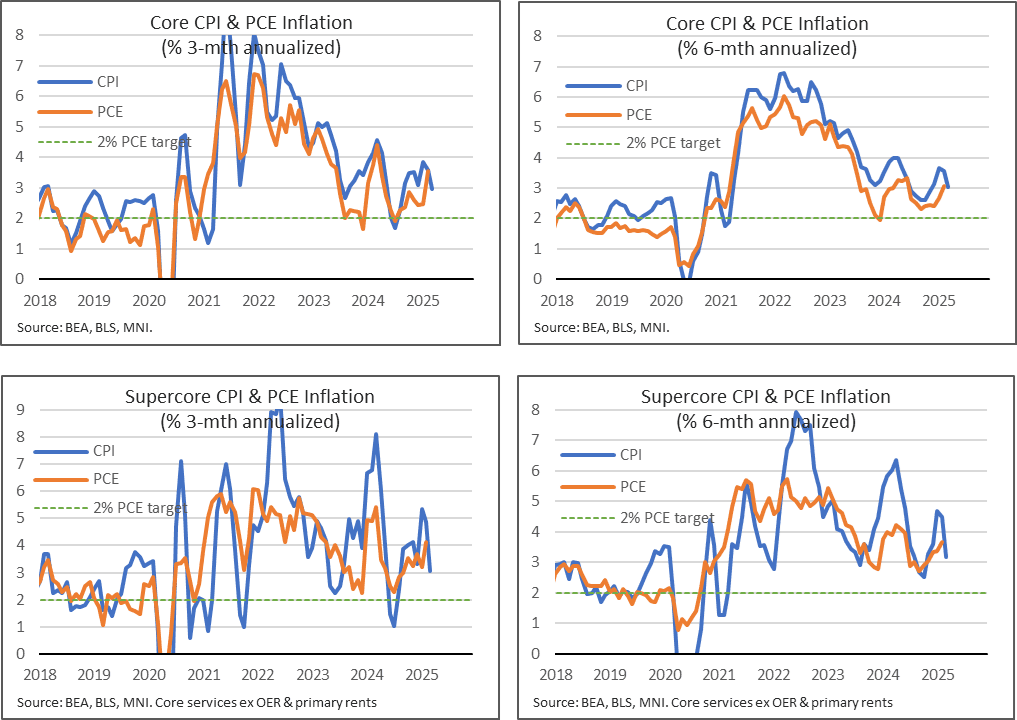

US DATA: CPI Trends Cool Faster Than Expected

Apr-10 13:05

- Looking over a longer basis, core CPI surprised notably lower in March at 2.79% Y/Y (vs consensus firmly centered on 3.0%) after the 3.12% Y/Y in Feb.

- It’s the lowest since Mar 2021.

- Recent run rates remain hotter, suggesting some upward momentum ahead in the Y/Y, but to a much lesser extent than was expected to have been the case.

- Both the three-month and six-month rates eased to 3.0% annualized from 3.6% as of Feb.

- The supercore run rates have seen a more pronounced slowing from strong rates, with the three-month from 4.8% to 3.1% annualized and the six-month from 4.5% to 3.2% annualized.

- Of course, the latter was biased lower by much larger than expected M/M declines in lodging, airfares and auto insurance in March, with the latter two not feeding into PCE as we say. That said, whilst lodging and airfares in particular are volatile categories, with anecdotal evidence of reduced Canadian travel to the US there’s only so much this might be downplayed.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

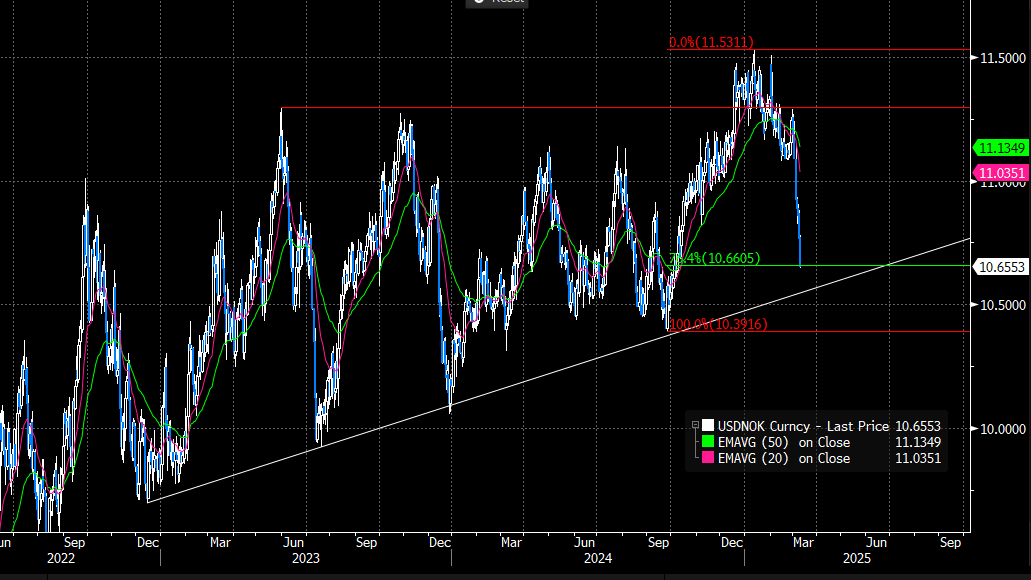

NOK: USDNOK Eyeing Trendline Support, Norges Bank March Decision Uncertain

Mar-11 13:03

USDNOK has pierced support at 10.6605, the 76.4% retracement of the September 2024 – January 2025 rally. Clearance of this level would expose trendline support drawn from the December 2022 low at 10.5454, which shields 10.3916 (the Sep 25, 2024 low). The pair is on track for a seventh consecutive session of lower lows, underscoring recent bearish momentum. This is the longest such streak since June 2023.

- The pullback in USDNOK from the Feb 28 high of 11.2885 had mostly been a function of USD weakness on heightened US growth concerns, until yesterday’s stronger-than-expected Norwegian February inflation report added pressure via the NOK leg.

- Today’s NOK strength could reflect some carry-over from yesterday’s data, which has reduced the market implied probability of a 25bp Norges Bank rate cut on March 27 to around 50% (from essentially 100% a few weeks ago).

- However, 2-year NOK swap rates are little changed today, suggesting the 1.2% recovery in brent crude futures is also supporting the krone.

- With the March Norges Bank decision now uncertain, focus for markets turns to the outcome of the 2025 wage bargaining rounds (the Technical Calculation Committee for Income Settlements is set to release a revised inflation estimate today, which will form a basis for negotiations) and the Q1 Regional Network Survey on March 20.

Figure 1: USDNOK

GILT SYNDICATION: 1.875% Sep-49 I/L gilt: Priced (additional details)

Mar-11 12:55

- Reoffer: 97.142 to yield 2.0234% (real)

- Spread set earlier at 0.125% Aug-48 linker (GB00BZ13DV40) + 1.0bp (Guidance was +1.0/1.5bps)

- Size: GBP5.0bln (larger than the GBP4.0-4.5bln MNI expected) - MNI note: This is the largest ever gilt linker syndication

- Books in excess of GBP67.5bln (inc JLM interest of GBP4bln) - MNI note: That is the largest ever book for a gilt linker syndication

- HR : 90% vs 0.125% Aug-48 linker (spot ref 64.880)

- Maturity: 22 September 2049

- ISIN: GB00BT7J0134

- Coupon: 1.875%, long first

- Settlement: 12 March 2025 (T+1)

- JLMs: BofA Securities, J.P. Morgan, Lloyds Bank Corporate Markets (B&D/DM), and UBS Investment Bank

- Timing: TOE 12:47GMT, FTT immediately

From DMO / market source / MNI colour

MNI: US REDBOOK: MAR STORE SALES +5.7% V YR AGO MO

Mar-11 12:55

- MNI: US REDBOOK: MAR STORE SALES +5.7% V YR AGO MO

- US REDBOOK: STORE SALES +5.7% WK ENDED MAR 08 V YR AGO WK