear break of this level signals scope for a continuation higher and opens 95.960, the 76.4% retracement level for the Sep’24 - Nov’24 downleg.

JGBS: Futures Stronger Overnight Despite Heavy US Tsys, 30Y Supply Due

In post-Tokyo trade, JGB futures closed stronger, +14 compared to settlement levels, despite US tsys finishing Monday's session with a modest bear-flattener, with yields 1-3bps higher.

- Optimism buoyed as the US shutdown appears to be nearer an end after eight Democrats broke formation with colleagues to reopen the government.

- MNI INTERVIEW: BOJ Dec Hike Needed To Support Yen - Sakurai. The Bank of Japan should raise its policy rate 25 basis points to 0.75% at the Dec 18-19 meeting, as delaying a move would undermine its independence and risk further yen depreciation amid pressure from U.S. funds, former board member Makoto Sakurai told MNI. Markets have priced in a 49.8% chance of a hike next month.

- Sakurai, who maintains close contact with BOJ officials since leaving the board in 2021, said Takaichi's dovishness also weighed on the bank's decisions. "The BOJ might have raised the rate in October if the prime minister wasn't Takaichi," he said, adding that concern over government reaction likely contributed to the bank's decision to stay on hold last month.

- Today, the local calendar will see Trade Balance and Bank Lending data alongside 30-year supply.

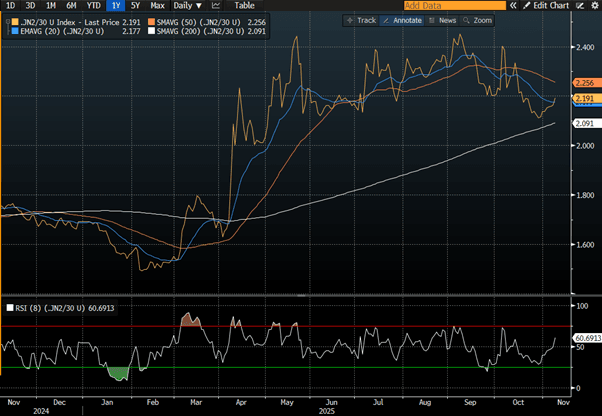

- The 2/30 curve remains within its well-established range ahead of today’s supply. (see chart)

Source: Bloomberg Finance LP