OIL: Crude Inventory Data & Monthly Reports Monitored As Surplus In Focus

Oil prices continued declining on Tuesday as excess supply is back in focus with the release of monthly reports this week. In line with this, weaker demand expectations drove diesel prices down a further 2.7% and a hawkish Fed may weigh on the outlook. US EIA data is out Wednesday and will be monitored for not only rising inventories but also softening product consumption.

- WTI fell 0.8% to $58.39/bbl to be slightly lower in December. It reached $59.17 before declining to $58.12. Moving average studies are in a bear-mode position with the bear trigger at $55.99. Initial resistance is at $61.84.

- Brent is down 0.6% to $62.09/bbl to be -0.5% this month. It rose to $62.78 and then fell to $61.83. The benchmark remains in a downtrend with the bear trigger at $59.93. Initial resistance is at $65.25, 24 October high.

- Bloomberg reported that US oil inventories fell 4.8mn barrels last week, according to those familiar with the API data. Product stocks were higher with gasoline stocks up 7.0mn and distillate 1.0mn.

- The EIA short-term energy outlook expects Brent to average $55/bbl in Q1 2026 and stay around there through the year. It said that OPEC’s policy to stabilise production and China’s ongoing inventory build should limit the downside. Some producers have said that lower prices would discourage investment in the US. The IEA and OPEC reports are out Thursday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Little Changed To Start The Week, RBNZ Inf Exp Tomorrow

NZGBs are unchanged after US tsys finished the NY session modestly cheaper on Friday as early risk-off sentiment moderated.

- On Friday, Republicans rejected Senate Democrats on ACA subsidy as the US Govt shutdown looks to enter it's sixth week next week. However, Bloomberg is reporting, "Senate Republican leader John Thune said a deal is "coming together" as he planned a Sunday vote to end the US government shutdown."

- MNI Tech: A short-term bearish threat in 10-year tsy futures (TYZ5) remains intact. Sights are on a reversal trigger at 112-06, the Sep 25 low, and the 100-DMA, at 112-07. Clearance of these price points would expose a trendline support at 112-00 - the trendline is drawn from the May 22 low.

- Fed Vice Chair Jefferson (voter) on wanting to proceed slowly, being closer to a neutral level rather than talking on Powell’s “fog”. He does, though, note a meeting-by-meeting stance being especially prudent with a lack of official data.

- Swap rates are little changed.

- RBNZ dated OIS pricing is little changed across meetings. 28bps of easing is priced for November, with a cumulative 37bps by February 2026.

- Today, the local calendar will be empty. The next release of note will be the RBNZ's Inflation Expectations data tomorrow.

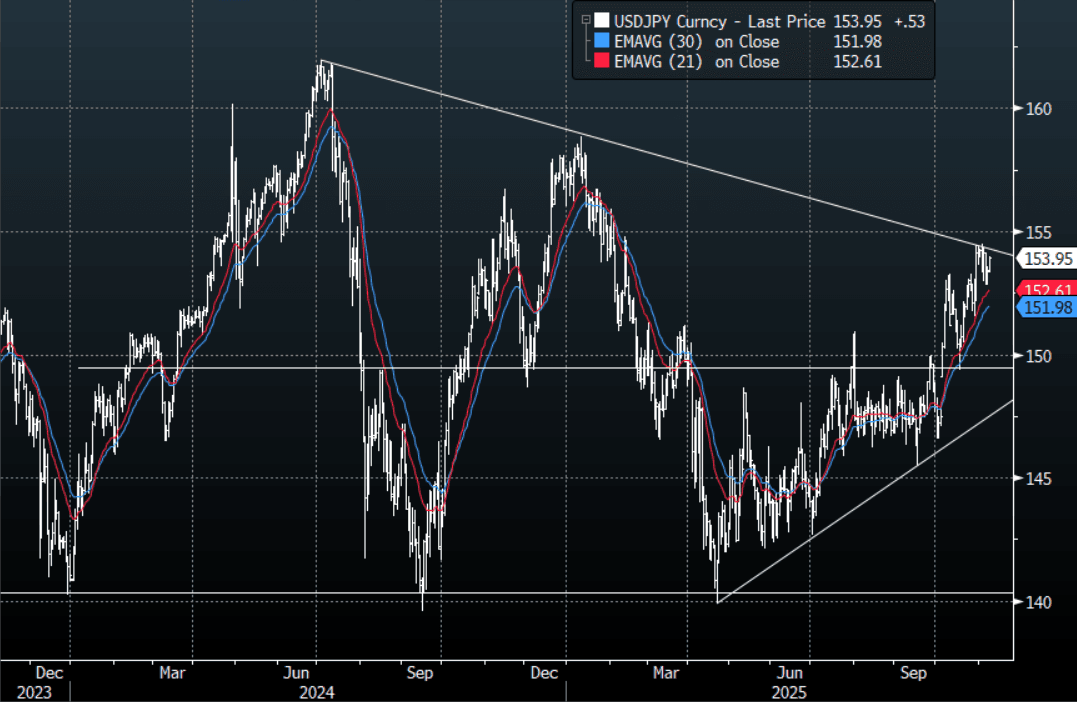

JPY: USD/JPY - Gaps Higher On Positive Shutdown Report

The Friday night range was 153.01 - 153.59, Asia is currently trading around 153.95, +0.35%. The pair has gapped higher on the Asian open as reports of a potential deal on the US shutdown make the rounds, reversing the short-term negative market sentiment on risk. USD/JPY found solid demand around the 153.00 area on Friday again, any confirmation of the shutdown ending would potentially see a knee-jerk higher in risk. In this scenario the focus would turn again to the resistance around the 154-155 area. A sustained break above here could potentially see the uptrend regain upward momentum as the focus would turn to the 160 area where I would start to become wary of intervention risks.

- Bloomberg reports, “ The LDP becomes more flexible in targeting budget surplus; CDP cites "fiscal discipline issues". On an NHK program on the 9th, LDP Policy Research Council Chairman Takayuki Kobayashi said, "Rather than being fixated on a single-year balance, we need to think about it a little more flexibly" regarding the target of achieving a primary balance surplus, an indicator of fiscal soundness.”

- Nikkei says, "Japan seeks to boost investment with upcoming economic stimulus. Japan's economic stimulus package is set to include tax cuts to spur investment focused around 17 key industries, including AI and semiconductors, and multi-year budget allocations to make policy more predictable, the Nikkei newspaper reported.”

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : none - BBG.

- Data/Event : Leading Index

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSTRALIA: Unemployment Rate Forecast To Dip, Released Thursday

The focus of the week will be Thursday’s October jobs data. After the unemployment rate rose 0.2pp to 4.5% in September, the release will be monitored to see if there is some stabilisation as the data can be volatile on a monthly basis. Bloomberg consensus expects it to fall 0.1pp to 4.4% with new jobs up 20k and the participation rate stable at 67%. RBA Governor Bullock has advised to look at the data on a 3-month average basis.

- On Monday, RBA Deputy Governor Hauser speaks at 1030 AEDT on the Outlook for the Australian Economy. It can be watched here.

- Other RBA speakers this week include a fireside chat with Assistant Governor (Financial System) Jones on Wednesday at 0915 AEDT and with Assistant Governor (Business Services) McPhee on Friday at 0910 AEDT.

- Key surveys are also released this week with November Westpac consumer confidence on Tuesday, which may be down again following the RBA’s clear hold on 4 November and the higher Q3 CPI print.

- The October NAB business survey also prints on Tuesday. It has been gradually recovering with the price/cost components fairly stable. The employment component is likely to be monitored after the Q3 survey showed an increase in employment intentions.

- Q3 home lending is published on Wednesday and the value of loans is forecast to rise 2.6% q/q after 2.0% in Q2.

- November Melbourne Institute consumer inflation expectations are out on Thursday. The series has been running at a higher rate since mid-year at 4.6% compared with 4.1% for the first 5 months of 2025. October was 4.8%.