CHINA: Country Wrap: September Exports Surge (Ex US) as Trade War Intensifies

Market Summary: With Japan out today, it was left to China's major bourses to guide sentiment as the trade war rhetoric ramps up. Having declined over -1.9% Friday, the CSI 300 started the week on the back foot, dragging the other key bourses with it. Down -1.7% today, it was the biggest two days of consecutive falls since April when the trade war began first ratcheted up. The Hang Seng fell sharply, down -3.3% as it traded through the key 20-day and 50-day EMA's and now is approaching the 100-day EMA which it last traded below in April. There was little positives to find as Shanghai Comp fell -1.30% and Shenzhen down -2.2%. The retail expansion of equity accounts over recent months has been a key contributor to the performance of stocks and comes on the back of a multi year decline in housing. The authorities will be loathe to see significant stock losses for investors and news agencies over the weekend were keen to spell out that the outlook for the CSI 300 should be little impact by the threats coming from Washington. The Yuan Reference Rate at 7.1007 Per USD; Estimate 7.1234 and bonds are staging a mini rally with the 10-Yr back down to 1.83%, having trade above 1.9% just prior to the recent break. The stability in CGBs comes despite the PBOC releasing details that it undertook no government bond trading for a ninth consecutive month.

- The moderation of exports in August was short-lived as September's numbers jumped +8.3% YoY, beating expectations and much stronger than the month prior. According to BBG estimates, the decline in exports to the US was significant, down -27% YoY. This points to the growth of demand from non US markets, arguably weakening the US's position in a trade war. Exports to Africa, India and other Asian nations are soaring with the latter back to pre-COVID levels. US President Donald Trump had threatened to raise tariffs on China and withdraw from a high-profile upcoming meeting with Chinese President Xi Jinping, in a lengthy statement on Truth Social, citing a letter from Beijing which he claims lays out new rare earth export control measures. The new Chinese rare earth export control measures are scheduled to take effect on December 1. Starting November 8, Beijing will also restrict exports of equipment needed to manufacture batteries for electric cars in a bid to protect the competitiveness of Chinese autos, per The New York Times. Imports climbed +7.4% in September for it's largest monthly expansion since April 2024. Despite being a crude indicator for domestic demand, the result nevertheless comes a an invaluable time as the US rhetoric ramps up. Along with the decline in exports to the US, imports from the US declined -16.1%, widening the trade surplus with the US to $22.bn. Whilst this data captures a period before the weekend's escalation it may slightly strengthen Beijing's position in negotiations, given the ever growing decline in the US's importance to China's trade outcome. (source MNI)

- Mainland China’s commercial and financial hub Shanghai has pledged to remove all regulatory hurdles for foreign investors to set up manufacturing businesses, as authorities move to shore up confidence in the local and national economies despite rising US-China trade tensions. Mayor Gong Zheng said on Sunday that deepened reforms had been carried out to grant overseas companies in the fields of electric vehicles, value-added telecommunications services, biotechnology and hospitals full access to the Chinese market. (source SCMP)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (U5) Bounces Further Off Support

- RES 3: 97.190 - High May 5 2023

- RES 2: 96.932 - 76.4% of Mar-Nov ‘23 bear leg

- RES 1: 96.860 - High Apr 07

- PRICE: 96.550 @ 15:36 BST Sep 12

- SUP 1: 96.430/95.900 - Low Sep 3 / Low Jan 14

- SUP 2: 95.760 - Low 14 Nov ‘24

- SUP 3: 95.480 - Low Jan 11 2023 and a major support

Aussie 3-yr futures are trading off recent lows. A resumption of gains from here would further narrow the gap with resistance at 96.730, the Sep 17 ‘24 high, leaving 96.860 as the next key level. Any continuation lower would instead strengthen a bearish threat. This would refocus attention on 95.760, the 14 Nov ‘24 low. Conversely, a reversal higher would open 96.860, the Apr 7 high.

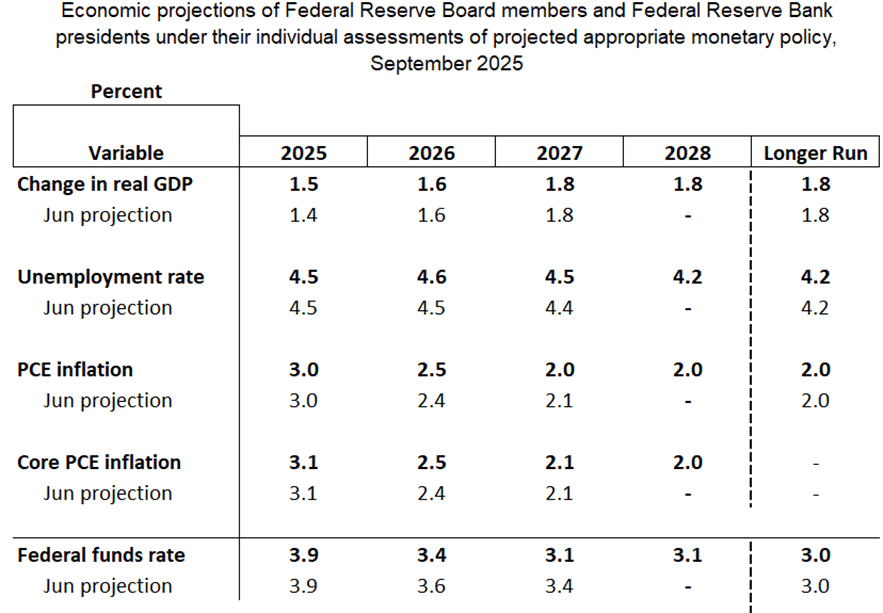

FED: MNI Fed Preview-September 2025: A Reluctant Return To Easing

We've published our preview of the upcoming FOMC meeting - Download Full Report Here

- The Federal Reserve is set to resume its easing cycle at the September 16-17 meeting with a 25bp cut to the funds rate range to 4.00-4.25%.

- The decision to cut after a 5-meeting pause was well-telegraphed by Chair Powell, whose Jackson Hole speech described a “shifting balance of risks” toward a weaker labor market that “may warrant adjusting our policy stance”.

- The updated quarterly projections aren’t likely to bring many changes to the macroeconomic variables, but as usual the signal sent from the Fed rate “Dot Plot” will garner attention. A Committee split between expecting one or two further cuts this year is likely, keeping each of the remaining meetings of 2025 “live”.

- The Statement will downgrade the description of the labor market to reflect a rise in the unemployment rate and poor payrolls growth, and is likely to include at least one dissent to the rate decision.

- But with a Committee that is fairly divided on the way forward, Powell will be noncommittal on future action, reiterating that policy is not on a preset course, and upcoming decisions will be data-dependent.

- A key undercurrent is an increasingly activist approach to Fed personnel management from the White House, which leaves the composition of the FOMC uncertain not just over the medium-term but also at this meeting.

MNI’s separate preview of sell-side analyst summaries to follow on Monday Sep 15

RATINGS: Fitch: France Cut To A+ From AA, Portugal Up To A From A-

Fitch has downgraded France's sovereign rating to A+ (with stable outlook) from AA-. Release here.

- Among other factors in the decision, Fitch cites "High and Rising Debt Ratio", "Political Fragmentation Hinders Consolidation", "Weak Fiscal Record", "High 2025 Deficit", "Uncertain Fiscal Consolidation Path", and "Fiscal Rigidities".

- In "Factors that Could, Individually or Collectively, Lead to Negative Rating Action/Downgrade", Fitch cites "Public Finances: A sustained increase in government debt/GDP over the medium term, due to failure to implement fiscal consolidation measures and/or a persistent increase in financing costs" and "Macro: Materially lower economic growth prospects and weakened competitiveness." Conversely, potentially leading to positive ratings action would be "Public Finances: Confidence that government debt/GDP will be put on a downward trajectory over the medium term, for example, due to fiscal consolidation and/or stronger economic growth".

- Fitch also raised Portugal to A (stable outlook) from A-, while elsewhere, S&P raised Spain to A+ (stable outlook) from A.

- As MNI wrote earlier, we expected France to be downgraded to A+ and Portugal to be upgraded to A.