OIL: Crude Higher As Ongoing Talks Seem No Closer To A Deal

Oil prices rose on Wednesday as the US-Ukraine-Russia continue talking but a deal remains elusive. Given negotiations have stalled previously, there remains a very real chance they will again. The prospect of an easing of sanctions and increased Russian exports has weighed on crude. It trended lower after US EIA data showing crude and product stock builds.

- WTI rose 0.8% to $59.10/bbl to be up 1% this week but has been trading in narrow range. It reached $59.64 before moderating. Gains are still considered corrective with the bear trigger at $55.99. Initial resistance is at $65.25.

- Brent is up 0.6% to $62.80/bbl after a high of $63.37. Initial resistance is at $65.25 but a bear theme persists with the trigger at $59.93.

- Russia said that US envoy’s Witkoff’s talks with President Putin were “constructive”, while President Trump said the meeting was “reasonably good” but can’t tell what the results will be. Ukrainian negotiators are due to meet US officials in Florida on Thursday, according to AP. On Wednesday, Secretary of State Rubio said talks are currently at the point of trying to work out what Ukraine can accept.

- The EIA reported a US crude inventory build of 0.57mn barrels last week with gasoline up 4.52mn and distillate 2.1mn. A 1.8pp rise in refining utilisation to 94.1% is contributing to the product increases, which is not unusual for this time of year. End November 2024 saw a 2.8pp rise in to 93.3% with product stocks rising through H2 November and through December.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

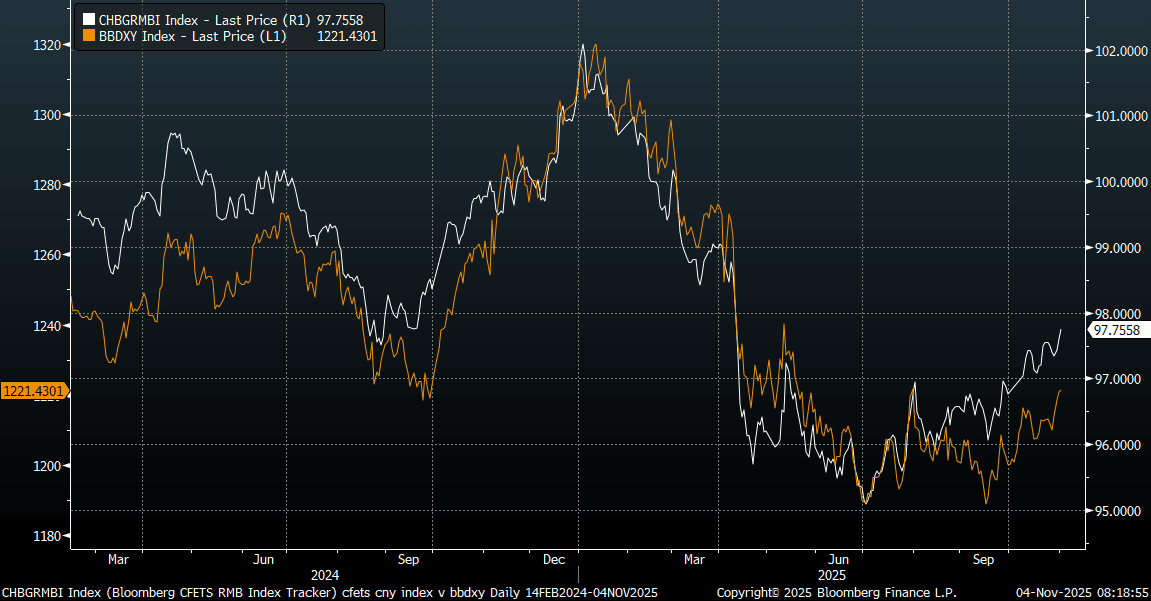

CNH: USD/CNH Recovery Continues, But CNY Basket Tracking USD Index Higher

USD/CNH tracks near 7.1265/70 in early Tuesday dealings, just short of intra session highs from Monday (7.1291). The pair remains in a modest uptrend, with eyes on a 50-day EMA resistance test (around 7.1335/40), as broader USD sentiment has stabilized/strengthened. Beyond that we have the 7.1500 region, which marked highs from Oct. CNH losses were broadly in line with USD index gains from Monday. Spot USD/CNY ended at 7.1213, while the CNY CFETS basket tracker continued to track higher, last 97.76, which is fresh highs back to April of this year.

- The positive correlation with the CFETS basket tracked and broader USD levels continues (see the chart below). Further USD upside should see higher basket levels all else equal, as CNY maintains a low beta to such trends (although higher USD/CNH levels remain a risk).

- For the USD the DXY rally stalled just ahead of the psychological 100 mark, and the August highs at 100.25. Additionally, weaker-than-expected ISM manufacturing and prices paid data have provided a moderate dollar headwind, especially against a backdrop of relatively few US data releases in recent weeks.

- CNH/JPY sits near 21.64, just off recent highs above 21.70, while EUR/CNH is eyeing a test under 8.2000 (last around 8.2100).

- On the data front, tomorrow delivers the RatingDog Services PMI, with a softer tone to manufacturing outcomes in Oct. The Citi China activity surprise index is in negative territory but up from recent lows.

Fig 1: CNY CFETS Basket Tracker & BBDXY Index

Source: Bloomberg Finance L.P./MNI

US TSYS: Corporate Issuance Drives Yields Higher, TSY Funding Estimates Lower

Despite the uptick in issuance, bond futures were relatively unchanged with the US 10-Yr future (TYZ5) unchanged. As cash was weak this could be indicative of funding for the new issues coming from UST sales rather than cash, a sign that funds have reduced cash of late. TYZ5 finished where it began at 112-21+ at the mid-point between the 50-day EMA of 112-26+ and the 100-day EMA of 112-11+. TYZ5 has opened at 112-21+ with limited price action early.

A uniform move higher in yields across the curve overnight on a generally weak night for bonds as corporate issuance ramped up.

- The 2-Yr was +3.3bps higher at 3.609%.

- The 5-Yr was +3.3bps higher at 3.722%

- The 10-Yr rose +3.1bps to 4.11%

- The 30-Yr is up +3.7bps to 4.69%

- Projected rate cut pricing gains slightly vs. late Friday levels (*): Dec'25 at -16.4bp (-15.6bp), Jan'26 at -24.6bp (-23.5bp), Mar'26 at -32.9bp (-32.1bp), Apr'26 at -39.1bp (-38.5bp).

- Data overnight was mixed with S&P Global US Mfg better than expected at 52.5, up from 52.2 prior whilst ISM Mfg declined to 48.7, from 49.1 with prices paid remaining high at +58 whilst new orders and employment in contraction.

- Treasury's latest Financing Estimates here as borrowing requirements were reduced to US$569bn from US$590bn and below MNI estimates with speculation that this week's funding announcement could see the current allocation to bill issuance of 21% to rise dramatically. The thinking being that this should keep longer dated yields down: https://home.treasury.gov/news/press-releases/sb0300

- November issuance kicked off with a bang with US$40.25bn of corporate debt issued. Govt issuance was focused on bills with a 13-week US$86bn and a 26-week US$77bn.

- Fed Gov Cook said in a speech Monday that she viewed the decision to cut rates in October "as appropriate, because I believe that the downside risks to employment are greater than the upside risks to inflation."

BONDS: NZGBS: Little Changed, Holding Yield Bounce, Q3 Jobs & Wages Tomorrow

NZGBs are unchanged despite a heavy close for US tsys, with yields ~3bps higher.

- US tsys extended early weakness after unexpectedly large corporate bond issuance announced ($40.5B with Alphabet making up $17.5B over 8 tranches) - only to gap back to pre-open level after lower-than-expected ISM Mfg & Prices paid data.

- The key event in NZ this week is the release of Q3 labour market and wages data tomorrow. Filled jobs for the quarter signal a stabilisation, but employment is likely to have remained weak, with consensus forecasting it to rise only 0.1% q/q to be still down 0.2% y/y. The unemployment rate is expected to rise 0.1pp to 5.3%, in line with the RBNZ's August projections. Soft labour demand is likely to weigh on private wage growth, which is forecast to rise around 0.4% q/q after 0.6%.

- Swap rates are little changed. The 2-year rate is holding its recent rise, bouncing off channel support, after reaching extreme overbought conditions. (see chart)

- RBNZ dated OIS pricing is little changed across meetings. 23bps of easing is priced for November, with a cumulative 30bps by February 2026.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 5.00% May-54 bond.

Bloomberg Finance LP