EU CREDIT SUPPLY: CREDIT SUPPLY: Deutsche Telekom FV

Nov-20 09:14

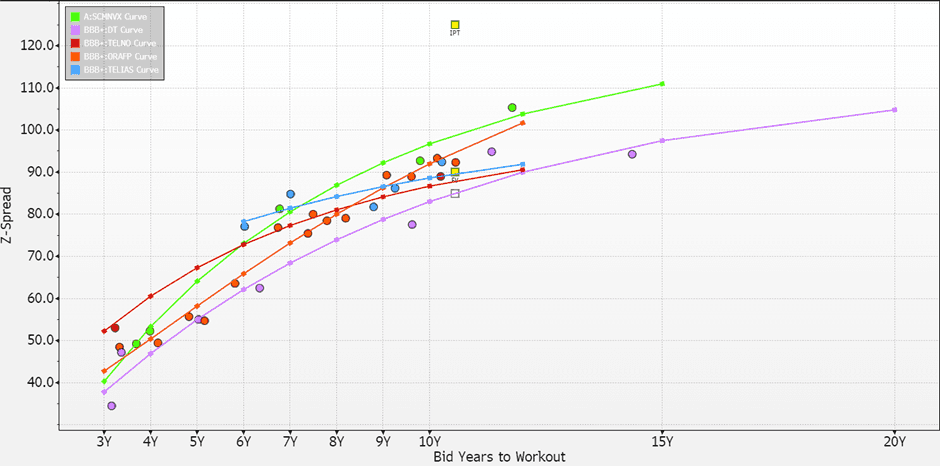

DT (EUR B’mark 10.5yr; Baa2[P]/BBB/BBB[P])

- IPT given at MS+125; we see FV around MS+90bps; noting low cash prices <90 on their 34s and 39s. First EUR bond in 5yrs on what is the tightest telco curve.

- Supply comes in the wake of their end-Oct shift to positive outlook at Moody’s following their CMD which saw strong targets with 4-6% adj. EBITDAaL growth and EUR 21bn FCFaL by 2027 (2023: EUR 16bn), supported by ambitious 5G/FTTH rollout and AI efficiencies with plans for T-Mobile USA stake increase. They dropped the lower bound on their leverage target though are also pivoting to shareholder-friendly priorities (e.g., buybacks, dividends).

- Q3 results in mid-Nov were strong with reported leverage at 2.64x against new Moody’s thresholds of 3x/3.5x (equiv to reported levels of 2.75x/3.25x): https://mni.marketnews.com/4hQdoD7

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Greenback on Cusp of Resuming Uptrend

Oct-21 09:12

- The greenback is reversing a decent part of Friday's pullback, keeping the broad dollar rally underpinned and the upside argument alive. The USD Index traded a new cycle high last week at 103.874, and a rally through here would resume the primary uptrend. We've written that better-than-expected US data is not the only driver of dollar strength, with domestic equity strength also playing a large part, raising the focus on the earnings schedule this week, across which 15% of the S&P 500 are set to report.

- Running in tandem with the US curve, the greenback is further clawing back some of the modest USD losses posted Friday, easing EUR/USD off highs and tipping GBP/USD to new intraday lows in recent trade, characterised by very light volumes. This keeps GBP among the poorest performers of the day so far, while firmer core US yields keep USD/JPY pressed toward Y150.00.

- 15min candle chart exposes weakness through 1.3023 support, exposing 1.3000/04 resistance. Any slip through 1.2961/74 would be a bearish signal and mark new monthly lows ahead of next week's budget release (Weds 30th) - through which FX could be more sensitive to volatility in bond prices given the upscaled focus on the release.

- Datapoints are few and far between Monday, leaving focus on the central bank speaker schedule. Fed's Logan speaks before the open, Kashkari during cash equity trade, and then Schmid and Daly follow after the close. Schmid's appearance will likely be the most consequential - addressing the US economy and monetary policy outlook directly, with a released text.

EURIBOR: EURIBOR FIX - 21/10/24

Oct-21 09:05

Source: EMMI/Bloomberg.

- EUR001W 3.3450 0.0060

- EUR001M 3.1450 -0.0020

- EUR003M 3.1380 -0.0630

- EUR006M 2.9720 -0.0560

- EUR012M 2.6300 -0.0790

EGB OPTIONS: DUX4 107.10/107.30 1x1.5 Call Spread Lifted

Oct-21 09:02

DUX4 107.10/107.30 1x1.5 call spread paper paid 2 on 10K, expires Friday.